The price of bitcoin keeps hitting new all-time highs, recently topping $24,000, which means things are getting a little nutty. The coiners want bitcoin to shoot to the moon. And the no-coiners want Tether to get taken down and the nonsense to end, like it should have three years ago after the 2017 bubble.

I’ve now got hundreds of new Twitter followers, most of them bitcoiners repeating the same boilerplate phrases like “have fun staying poor,” “gold is a Ponzi too” (it’s not) and proclaiming me the U.S. dollar is going to collapse, which would be a shame as bitcoin is mainly traded in dollars.

Caught up in the whirlwind, Mike Novogratz, CEO of Galaxy Digital, has gotten a tattoo—a large moon and a rocket with the letter “B” on it. Fortunately, the “B” is relatively small, so he can easily get that part lasered or covered up if bitcoin crashes, which it will, because that is the fate of all Ponzi schemes.

Here is the news:

Ledger creates a target list for SIM swappers

In July 2020, hardware wallet provider Ledger was hacked, with the hackers gaining access to its customer database. The database has been circulating for five months now, and the hacker has just dumped it on RaidForums, a site dedicated to sharing hacked databases, for the whole world to access—at no charge.

“The first confirmed price I saw for this database was 5 BTC,” the hacker wrote. “Today you can get it for free.”

The database contains the emails, physical addresses, and phone numbers of 272,000 Ledger buyers along with emails of 1 million additional users.

Essentially, Ledger, a company dedicated to security, has given hackers access to a massive target list for SIM swappers and phishing campaigns. Ledger is very, very sorry for the leak.

ALERT: Threat actor just dumped @Ledger's database which have been circling around for the past few months.

The database contains information such as Emails, Physical Addresses, Phone numbers and more information on 272,000 Ledger buyers and Emails of 1,000,000 additional users. pic.twitter.com/Sv9cQwhuNy

Coinbase, the most valuable U.S. crypto firm, has filed confidentially for an IPO with the SEC. When the crypto exchange last raised private funding in 2018, it was valued at $8 billion. It is probably worth plenty more now, with investors going mad over tech stocks.

The San Francisco company has tapped Goldman Sachs to bring it to market, meaning that that the bank will lead the syndicate of banks underwriting the deal. (Cointelegraph)

Several VCs have invested hundreds of millions of dollars into Coinbase, and it makes sense that at some point they want to realize the returns on their investment, probably before this bubble blows.

According to Nicholas Weaver, a researcher at the International Computer Science Institute in Berkeley, the IPO “is entirely about a16z and the other VCs unloading their ownership-bags, not cryptocurrency bags, before the space implodes because Tether finally gets killed.”

Note this is entirely about a16z and the other VCs unloading their ownership-bags, not cryptocurrency bags, before the space implodes because Tether finally gets killed.

The Financial Crimes Enforcement Network has unveiled new rules aimed at closing anti-money laundering loopholes for regulated cryptocurrency transactions. The rules call for additional customer verification and more reporting.

According to the proposed rule, if a user makes a deposit or a withdrawal of over $3,000 involving a non-custodial wallet, exchanges have to record the name and physical location of the wallet owner. Crypto exchanges also have to report to the U.S. Department of Treasury any deposit or withdrawal over $10,000.

The rule is devastating to regulated crypto exchanges. In a lengthy Twitter thread last month, when he first learned of the new rule coming down the pipes, Coinbase CEO Brian Armstrong publicly attacked the new regulation. He knows serious KYC requirements will kill a lot of his business.

Nouriel Roubini responded by bashing Armstrong as a contemporary Gordon Gekko—a character in the 1987 Oliver Stone movie “Wall Street”—putting his profits ahead of the need to enforce regulations to stop the financial activities of criminals, tax evaders, terrorists, drug dealers and human traffickers.

.@brian_armstrong : you are a self serving modern version of greed-is-good Gordon Gekko putting your profits ahead of the need of any civilized country to enforce AML/KYC/TFC regs to stop financial activities of criminals, tax evaders, terrorists, drug dealers, human traffickers! https://t.co/xKYxSgy3Nw

Tokyo bitcoin exchange Mt. Gox went bankrupt in early 2014, and its former users are still waiting to get some portion of their funds back. Their long wait may soon be over. Recently, the Mt. Gox trustee submitted a draft plan for the rehabilitation of creditors.

If the Tokyo District Court gives the plan a thumbs up, that means 140,000 bitcoin may soon flood the market. The price of BTC has gone up substantially since 2014, so no doubt claimants will want to sell as quickly as possible—and that could create a bear market, pushing down the price of BTC. (Coindesk)

Unless there’s enough real cash left in the system—which is unlikely, because if there was, we wouldn’t need 20 billion tethers—Tether will need to issue an additional 2.5 billion tethers to absorb those bitcoin.

Tether surpasses $20 billion

Tether has now crossed $20 billion worth of tethers in circulation. Paolo Ardoino, Bitfinex and Tether CTO, bragged about it on social media. He tweeted: “#tether $USDt 20 BILLION!”

Patrick McKenzie, the software engineer who last year wrote this brilliant article explaining Tether, says all he wants for Christmas is for “Tether to unwind explosively.”

As Tether keeps issuing more and more tethers to pump bitcoin’s price, remember that the whole point in all this is to lure real dollars into the system. Look, the price keeps going up! You too can get rich! Buy bitcoin!

As David Gerard explained in a recent blog post, bitcoin price pumps are almost always immediately followed by a sell off. If you’re still not convince how the game works, CryptoQuant CEO Ki Young Ju provides proof.

He points out that when bitcoin hit $20,000, it was a coordinated pump fueled by stablecoins—127 different addresses depositing stablecoins to exchanges in one block of transactions on Ethereum minutes before the first price peak. “Price is all about consensus,” he said.

Lots of people deposited stablecoins to exchanges 7 mins before breaking $20k.

Price is all about consensus. I guess the sentiment turned around to buy $BTC at that time.

Visa and Mastercard said they will stop processing payments on Pornhub following a report in the NYT about illegal content on the site uploaded by unverified users. Mastercard has cut off ties completely, while Visa says it has cut off ties pending an investigation. (Decrypt)

According to Vice, Pornhub purged 70% of its content in an attempt to get the card providers back. How else will it stay in business? The site still accepts crypto—and cash via checks and wires—but apparently that’s not enough. There’s no way it can function without the credit card payments. More proof that bitcoin is a failed payments system.

Other news

The Dread Pirate Roberts is sorry, so please let him go. President Trump is weighing granting clemency to Ross Ulbright, the founder of the Silk Road. (Daily Beast)

“If Ulbricht’s supporters really cared about the war on drugs or libertarian ideals, they’d be demanding that the nearly half a million people currently in U.S. jails for drug offenses should be pardoned too.” (Vanity Fair)

A NY judge says Reggie Fowler’s defense team can withdraw from the case. Their client hasn’t paid them in a year. Fowler has 45 days to find a new lawyer who is also willing to risk not getting paid. (My blog)

Binance reportedly puts zero actual effort into keeping U.S. customers out. The info comes by way of a U.S. user who created a BFX account (no VPN), transferred bitcoins to BFX and sent some out from there. (Twitter)

If you want to cash out your USDT on Kraken, the exchange apparently only takes two types: Omni or ERC-20. (Twitter)

Eric Peters, CEO of One River Asset Management, has set up a new company to invest in crypto. His firm will bring its holdings of bitcoin and ether to about $1 billion as of early 2021, he said. (Bloomberg)

Michael Saylor wants to lure Elon Musk into bitcoin. (Decrypt)

A New York district judge agreed to allow Reginald Fowler’s defense team to withdraw from their client’s case due to nonpayment. He then gave Fowler 45 days to seek a new attorney.

(Update on Feb. 9: The judge has given Fowler three more weeks. Fowler now has until Feb. 25 to retain new counsel, according to the latest court filing.)

Judge Andrew L. Carter

Fowler is the former NFL minority owner linked to hundreds of millions of dollars in missing Tether and Bitfinex funds. Tether is the company that has so far issued $20 billion worth of stablecoins, and Bitfinex is a crypto exchange. Both companies are operated by the same individuals.

In a telephone status conference today, Judge Andrew L. Carter agreed to allow Fowler’s defense counsel—Hogan Lovells and Rosenblum Schwartz & Fry—to step down. They claim their client owes them more than $600,000.

However, while the government agreed to letting the lawyers withdraw, it was opposed to an adjournment of the April 28 trial, arguing that the situation was of Fowler’s own making. After all, his lawyers had been warning him since February they were planning to quit. The trial has already been postponed twice.

“We believe the almost four months until trial is sufficient time for a new counsel to prepare for trial,” U.S. Assistant Attorney Jessica Greenwood told the judge.

