Tether, the world’s most popular stablecoin issuer, released a breakdown of the composition of its reserves backing tethers on May 13.

The breakdown is no surprise to Tether followers: Two lame pie charts showing, at best, only a fraction of assets are in cash, and the rest are in risky assets.

Specifically, this is a breakdown of the composition of Tether’s reserves on March 31, 2021, when Tether had roughly 41.7 billion tethers in circulation. (As of this writing, Tether now has nearly 58 billion tethers in circulation.)

According to its settlement agreement with the NY AG, Tether must issue these breakdowns quarterly for two years—though it may have to provide more detail to the NY AG, in addition to what it has made public today.

Let’s take a closer look at the two pie charts. (This information may be updated, as I get more feedback.)