Judge Carter disagreed. That assumes Fowler’s new attorneys have already been retained and are on the case today, he said, stressing that it may take time for Fowler to find a new lawyer—especially given that his current lawyers are seeking to withdraw because he hasn’t paid them.

“That usually doesn’t make the defendant a very attractive client to a subsequent law firm,” Carter said.

The judge then explained to Fowler—who was on the call, joined by his defense team—that if he was unable to afford a new attorney, the court would provide him one free of charge. However, he would need to fill out a financial affidavit for the court to make that determination.

Although Fowler would not admit to whether he could afford an attorney, he did say he wished to try and hire one who would be more willing to work with him given his “current condition.”

“The government has seized all my assets,” he said, starting to sound a bit angry. “The government has asked me to put the properties that I have that are free and clear up for bail. The government has handcuffed me. They have shut me down. They have locked down my family,” he said—though it’s not clear what he meant in saying his family was “locked down.”

“I can’t even get a bank account. My business has been shut down since COVID, so we don’t have any income. We do have assets. We can’t get to the assets because the government has tied them all up, so what I want to do, respectfully, is to try to find a firm that will work with me, understanding that we have assets that are tied up by the government, i.e., the properties that have me set for bail, or whatever you call it.”

Fowler, now living in Chandler, Arizona, is free on $5 million bail. Five properties were put up for lien in order to secure his bond.

He called it “ludicrous” that the government forced him to put up “nearly $2 million worth of nearly free-and-clear properties” for bond. (A quick look on Zillow puts the properties’ value at around $1.4 million.)

Fowler said if he could not find an attorney to work with him, he would ask the court for assistance.

The judge stressed that Fowler has a right to be represented by an attorney, and gave him until Feb. 2, 2021, to find one on his own. A new trial date will be set after that time, the judge said.

Hogan Lovells also represents Fowler in a class-action complaint against Tether and Bitfinex, in which Fowler is named. They are seeking to withdraw from that case as well.

The price of bitcoin is headed back over $19,000 again. What will it take to push it past $20,000—more tethers? More institutional buying? Or maybe, more crypto journalists proclaiming (without evidence) that tethers are fully backed? Here’s the news:

MicroStrategy wants more, more, more

Michael Saylor, the new crazy god of bitcoin institutional buying, continues his bitcoin buying spree. He seems really, really confident the price of BTC will go up.

Saylor’s publicly traded company MicroStrategy currently owns 40,824 bitcoins—because no sense using all that excess cash for buying back a ton of stock or paying a big dividend. Better off to gamble it on crypto.

Now the firm is actually going into debt to buy bitcoin. After completing a $650 million bond offering, MicroStrategy plans to plow all the proceeds into buying more bitcoin. (Microstrategy PR, Cointelegraph)

Citibank isn’t impressed. Analyst Tyler Radke downgraded MicroStrategy (MSTR) from neutral to sell, calling the recent rally—MSTR went up after its first few BTC buying announcements—”overextended” and a possibly “deal-breaker” for software investors. (The Block)

Tether: Ain’t no stopping us now

Tether is now at $20 billion worth of tether—that’s assets, but circulating supply is soon to follow—and there is no evidence whatsoever to conclude that there is $20 billion in real cash behind all those tethers. Why? Because the company has never had a formal audit.

Still, last month, The Block’s Larry Cermak defended tethers as being “either fully backed or very, very close,” telling folks “everything is in order now.” He based that on conversations he claimed to have had with “third-parties” who told him they had successfully redeemed several hundred million in tethers.

Cermak is not the only one to buy the Tether line of B.S.

In December 2018, after looking at Tether bank statements, Bloomberg’s Matt Leising also reported that Tether appeared to be fully backed. He was wrong.

Unbeknownst to him at the time, in the previous two months, the DOJ froze five NY bank accounts belonging to Reginald Fowler, who ran a shadow banking service for Tether/Bitfinex’s Panamanian payment processor. And in November, the NYAG, having serious concerns about Tether’s finances, issued subpoenas to Bitfinex and Tether asking for details on their banking. Finally, in April 2019, Tether admitted it was only 74% backed. And that’s before it went off and printed another 17.5 billion tethers. So what’s backing all those?

In a recent blog post, David Gerard explains why Tether is “too big to fail.” Essentially, it’s keeping the entire BTC market afloat. If Tether were to get the Liberty Reserve treatment, the price of bitcoin is unlikely to ever recover.

Thus, “the purpose of the crypto industry, and all its little service sub-industries, is to generate a narrative—so as to maintain and enhance the flow of actual dollars from suckers, and keep the party going,” he said.

NYAG: Tether documents forthcoming

Meanwhile, there’s been a new document filing in the NYAG Tether probe.

In a letter to the NY supreme court, NYAG says Bitfinex/Tether are cooperating on document production and the parties expect to finalize things “in the coming weeks.” These documents, of course, consist of everything NYAG asked for in its original November 2018 subpoena—information that will shed light on the Tether and Bitfinex’s shadowy dealings since 2015.

A part of me wants to get excited about this news, but another part says, wait a minute. In the past when Tether’s operators said they were going to hand documents over, they simply handed over material that was already public information. They also have a long history of shenanigans, so let’s just wait and see.

How to turn USDT into cash

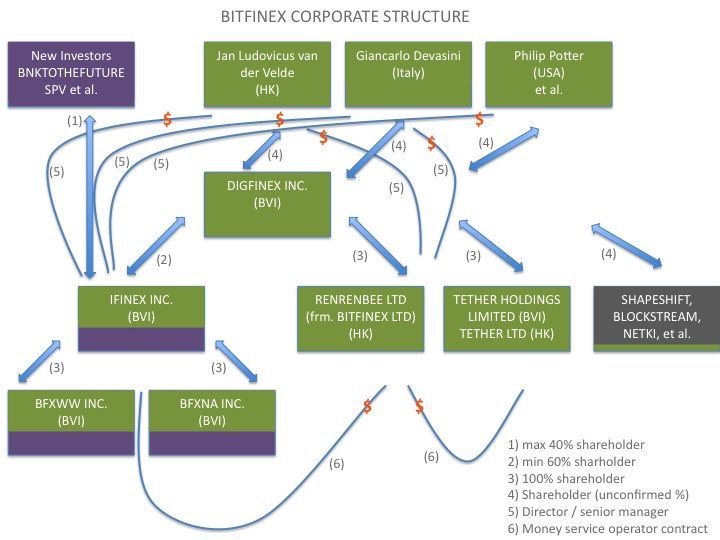

Jorge Stolfi, a computer scientist from Brazil, shared on Reddit a “mainstream theory” on what could be happening behind-the-scenes at Tether—specifically, how Tether’s operators could convert USDT into cash for their own personal use. Remember, this is totally unproven. It is just a theory. (The “triad,” by the way, refers to Tether CSO Phil Potter, CEO and man of mystery J.L. van der Velde, and CFO Giancarlo Devasini. They are the same operators behind sister company Bitfinex.)

He writes:

The owners of Tether Inc (which I will call “the Triad”) print billions of USDT without any backing.

The Triad deposits those USDT into Bitfinex (which they own too).

The Triad uses those USDT to buy BTC and other cryptos from other Bitfinex clients, attracted by the better price.

The Triad withdraws the BTC to their private wallets.

The Triad moves all or some of those BTC to other exchanges that handle real currencies, such as USD, EUR, JPY, etc.

The Triad sells those BTC for real money.

The Triad withdraws the real money into their personal bank accounts.

This is a theory. This is not proven. But the point is, when you have no checks and balances in place along with massive loopholes in oversight, anything can happen. We saw this already with QuadrigaCX—the Canadian crypto exchange that went bankrupt after the founder disappeared (aka “died in India”), taking along with him hundreds of millions of dollars in customer funds.

Coinbase loses half critical security team

After NYT reporter Nathaniel Popper reported about discriminatory complaints at Coinbase, new information came out. Among those who recently resigned to protest the exchange’s new internal policies, were four of the seven people on Coinbase’s critical security team—aka the “key management team.”

New detail on how the turmoil at Coinbase has hit the company's efforts to secure its Bitcoins.

Among the people who resigned this fall – to protest new internal policies – were 4 of the 7 people on the most critical security team, the "key management team," sources told me.

The key management team is responsible for securing the cryptographic keys to Coinbase’s cold wallets, where the majority of the company’s crypto is held—somewhere in the neighborhood of $30 billion.

“No job is more fundamental to the company’s success,” Popper said.

Coinbase’s security chief shot back, saying Coinbase’s security team is managed by several teams with redundancy built in. Of course, he wants us to believe everything is fine, but not everyone is convinced.

LOL what "most of the key management team for Coinbase's cold wallets quit" is absolutely not a "nothingburger"

Bitcoin has a new institutional investor: MassMutual. The Springfield-Mass insurance firm purchased $100 million worth of BTC for its general investment account, which totals $235 billion. (WSJ)

MassMutual purchased the bitcoin through NYDIG, a New York-based fund management company, which has $2.3 billion worth of crypto under management. MassMutual also acquired a $5 million minority equity stake in NYDIG.

The $100 million cash injection into bitcoin sounds like a lot, but it’s small potatoes. That money will cover the network’s operators—the bitcoin miners—for only six days. Remember, bitcoin miners are selling their 900 newly minted bitcoin per day for $17 million, at current BTC prices. Investors will never see that money again. Bitcoin doesn’t make any real profits on its own—just investor money going in one end, out the other.

Law firm Hogan Lovells is requesting to withdraw their representation of Reggie Fowler in a class-action against Bitfinex and Tether in which Fowler is also named. (Motion to withdraw)

Bryce Weiner has written a nice overview of how Tether works in relation to the crypto industry.

Crypto-friendly CFTC chair Heath Tarbert plans to resign early next year. His term was set to expire in 2024. (The Block)

Bitcoin’s right-libertarian anarcho-capitalism fits right in with far-right extremism. Crypto analyst Tone Vays brags on Twitter about spending a night with the Proud Boys.

If you like my work, please consider supporting my writing by subscribing to my Patreon account for as little as $5 a month. Thank you!

Among other things, it means MicroStrategy CEO Michael Saylor has replaced Patrick Bryne as the new crazy god of institutional bitcoiners. And another crypto exit scam has been invented: dying in India. (See Jorge Stolfi’s full reddit post. He is a computer scientist in Brazil.)

All Ponzi schemes eventually implode, even if it takes 25 years like Bernie Madoff’s did. When that happens, you have two choices: turn yourself in or disappear. Gerald Cotten chose to disappear. Of course, many people believe he is really and truly dead. I’m just not one of them.

With that, here is the news that I find interesting from Bitcoinlandia, an imaginary place where people keep insisting bitcoin is not a Ponzi.

MicroStrategy buys more BTC

MicroStrategy continues to funnel its excess cash into bitcoin. The analytics firm bought another $50 million worth of bitcoin, Saylor disclosed in a tweet.

MicroStrategy has purchased approximately 2,574 bitcoins for $50.0 million in cash in accordance with its Treasury Reserve Policy, at an average price of approximately $19,427 per bitcoin. We now hold approximately 40,824 bitcoins.https://t.co/nwZcM9zAXZ

MicroStrategy bought its most recent pile of bitcoins at an average price of $19,427—at the top of the market—and now owns a total of 40,824 bitcoins.

Here’s the thing: Saylor holds 73% of the voting stock of MicroStrategy, so he does not need buy-in from stockholders to make decisions. He is ruler and king, and if he wants his firm to buy more bitcoin, so be it.

Saylor also has a large private stash of bitcoins. I would be very curious to know how much BTC he owned before and after MicroStrategy’s recent purchase.

If those bitcoin hold their value, all will be fine, Jorge Stolfi said on Reddit. But, if BTC “drops back to $8,000, the other stockholders will be upset, and may have grounds to sue Michael for mismanagement or whatever—even if there are no other shenanigans. If he did sell his coins while the company bought them, it will be worse.”

Guggenheim Partners

Another institutional investor has jumped on the bitcoin bandwagon. In a recent SEC filing, Guggenheim Partners, a leading Wall Street investment firm, revealed that it is looking to invest 10% of its $5.3 billion Macro Opportunities Fund into Grayscale’s Bitcoin Trust.

To be clear, Guggenheim is not buying bitcoin directly. It plans to invest nearly $500 million in GBTC shares. Grayscale itself now owns more than 500,000 bitcoin.

And Guggenheim isn’t taking on any risk. The firm makes money whether the price of BTC goes up or down. The retailers who are invested in the fund are the ones who carry all the risk.

Bitcoin is highly volatile and has no role in retail investor portfolios. As Economist Nouriel Roubini explained in a lengthy Twitter rant:

“Investing in BTC is equivalent to [taking] your portfolio to a rigged illegal casino & [gambling]; at least in legit Las Vegas casinos odds aren’t stacked against you as those gambling markets aren’t manipulated the way BTC is. Instead BTC is manipulated heavily by Tether & whales.”

Tether’s runaway train

On to my favorite topic: Tether—a firm that mints a dollar-pegged stablecoin that’s hugely popular on unbanked exchanges.

On Nov. 28, Tether surpassed 19 billion tethers in circulation. And like a runaway train with no way of stopping, it is fast on its way to issuing 20 billion tether—worth the notional equivalent in US dollars.

So, what is going on with the New York Attorney General’s investigation into Tether and Bitfinex?

The last bit of real news we had was in September when Judge Joel M. Cohen once again ordered Bitfinex and Tether to turn over financials. However, he did not set a deadline. He left that decision to a special referee, according to Coindesk. And we haven’t heard anything on the matter since.

Stepping back, recall that Bitfinex/Tether have been resisting handing over documents since November 2018 when the NYAG—in pursuant to the Martin Act, which gives it broad powers to investigate fraud—first served subpoenas for information stretching back to January 2015.

In April 2019, when the NYAG was concerned that iFinex (parent company of Bitfinex/Tether) was insolvent and Bitfinex was dipping into Tether’s cash reserves, it sought an ex parte order compelling the companies to produce documents and staying further actions pending the ongoing investigation.

iFinex responded with a motion to dismiss. In August 2019, the Supreme Court denied the motion and the respondents sought to appeal, arguing that the NYAG did not have the power to demand documents since Bitfinex and Tether didn’t have sufficient contacts in New York.

In July 9, 2020, a New York state appeals court sided with the NYAG. (Court filing)

As I’m writing up this newsletter, Coindesk’s Nikhilesh De has just pulled up a new court filing in the case from Dec. 4 that is a bit bewildering. At first glance, it appears to be the same filing from July, repeated twice.

So there was a new filing in NYAG v iFinex on Friday (h/t @ahcastor for making me think of this today). But there's something odd about this… https://t.co/rS7MXJBW1B

Drew Hinks, a lawyer not involved in the case, said the filing is a remittitur—a jurisdictional document that formally ends the life of an appeal by notifying the world that the decision is final.

I’ll update this post as I learn more—specifically why a remittitur is important after the appellate judgment has already been issued and become final. Does this help the investigation going forward?

(Update: I am pretty sure that the remittitur was just a procedural thing that signals that the appellate court is done and has kicked the ball back to the original court—i.e., Justice Cohen.)

Bitcoin sets new all-time high

On Nov. 30, the price of bitcoin reached $19,900 on Coinbase, according to the Block, surpassing its previous all time high (ATH) set on Dec. 17, 2017, by about $10.

After bitcoin reached its new high, it promptly lost 13% of its value.

When you see bitcoin getting pumped like this, what you are seeing is traders cashing out before the bubble bursts. Bitcoin is not a company. It does not create any actual revenue. Cash coming into the system goes to paying the miners, who sell their 900 newly minted BTC per day and earlier investors lucky enough to sell at the right time.

I’m sure the current pump has nothing to do with the NYAG getting closer to exposing Tether/Bitfinex’s inner workings, the recent indictment of BitMEX operators, and Binance’s latest efforts to aggressively block U.S. citizens from using its exchange.

Binance pulls in big profits

The largest tether exchange expects to earn between $800 million and $1 billion in profits for 2020, its captain Changpeng Zhao (“CZ”) told Bloomberg. The Malta-registered exchange also expected $1 billion in profits 2018.

Speaking of Binance, the crypto exchange is suing Forbes and two journalists for a recent report claiming that the exchange had a plan to dodge regulations. (Here is the complaint.) It’s unlikely CZ will get anywhere with this lawsuit because the suit will get torn apart in discovery.

Similar to when Bitfinex threatened to sue prolific critic Bitfinex’ed in December 2017, this is likely more of warning to other journalist: don’t dig too deep, or we’ll come after you.

STABLE Act

The big news of the week is that three congressional democrats are trying to pass a bill that will require stablecoin issuers to comply with the same regulations and rules as banks.

If passed, the Stablecoin Tethering and Bank Licensing Enforcement (STABLE) Act, would require stablecoin issuers to apply for bank charters, get approval from the Federal Reserve and hold FDIC insurance. (The bill, press release.)

Stablecoin issues are like wild cat banks. Back in the 1800s banks would issue their own currency, and nobody knew what was backing the currency. And because these banks were often in remote, hard to get to locations, people often had trouble redeeming their notes for silver or gold or whatever it was that was supposed to be backing them.

They are banks printing their own banknotes. It is literally recapitulating 19th century banking. They just don't have pretty critters on the pieces of paper.

Reggie Fowler owes his defense team $600,000. Lawyers were conned by a con. (My blog)

Joe Biden intends to nominate Adewale Adeyemo as Deputy Treasury Secretary, not Gary Gensler as previously thought. (New York Times)

Bill Hinman, who first spoke of “sufficient decentralization,” served his last day as SEC’s Division of Corporation Finance director on Friday. (SEC statement on departure)

Spotify is looking to add support for crypto payments. The streaming service wants to hire an associate director to lead activity on the libra project and other crypto efforts. (Coindesk)

If you like my work, please consider supporting my writing by subscribing to my Patreon account for as little as $5 a month.

Reggie Fowler, the former NFL minority owner linked to missing Tether and Bitfinex funds, owes his defense team more than $600,000, according to a new court filing on Tuesday.

Fowler’s lawyers want to drop out of the case due to nonpayment, but they need to get permission from the court first.

Last we left off, U.S. District Judge Andrew Carter ordered attorneys at law firm Hogan Lovells—also representing defense lawyer Scott Rosenblum at Rosenblum Schwartz & Fry—to file three versions of a sealed letter dated Nov. 18.

The public version—redacting what should not be revealed to the government or the public—discloses more details on the lawyers’ frustrations with a client who perpetually strings them along.

Hogan Lovells attorneys James McGovern and Michael Hefter initially asked for a $25,000 retainer in late 2018 when they first met with their client. Fowler only ever paid the retainer, and two years later, he now owes them $600,000.

His defense team believed all the stories he told them that he was swimming in money, so they weren’t too concerned—at first.

“From the very inception of this matter, we have been led to believe that Mr. Fowler is a high net worth individual with substantial assets, which would allow him to pay his legal bills with little hardship,” the lawyers said in their letter to the judge.

Hogan Lovells started working with Fowler on October 18, 2018. They had their first meeting with him on Nov. 8, 2018, around the time Fowler was initially contacted by the FBI.

“When we agreed to represent Mr. Fowler, it was our understanding that he had been targeted by cryptocurrency businessmen seeking to take advantage of Mr. Fowler’s personal balance sheet as a means of transacting cryptocurrency transactions without drawing the attention of bank compliance officers or regulators,” they said.

After his release in May on $5 million bail, Fowler hired Scott Rosenblum to join the defense team. Rosenblum asked for a $275,000 retainer and an additional $85,000 per week retainer, if the case went to trial. Rosenblum received a partial retainer of $100,000, which Hogan Lovells notes that Fowler paid “while he had several unpaid, overdue invoices for legal services issued by Hogan Lovells.”

Additionally, Fowler paid another lawyer (unnamed) in Portugal in full for her services. He also paid international law firm Reed Smith LLP for services rendered in 2018.

“The fact that other attorneys had received payments from Mr. Fowler for their services led us reasonably to believe that Mr. Fowler’s representations to us that he would pay our bills was truthful,” the lawyers said.

In the second half of 2019, the lawyers were diligent about contacting Fowler for money. Each time they reached out, he told them payment was imminent and that “transactions or business deals that would fund the payment of our fees were in process”—but he never paid him.

In February, following a plea bargain that went awry and a superseding indictment, the defense team realized the case would likely go to trial, requiring a substantial amount of work, and still no check from their client.

Fowler has ample funds, they said, including “$10 million in real estate that is unencumbered and could have been liquidated or monetized at any point during the past two years.” His refusal to pay, the lawyers added, has “led to a breakdown in the attorney-client relationship.”

The government has till Dec. 8 to respond and replies are due Dec. 11.

If you like my work, please consider supporting my writing by subscribing to my Patreon account for as little as $5 a month.

Are the pixie fairies sprinkling gold dust on bitcoin’s market again? By the looks of things, you might think so.

Like in the bubble days of 2017, the price of bitcoin is headed ever upward. On November 18, 2020, it surpassed $18,000 — a number not seen since December 2017 when bitcoin, at its all-time peak, scratched $20,000.

Of course, the market crashed spectacularly the following year, and retailers lost their shirts. But here we are once again, trying to unravel the mysteries of bitcoin’s latest price movements.

Several factors may explain it — Tether, PayPal, and China’s crackdown on over-the-counter desks — but before we get into that, let me reiterate how critical it is for bitcoin’s price to stay at or above a certain magic number.

Bitcoin miners — those responsible for securing the bitcoin network by “mining” the next block of transactions on the blockchain — need to sell their newly minted bitcoins for real money, so they can pay their massive energy bills.

Roughly $8 million to $10 million in cash gets sucked out of the bitcoin ecosystem this way every day. So, in order for the miners — the majority of whom are in China — to turn a profit, bitcoin needs to be priced accordingly. Otherwise, if too many miners were to decide to call it quits and unplug from the network all at once, that would leave bitcoin vulnerable to attacks. The entire system, and its current $345 billion market cap, literally depends on keeping the miners happy.

Now let’s jump to May 11, an important day for bitcoin. That was the day of the “halvening,” an event hardwired into bitcoin’s code where the block reward gets slashed in half. A halvening occurs once every four years.

Before May 11, miners received 1,800 bitcoin a day in the form of block rewards, which meant they needed to cash in each bitcoin for $5,000. But after the halvening, the network would produce only 900 bitcoins per day, so miners knew they needed to sell each precious bitcoin for at least $10,000.

But trouble loomed. Just months before the halvening, the price of bitcoin went into free fall. Between February and March, when the world was first gripped by the COVID crisis, bitcoin lost half its value, dropping to a low of $3,858 on March 13 — barely enough to pay the system’s energy costs post-halvening. Miners were likely pacing, wringing their hands, wondering how they would stay in business. Who would guarantee their profits?

That is when Tether — a company that produces a dollar-pegged stablecoin of the same name — sprung into action and started issuing tethers in amounts far greater than it ever had before in its five years of existence.

Tethers, for the uninitiated, are the main source of liquidity for unbanked crypto exchanges, which account for most of bitcoin’s trading volume. Currently, there are $18 billion (notional value) worth of tethers sloshing around in the crypto markets. And nobody is quite sure what’s backing them.

Due to Tether’s lack of transparency, its failure to provide a long promised audit, and the fact that the New York Attorney General is currently probing the firm along with Tether’s sister company, crypto exchange Bitfinex, for fraud, a good guess is nothing. Tethers, many suspect, are being minted out of thin air.

(Tethers were initially promised as an IOU where one tether was supposed to represent a redeemable dollar. But that was long before the British Virgin Island-registered firm began issuing tethers in massive quantities. And no tethers, to anyone’s knowledge, have ever been redeemed—except for when Tether burned 500 million tethers in October 2018, following the seizure of $850 million from its payment processor Crypto Capital.)

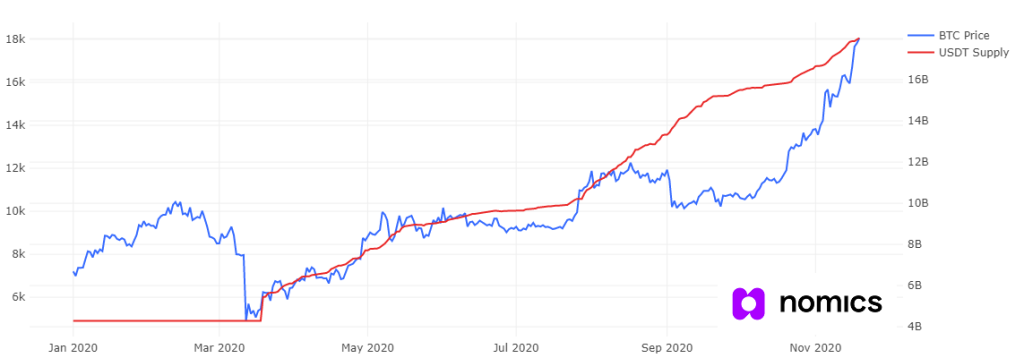

According to data from Nomics, at the beginning of 2020, there were only $4.3 billion worth of tethers in circulation. That number remained stable through January and February and into March. But starting on March 18, just five days after bitcoin dipped below $5,000, the tether printer kicked in.

Tether minted 4.4 billion tethers in April 2020 — crypto’s version of an economic stimulus package. By early June, the price of bitcoin crossed $10,000. Yet the Tether printer kept printing, pushing the price of bitcoin ever skyward and giving bag holders an opportunity to cash out.

In May, June, and July 2020, Tether issued a combined total of 3 billion tethers. In August, when the price of bitcoin reached $12,000, Tether issued another 2.6 billion tethers. In September, when bitcoin slid below $10,000, Tether infused the markets with another 2.2 billion tethers, although, even that couldn’t lift bitcoin up to $12,000 again. The price just hovered in the $10,000 range.

And then in October — just after US prosecutors charged the founders of BitMEX, a Seychelles-registered, Hong Kong-based bitcoin derivatives exchange, for failing to maintain an adequate anti-money laundering program — the price of BTC started to soar. What happened?

Tether’s frenzied pumping

One theory is that Tether just kept issuing tethers, billions and billions of them, and those tethers were used to buy up bitcoin. A high demand drives up the price — even if it’s fake money.

Only unlike in 2017, the effort to drive up bitcoin’s price is requiring a lot more tethers than ever before. (At the end of 2017, before the last bitcoin bubble popped, there were only $1.3 billion worth of tethers in circulation, a fraction of what there are today.)

Nicholas Weaver, a bitcoin skeptic and a researcher at the International Computer Science Institute in Berkeley, is convinced bitcoin’s latest price moves are 100% synthetic.

“The amount of tether flooding into the system is more than enough explanation for the price as it is well more than the amount needed to buy up all the newly minted bitcoin,” he told me. “If it was organic, there would at least be some significant increase in the outstanding amount of non-fraudulent stablecoins.”

What he means is, if real money was behind tether, we’d be seeing a similar demand for regulated stablecoins. But that is not the case. Only one regulated stablecoin has seen substantial growth — Circle’s USDC — but that growth is far overshadowed by Tether, and mainly a result of the growing decentralized finance (DeFi) market — a topic for another time.

Jorge Stolfi, a professor of computer science at the State University of Campinas in Brazil, who in 2016 wrote a letter to the SEC advising about the risks of a bitcoin ETF, which the SEC published, agrees.

“As long as fake money can be used to buy BTC, the price can be pumped to whatever levels to keep the miners happy,” he told me. He went on to explain in a Twitter thread that the higher the bitcoin price, the faster real money flows out of the system — assuming miners sell all their bitcoin for cash. Multiply bitcoin’s current price of $18,600 times 900, and that’s nearly $17 million a day. Investors will never get that money back, he said.

Klyith (not his real name) from Something Awful, a predecessor site to 4Chan, explains Tether this way:

“A bunch of pixies show up and start flooding the parchment market with fairy gold, driving prices to amazing new heights. But when any of the player characters try to spend the fairy gold in other towns or to pay tithes to the king, it turns into worthless rocks.

“If you denounce the pixies to the peasants or start using dispel magic to reveal that fairy gold is rocks, the price of parchments will collapse and the peasants may stop using them altogether. But if you ignore the pixies and keep the parchment economy going, you will end up with more and more worthless rocks instead of gold. The pixies can of course tell the difference between fairy gold and real gold at a glance. So they will quickly drain all the real gold from the whole township if you don’t act. What do you do?”

Still, it is hard to imagine that outside events don’t have some impact on bitcoin’s price. Two other events are being talked about right now as reasons behind bitcoin’s price gains—and they are getting a lot more media attention than Tether.

PayPal’s shilling

One of the biggest companies in the world is now promoting crypto, giving retail buyers the impression that bitcoin is a safe investment. After all, if bitcoin were a Ponzi or a scam, why would such a well-known, respectable company embrace it? I should add that MicroStrategy, Square, Fidelity Investment and Mexico’s third-richest person, Ricardo Salinas Pliego, are also currently shilling bitcoin on the internet.

On Oct. 21, PayPal announced a new service for its users to buy and sell crypto for cash. And on Nov. 12, the service became available to U.S. customers, who can now buy and sell bitcoin, bitcoin cash, ether, and litecoin via their PayPal wallet.

If you are a PayPal user, you have already gone through the process of proving you are who you say you are. And that removes the hassle of having to sign up with an crypto exchange, like Coinbase in the U.S., and take selfies of yourself holding up your driver’s license or passport.

Of course, there are limitations. You can’t transfer crypto into or out of your wallet, like you can on a centralized exchange. But you can pay PayPal’s 26 million merchants with crypto — although, not really, because what they receive on their end is cash. And the transaction is subject to high fees, like 2.3% for anything under $100, so what is the point? All you are doing is taking out a bet against PayPal that the price of bitcoin is going to rise.

Stolfi describes PayPal on Twitter as “a meta-casino where you can choose to use special in-house chips with a randomly variable value.”

The broader point is that PayPal makes it easy to buy crypto for people who are less likely to understand how crypto really works or know about Tether and the risk it imposes on the crypto markets. (If authorities were to arrest Tether’s operators and freeze its assets, similar to what happened to Liberty Reserve in 2013, that could lead to a huge plummet in bitcoin’s price.)

If you think Tether doesn’t have that big of an impact on bitcoin’s price, recall that Tether/Bitfinex CFO Giancarlo Devasini (going by “Merlin”) is recorded in the NYAG’s 2019 complaint as having reached out to Crypto Capital to plead for missing funds: “Please understand all this could be extremely dangerous for everybody, the entire crypto community,” said Merlin, indicating what could happen if Tether failed to exist. “BTC could tank to below 1k if we don’t act quickly.”

PayPal this month reached 85% of the volume of Binance.US, the U.S. branch of major crypto exchange Binance. Granted the volume of Binance.US is small in comparison with Binance’s main crypto exchange, but you can see where this is going.

One thought is that PayPal’s move into crypto is a “death sentence” for bitcoin, and that Tether and the exchanges who depend on tethers are working together to pump up the price of bitcoin to lure as much cash into the system as possible while the going is good.

Paypal's move was a death sentence for crypto. It's much easier for people to simply "buy Bitcoin" on Paypal, instead of sending their fiat to exchanges & Tether. That's why they rushed their epic pump now, before Paypal gains traction, to get as much FOMO cash as they still can.

According to news coming out of the country, China’s bitcoin miners may be encountering difficulty selling their bitcoin on over-the counter exchanges.

Since China banned crypto exchanges three years ago, OTC exchanges — where buyers and sellers go to trade directly — have become the most convenient way for the country’s citizens to on-ramp and off-ramp into and out of the crypto world. It’s also the main way bitcoin miners sell their bitcoin for yuan.

Recently, as part of a move to curtail internet gambling and contain capital outflows, Chinese authorities have been targeting OTC desks. If authorities determine that your counterpart (the person on the other end of your trade) is trying to launder illicit funds, you risk getting your bank account frozen. As a result, miners may be having to take more precautions and cash out less frequently, according to The Block (paywalled).

There is some speculation that this is making it harder for bitcoin miners to offload their bitcoins, leading to a liquidity crisis. In other words, fewer bitcoin are available to buyers, thus driving up demand similar to if hoards of bitcoin were being bought up by Tether.

But ICSI’s Weaver cautions there is no way to think rationally about bitcoin’s price. “The market is completely loony,” he said.

In a rational world, he believes shutting down OTC desks would have no effect on the price of bitcoin — if the rest of the markets were efficient and honest. OTC desks are really about miners’ paying power and Chinese who want to evade capital controls by trading cash for bitcoin and moving that bitcoin overseas, he said. He added that he could envision China’s crackdown on OTC desks driving up the price of bitcoin if it resulted in fewer OTC purchasers selling their bitcoin on banked exchanges. “But really, that doesn’t make sense either,” he said. “How many banked exchanges are left?”

Updated on Nov. 21 to mention that nobody has ever redeemed their tethers, meaning there is no record of anyone having sent their USDT back to Tether and received a bank wire for cash.

If you like my work, please consider supporting my writing by subscribing to my Patreon account for as little as $5 a month.

Bitcoin broke $16,000 on Thursday. That’s up from $10,000 in early September. And yet, with all the media outlets rabidly covering the latest “Bitcoin bull run,” the only one mentioning the billions and billions of dollars worth of tether (USDT) entering the market was Cointelegraph.

In particular, none of the mainstream press has bothered to mention tether in their writings about BTC’s recent price rise. This is worrisome because retail folks — the ones most vulnerable to risky investments — have little understanding of tether and the risk it imposes on Bitcoin’s price.

Instead, most media pointed to the election, PayPal’s recent embrace of crypto and huge BTC investments by MicroStrategy and Square as the reasons for BTC’s moon. Mainstream adoption! Institutional money! The truth is, crypto markets are easy to manipulate. And when BTC goes up in value like this, the main benefit is so early investors can cash out.

In other words, BTC gets passed on to the next bright-eyed, bushy-tailed dupe who hopes the price will continue skyward. History has shown, however, these bubbles are generally followed by a crash, and a lot of people getting hurt, which is exactly what happened in 2018.

Trolly McTrollface (not his real name, obvs) points out in a tweet thread that Tether went into hyperdrive in March to stop BTC from crashing. BTC had dropped to $5,000, losing half its value from two months prior. In fact, March is when BTC entered its current bull run phase.

During the bloodbath of March – May 2020, Tether created 4B new USDT. These issuances marked turning points in $BTC – namely, stopping the crash, and pumping prices back up. It was a coordinated action between Tether and exchanges. A thread.

Remember, if the price of BTC falls too low, the network’s miners — who are responsible for Bitcoin’s security — can’t make a profit, and that puts the entire network in danger.

Trolly believes the current price pump is a coordinated effort between Tether — which has now issued a jaw-dropping $18 billion worth of dollar-pegged tethers — and the exchanges.

Let’s talk about some of those exchanges.

OKEx withdrawals still frozen

Withdrawals from OKEx, one of the biggest crypto exchanges, have been frozen ever since the news came out that founder “Star” Xu was hauled away for questioning by Shanghai authorities more than a month ago.

Xu’s interrogation appears to be part of a broader crackdown on money laundering in China, though OKEx denies any AML violations.

OKEx is registered in Malta, but retains offices in Shanghai and Beijing, where it facilitates peer-to-peer—or “over-the-counter”—trades. The exchange acts as an escrow to reduce counter-party risk in fiat-to-crypto trades, so you don’t have to worry about someone disappearing with your cash before they hand over the BTC you just bought from them.

As Wolfie Zhao explains for the Block, these OTC trades are the only fiat on/off ramp for Chinese crypto traders—and have been ever since September 2017 when the country banned crypto trading on exchanges.

Effectively, the government made it so the exchanges could no longer get access to banking in the country.

P2P allows two people to transact directly, thus bypassing the Chinese ban, as long as the trades are small in scale. All Chinese crypto-to-fiat is OTC, while crypto-to-crypto trades are still done via a matching order book. (A Chinese citizen simply needs to use a VPN to access Binance, for instance.)

Currently, the OTC desk is the only trading desk that remains open at OKEx All of its exchange trading activity has been ground to a halt. The exchange claims Xu has access to the private keys needed to access its funds, and until he is free, all that crypto sits locked in a virtual vault.

As a result, according to blockchain analytics firm Glassnode, there are currently 200,000 bitcoin stuck on OKEx. The exchange insists all funds are safe, and says, essentially, that everything will be fine as soon as Xu returns. But its customers remain anxious. Did I mention OKEx is a tether exchange?

Update Nov 12:

Withdrawals remain suspended with user funds safe & unaffected: https://t.co/1fxZsOj6Cj@OKEx Microstructure report, Oct: https://t.co/AlPCGjVofC – OKEx sees highest OI for BTC & ETH futures at $1.1B & $240M – #DeFi trading volume remains stable

Like OKEx, Huobi is another exchange that moved its main offices out of China following the country’s 2017 crackdown on crypto exchanges.

Huobi, now based in Singapore, continues to facilitate fiat-to-bitcoin and fiat-to-tether trades in China behind an OTC front. (Dovey Wan does a nice job explaining how this works in her August 2019 story for Coindesk.)

Since earlier this month, rumors have circulated that Robin Zhu, Huobi’s chief operating officer, was also dragged in for questioning by Chinese authorities. Huobi denies the rumors.

Meanwhile, since Nov. 2—the day Zhu was said to have gone missing —$300 million worth of BTC has flowed from Huobi to Binance, according to a report in Coindesk. (I still don’t have a good explanation as to why Huobi is doing this. If anyone can fill in the gaps, please DM me on Twitter.)

What’s up with Binance?

If you follow Whale Alert on Twitter, like I do, it’s hard to ignore the enormous influx of tether going into Binance multiple times a day.

Here’s an example: On Friday, in four separate transactions, Tether sent Binance a total of $101 million worth of tethers. The day prior to that, Tether sent Binance $118 million in tethers, and the exchange also received $90 million worth of tethers from an unknown wallet. And on Wednesday, Tether sent Binance $104 million in tethers.

That’s over $400 million worth of dubiously backed tethers—in three days.

Reggie Fowler, the Arizona businessman in the midst of the Crypto Capital scandal, is running low on cash. His lawyers have decided they don’t do pro bono work, so now they want to drop him as a client.

Last month, Fowler’s legal team asked the court to change his bond conditions to free up credit. But apparently, that isn’t working. Unfortunately, all this is happening just when there was a possibility of negotiating another plea deal. (Read my blog posts here and here.)

Quadriga Trustee releases report #7

EY, the trustee handling the bankruptcy for failed Canadian crypto exchange QuadrigaCX, released its 7th Report of the Monitor on Nov. 5.

According to the report, EY has received 17,053 claims totaling somewhere between CA$224 million and CA$290 million—depending on what exchange rate EY ends up using to convert the USD and crypto claims to Canadian dollars for disbursement.

EY has CA$39 million ready to distribute to affected Quadriga users, who submitted claims. But none of that money is going anywhere until the Canadian Revenue Agency finishes its audit of the exchange. (Ready my blog post for more details.)

Gensler goes to Washington

Gary Gensler has been picked to lead President-elect Joe Biden’s financial reform transition team. As Foreign Policy notes, Gensler, who was the head of the CFTC during the Obama years, is an aggressive regulator.

He is also well familiar with the world of crypto. He taught a course on blockchain at MIT Sloan. He suspects Ripple is a noncompliant security, and he told me in an interview for Decrypt that the SAFT construct—a once-popular idea for launching an initial coin offering—will not spare a token from securities laws. (He also thinks 99% of all ICOs are securities.)

Libra Shrugged author David Gerard said in a tweet that Gensler was excellent in the Libra hearing last July. Gensler also “helped clean up the 2008 financial crisis, he knows literally all the possible nonsense,” said Gerard.

Clearly, this is good news for bitcoin.

Gensler was *excellent* in the Libra hearing last July (see the book). He helped clean up after the 2008 financial crisis, he knows literally all the possible nonsense https://t.co/zdo1kgNF5H

Nov. 15 — Before I said that OKEx offered the only fiat-to-crypto on/off ramp in China. That is inaccurate. P2P OTC exchanges *in general* are the only fiat on/off ramps for crypto traders in China and have been since Sept. 2017.

Nov. 16 — Previously, this story stated that Quadriga’s trustee has CA$30 million available to distribute to claimants. It’s been updated to correctly reflect that EY has CA$39 million (US$30 million) to distribute.

Reginald Fowler’s lawyers confirmed that money is indeed at the center of a conflict between them and their client — and the main reason why they want to withdraw from the case.

The news was revealed Friday in a telephone status call attended by Assistant US Attorneys Jessica Greenwood, Sheb Swett and Sam Rothschild; Fowler’s defense team, James McGovern, Michael Hefter, and Sam Rackear of Hogan Lovells, and Scott Rosenblum of Rosenblum Schwartz & Fry; and Fowler himself.

Fowler, a former NFL investor — who resides in Chandler, Arizona, and is free on bail — is accused of setting up a shadow banking service that has been linked to Crypto Capital, a Panamanian firm at the center of the New York Attorney General’s investigation into crypto firms Bitfinex and Tether.

As I wrote earlier, Fowler’s defense counsel have been careful about disclosing details on why they want to ditch their client, who they have been working with since Fowler was indicted in April 2019.

District Judge Andrew Carter began the call: “Defense, can you give me a little further elucidation regarding the grounds for your seeking to be relieved without getting into any privileged or confidential materials?”

Fowler’s attorney McGovern said the matter involved privileged and confidential information but added: “I think it is fair to say that it is of the nature that the government assumes in their filing, of a fee-based nature.”

Judge Carter cut straight to the heart of the matter: “So it is fair to say, without getting into the details, this is about lawyers not getting paid?”

“Yes,” McGovern answered, but added it was “a little bit more than that.” He then suggested that his team file an ex-parte submission setting out the nature and specifics of the request to withdraw. “That way, we’ll provide the court with a substantial amount of information that will provide color for the entire discussion,” he said.

Fowler is represented by two legal firms. Carter asked if the nature of the conflict was the same for both firms. “Yes,” responded Rosenblum, Fowler’s attorney at the second law firm.

Federal prosecutors have argued that Fowler’s defense can’t simply withdraw from the case without giving some type of explanation.

US Assistant Attorney Greenwood reiterated that argument, telling the judge that “there are significant portions of a fee arrangement that are not potentially privileged.” She suggested Fowler’s attorneys provide details in an ex-parte and then allow the government to access the non-privileged portions “so we can appropriately respond to the motion to withdraw.”

Judge Carter agreed to allow Fowler’s defense team to file a submission under seal. “Once I receive those materials,” he said, “I will make a determination as to whether or not the document will remain under seal or whether or not there are portions that can, in fact, and should, in fact, be redacted and other portions that should be made public.”

The defense counsel said they would submit the document on Nov. 18.

So where is Fowler’s money?

Fowler has been having money problems for a while—problems that extend back to when the US Department of Justice froze his bank accounts in late 2018, leading to the collapse of the Alliance of American Football, a new football league that he cofounded and was a major investor in.

From there, things seem to have gotten worse.

Recall that in January 2020, Fowler rejected a plea deal that would have required him to forfeit $371 million. It was the forfeiture requirements that blew up the deal. Prosecutors hit back with a superseding indictment that added a new count: wire fraud.

On October 15, Law360, reported that Fowler’s legal team might be open to exploring for a second time potential options to resolve the charges, even though the new wire fraud charge complicated things.

And then, on October 23, Fowler’s defense team went to the court seeking to modify conditions of his bond so that he could pay for his defense. (Here is the original May 2019 bond conditions; here is their request for a change.)

Specifically, they wanted to change the bond conditions to enable Fowler to take credit out on properties he had acquired prior to February 2018 “when the alleged conspiracy began” without approval from pretrial services. And to remove the five properties posted as security for the $5 million bond.

Those properties, based on a rough estimate of looking at them on Zillow, are probably only worth around $1.5 million total.

Whatever happened after that — it clearly wasn’t enough to satisfy his attorneys.

Updated Nov. 14 to add the bit about Fowler’s accounts getting frozen in 2018 and the AAF.

Reginald Fowler, the Arizona, businessman allegedly linked to hundreds of million of dollars in missing Crypto Capital funds, is about to lose his defense team. Did he neglect to pay them?

And knowing who their client was, did his lawyers ask for a large enough retainer in the event that something unexpected like, say, a superseding indictment might extend their work?

Crypto Capital is the payment processor that Tether and Bitfinex—and several other cryptocurrency firms—used to shuttle money around the globe as a workaround to the traditional banking system. Fowler allegedly helped out by opening up a network of bank accounts for them.

We can only guess the real reason Fowler’s lawyers are keen to drop their client at the moment, but court docs may offer clues. Here is the backstory:

Earlier this week, Fowler’s attorneys—James McGovern and Michael Hefter of Hogan Lovells US LLP—asked a New York judge for permission to withdraw from the case. (Here is their motion to withdraw filed on Nov. 9.)

(Fowler is also represented by Scott Rosenblum of Rosenblum Schwartz & Fry PC, though Rosenblum’s name is not on the motion.)

The lawyers claim they initially told Fowler their reasons for wanting to quit on February 26—coincidentally, just five days after the government added a fifth charge against Fowler in its superseding indictment and a month after Fowler forfeited on a reasonable sounding plea bargain.

In the months follower, the legal team informed Fowler both “orally and in writing on multiple occasions” of their grounds for wanting to withdraw. Now, after much back and forth, they have had enough: they are asking the court for permission to drop him.

McGovern and Hefter don’t offer a specific reason for wanting to quit in their motion, citing attorney-client privileged. But they argue the case has had “limited pertinent discovery,” Fowler has had ample time to find new counsel, and essentially, the case should go on just fine without them.

Federal prosecutors are not convinced. In a letter addressed to Andrew Carter, the Southern District of New York judge overseeing the case, they argue the defense counsel has’t presented enough facts for the court to decide on the motion. (Here is their response filed on Nov. 12.)

Specifically, they dispute the “limited pertinent discovery” claim, saying the government has so far produced over 370,000 pages of discovery, much of which they have already discussed in detail with the defense counsel.

Further, they argue that if this is about a “fee dispute,” the court needs to weigh other factors, such as “nonprivileged facts” about the fee arrangement, including whether a “more careful or prudent approach to the retainer agreement might have avoided the current problem”—i.e., McGovern and Hefter should have insisted on more money up front.

Finally, they claim that if Fowler’s lawyers’ leaving further delays the trial, the court should not allow it. After two postponements, the trial is currently scheduled for April 12, 2021. (It was originally slated to begin on April 28, 2020, and then got moved to January 11, 2021, before the current trial date.)

“Now, approximately five months before the current trial date, defense counsel seeks to withdraw from this matter based on facts they claim were discussed with the defendant as early as February 26, 2020—nearly nine months ago and before both prior adjournments in this case,” federal prosecutors said. “The current motions should be denied if allowing counsel to withdraw at this late stage would further delay trial.”

It’s no fun when the money’s all gone. Two weeks after Polish crypto exchange Bitmarket shut down due to “lack of liquidity,” the lifeless body of its CEO, Tobiasz Niemir, turned up in the woods. It’s not clear if he fell in with shady characters or he put that bullet in his head all by himself.

Here is an interviewwith Niemer done shortly before his death.

You remember BTC-e, the crypto exchange that was shut down in mid-2017? The U.S. is now suing the exchange and its operator Alexander Vinnik to recover penalties of $100 million imposed by FinCEN for allegedly violating the Bank Secrecy Act. Vinnik, a Russian national, is facing extradition requests from both the U.S. and Russia. (Here are the court docs.)

Binance has been shilling its centralized BNB token. The crypto exchange regularly burns (destroys) large numbers of the token to increase the value of whatever is left. The BNB burn is “meaningless nonsense to fool suckers,” writes David Gerard. “Anyone taking Binance posts about BNB seriously as any sort of trading signal is dumb enough to trade literally any shitcoin they see, and probably deserves to.”

The hearing for Reggie Fowler, the AAF investor tied to Bitfinex’s missing $850 million, has been moved to December. (Here are the court docs.) Also, recall that he was released on $5 million bail secured by several pieces of cheap real estate and two financially responsible people. Who were his wealthy friends? A source tells me it was his ex-wife Lori Fowler and Molly Stark, the director of Spiral Volleyball, a company he owned. It pays to stay on good terms with your exes.

(Update Dec. 22: Lori Fowler and Molly Stark signed the court documents for his release.)

Bitfinex and Tether filed court docs arguing once again that they are not doing any business in New York and tether is not a security. (Here is Bitfinex counsel Stuart Hoegner’s affidavit and an accompanying memorandum of law submitted by the company’s outside counsel). It all boils down to “yeah, but, no, but yeah.” We’ll hear from the judge on Monday, July 29 as to what he thinks.

Big whoops: Swedish crypto exchange Quickbit says it has leaked the data of 300,000 customers. According to the exchange, a third-party contractor left the data unprotected while upgrading on the exchange’s servers.

Elsewere in cryptoland

After bidding an astounding $4.5 million in a charity auction for the privilege to have lunch with billionaire Warren Buffet, Tron CEO Justin Sun cancelled last minute, claiming a bad case of kidney stones. But come to find out Sun’s been on the lam from China since November 2018. He is living in San Francisco now, which was where the lunch was supposed to have taken place.

Sun was, however, feeling well enough to attend the Tron after-party on July 25, even though nothing actually happened before the party, since lunch was cancelled.

According to Chia founder Bram Cohen, Sun also forgot to make a scheduled payment as part of Tron’s mid-2018 acquisition of file sharing service BitTorrent. Someone needs to explain to Bram that kidney stones can take a lot out of a person.

Anybody know if Justin Sun is hard up for cash? He isn't letting the last payment for BitTorrent get out of escrow.

In other news, the IRS is sending out scary letters to bitcoin holders, reminding them that they need to report any gains in crypto trading and pay their taxes. “Taxpayers should take these letters very seriously, IRS Commissioner Chuck Rettig said.

How did the IRS get all this info? Previously, a court ordered Coinbase to hand over the personal identifying information of customers who had transactions of $20,000 or more on the exchange between 2013 to 2015.

An MIT fellow thinks the structure of Facebook’s Libra was lifted verbatim from a paper that he and two other scholars published last year. What say you, Facebook? Are you stealing people’s ideas? It’s not like you’ve done anything like that in the past.

On the subject of Libra, one of the big selling points of the project was that it had 27 partners backing the project. But the CEO of Visa reminds us, no companies have officially joined yet. They’ve only signed non-binding letters of intent.

Telegram is under the gun. The popular messaging service has sold $1.7 billion worth of its Gram tokens to investors. Now it needs to build a Gram wallet into Messenger by October or give all the money back — and we’re sure it doesn’t want to do that.

Finally, Sergey Ivancheglo (aka “Come from Beyond”), the founder of IOTA and one of the project’s core developers, quit the IOTA Foundation. The two remaining directors are non-developers, but we’re sure they’ll handle everything just fine on their own. Nice bunch of people, really.

Since I’m now the editor of an ATM website, let’s start with bitcoin ATM news. LibertyX is adding 90 machines to its bitcoin ATM network. It now has over 1,000 machines.

Actually, these are not new machines. They are traditional cash ATMs that are bitcoin enabled. A software upgrade on the machines allows users to buy bitcoin with a debit card. The ATMs continue to dispense cash as well.

According to CoinATM Radar, there are now 5,200 bitcoin ATM machines on this earth. Who the heck is using them? At least one operator, frustrated by a lack of business, has moved his Bitcoin ATM into his mother’s garage.

In the exchange world —

Dmitri Vasilev, the ex CEO of defunct crypto trading platform Wex, was arrested in Italy. Wex was a rebrand of BTC-e, an exchange that was shut down in 2017 for being a hub of criminal activity. BTC-e was also linked to the stolen bitcoin from Mt. Gox.

Economist Nouriel Roubini — aka “Dr. Doom” — has stepped up his attack on crypto derivatives exchange BitMEX. In a scathing column in Project Syndicate, Roubini claims sources told him the exchange is being used daily for “money laundering on a massive scale by terrorists and other criminals from Russia, Iran, and elsewhere.”

Days after Roubini’s column came out, Bloomberg reported that the CFTC was investigating whether BitMEX allowed Americans to trade on the platform. In fact, we know that crypto analyst Tone Vays, a New York resident, was trading on the platform until November 2018 when his account was terminated.

Regulators are cracking down on crypto exchanges. As The Block’s Larry Cermak points out, the situation is getting “quite serious.”

This is getting quite serious. Let's summarize:

– Both BitMEX and Bitfinex are now investigated for servicing U.S. customers

– Bittrex and Poloniex started to geo-block tokens from the U.S.

– Binance pulled crypto-to-crypto trading out of the U.S. completely

Elsewhere, Bitpoint, the Tokyo-based crypto exchange that was recently hacked, says it will fully refund victims in crypto, not cash. Roughly 50,000 users were impacted when $28 million worth of crypto vanished off the exchange. Two-thirds of the stolen funds belonged to customers of the exchange.

U.S. crypto exchange Coinbase has killed off its loss-making crypto investment packages. After shutting down its crypto index fund due to a lack of interest, it closed its much ridiculed “Coinbase Bundle.” The product launched eight months ago with the aim of making it easy to purchase a market-weighted basket of cryptocurrencies.

Malta-based Binance found itself $775,000 richer when it stumbled across nearly 10 million Stellar lumens (XLM). Turns out, the exchange had been accidentally staking (receiving dividends) on its customers lumens for almost a year. It’s planning to give the tokens away in an airdrop and will also add staking support for customers.

Tether, the stablecoin issued by Bitfinex/Tether, is now running on Algorand, a new blockchain protocol. It’s also running on Omni, Ethereum, Tron and EOS. Presumably, running on a plethora of networks makes tether that much harder to shut down. It’s sort of like whack-a-mole. Try to take it off one network, and tether reappears on another.

There are now officially more than $4 billion worth of tether sloshing around in the crypto markets. That number almost doubled when Tether inadvertently issued $5 billion unbacked tethers when it was helping Boston-based crypto exchange Poloniex transfer tethers from Omni to Tron. Oops.

Also interesting —

David Gerard is working on a book about the world’s worst initial coin offerings. He recently uncovered another cringe-worthy project. “Synthestech was an ICO to fund research into transmutation of elements, using cold fusion — turning copper into platinum. Literally, an ICO for alchemy. Turning your gold into their gold.”

Facebook’s Libra had a busy week.

U.S. Secretary of Treasury Steven Mnuchin gave a press briefing on crypto at the White House. (Here’s the transcript.) He is concerned about the speculative nature of bitcoin. He’s also seriously worried Libra will be used for money laundering. He said the project has a long, long way to go, before he feels comfortable with it.

Unlike bitcoin, which goes wildly up and down in price, Libra would have a stable value, because it would be pegged to a basket of major currencies, like the dollar, euro, and yen. Although, nobody is quite sure how that will work and what currencies it will be pegged to. Tether has a stable value, too, of course.

After his talk, Mnuchin flew off to Paris, where he met with finance ministers from six other powerful countries at the G7 summit. Everyone there agreed they need to push for the highest standards of regulation on Libra.

Meanwhile, David Marcus, the head of the Libra project, got a grilling in Congress over privacy and trust issues. (You can watch the Senate hearing here and the House Financial Services Committee hearing here.) Nobody believes Facebook will keep its word on anything.

All of this is happening, of course, just after the social media giant got a $5 billion slap on the wrist for privacy violations following the Cambridge Analytica scandal.

What we learned from today's senate hearing and grilling of Mr. Marcus: + A bunch of Senators hate FB + A couple of them think the tech could be cool + Senators attuned to in weeds issues (Warner a good example) + Marcus is a skilled operator + There will be more hearings

The dumb tweet of the week award goes to Anthony Pompliano, co-founder of a digital asset fund Morgan Creek Digital, who says dollars aren’t moved digitally, they are moved electronically. For some reason, he has 250,000 followers on Twitter. The historic tweet even made it in FT Alphaville.

They aren’t moved digitally. They are moved electronically. That is why it takes so long for you to settle dollar transactions between banks for example. Small, but very important difference.

Apple co-founder Steve Wozniak has joined an energy-focused blockchain startup in Malta. The Mediterranean island nation is gung-ho about blockchain. It is also a haven for money laundering and the place where a female journalist who tried to expose government corruption was blown up in 2017.

U.S authorities have charged former Silk Road narcotics vendor Hugh Brian Haney with money laundering. The darknet market was shut down in 2013. Special agents used blockchain analytics to track down Haney and seize $19 million worth of bitcoin.

This clever young man has made a business out of helping crypto exchanges inflate their volume.

ConsenSys founder Joseph Lubin is being sued by a former employee for $13 million. The employer is alleging fraud, breach of contract and unpaid profits.

Former bitcoin core developer Peter Todd is being sued for allegedly touching people inappropriately.

And finally, bitcoin ransomware Ryuk is steadily making its way into China.

This newsletter is reader supported. If you appreciate my work enough to buy me a beer or cup of coffee once a month, that’s all it costs to become a patron. I’m trying to pick up freelance gigs when I can, but one of the joys of writing for my own blog is I can write whatever I want, when I want. On to the news…

Bitfinex and LEO

UNIS SED LEO, the full name of Bitfinex’s shiny new utility token, is in its second week of trading. The price started at around $1, but it’s already climbed to a high of $1.52, according to CoinGecko. I’m sure the price increase is totally organic—not.

There are 1 billion LEO in circulation—660 million issued on Ethereum and 340 million issued on the EOS blockchain.

Crypto Rank warns that 99.95% of LEO coins are owned by the top 100 holders. Also, Bitfinex still has not disclosed information about the investors. “We consider that the token can be manipulative,” Crypto Rank tweeted.

Given its $850 million shortfall, Bitfinex needs to pull in more money. It recently entered the initial exchange offering (IEO) business. IEOs are similar to initial coin offerings (ICOs), except that instead of handing you money directly to the token project, you give it to the exchange, which acts as a middleman and handles all of the due diligence.

Tethers

As the price of bitcoin goes up—at this moment, it is around $8,730—the number of tethers in circulation is going up, too. There are now more than $3 billion worth of tethers sloshing around in the crypto markets, pushing up the price of bitcoin.

Utter rubbish. It has skyrocketed for one reason only, and that is market manipulation by Bitfinex/Binance/Tether to recoup the $850m lost by Bitfinex and evade the NYAG's injunction. https://t.co/bHTgAWNx0O

— (((Frances Coppola))) (@Frances_Coppola) May 31, 2019

Omni tethers, Ethereum tethers, Tron tethers. Tethers appear to be constantly coming and going, bouncing from one chain to another. It gets confusing. But maybe that is the point—to keep us confused. And to add to the jumble, tethers are now executing on EOS.

. @Tether_to is launching on a new chain today. Any guess? I believe that cross-chain support is a key element for the success of a stable-coin.

In the next couple of weeks, Tether is also planning to issue tethers on Blockstream’s federated sidechain Liquid. And later this year, the Lightning Network.

I updated my recent tether story to note that if you want to redeem your tethers via Tether, there is a minimum redemption of $100,000 worth—small detail. Also, I still haven’t found anyone who has actually redeemed their tethers.

Cryptopia’s data—held to ransom?

Cryptopia filed for liquidation on May 14. Liquidator Grant Thornton New Zealand is now scrambling to save the exchange’s data, held on servers hosted by PhoenixNAP in Arizona. The tech services wants $1.9 million to hand over the data.

Grant Thornton is worried Phoenix will erase the SQL database containing critical details of who owned what on the exchange. It filed for Chapter 15 and provisional relief in the Bankruptcy Court of the Southern District of New York. (Here is the motion.)

According to the motion, Cryptopia paid Phoenix for services through April. But when it offered to pay for May, Phoenix ended the service contract and “sought to extract” $1.9 million from the exchange. Grant Thornton says only $137,000 was due for the month of May. Phoenix also denied the liquidators access to the data.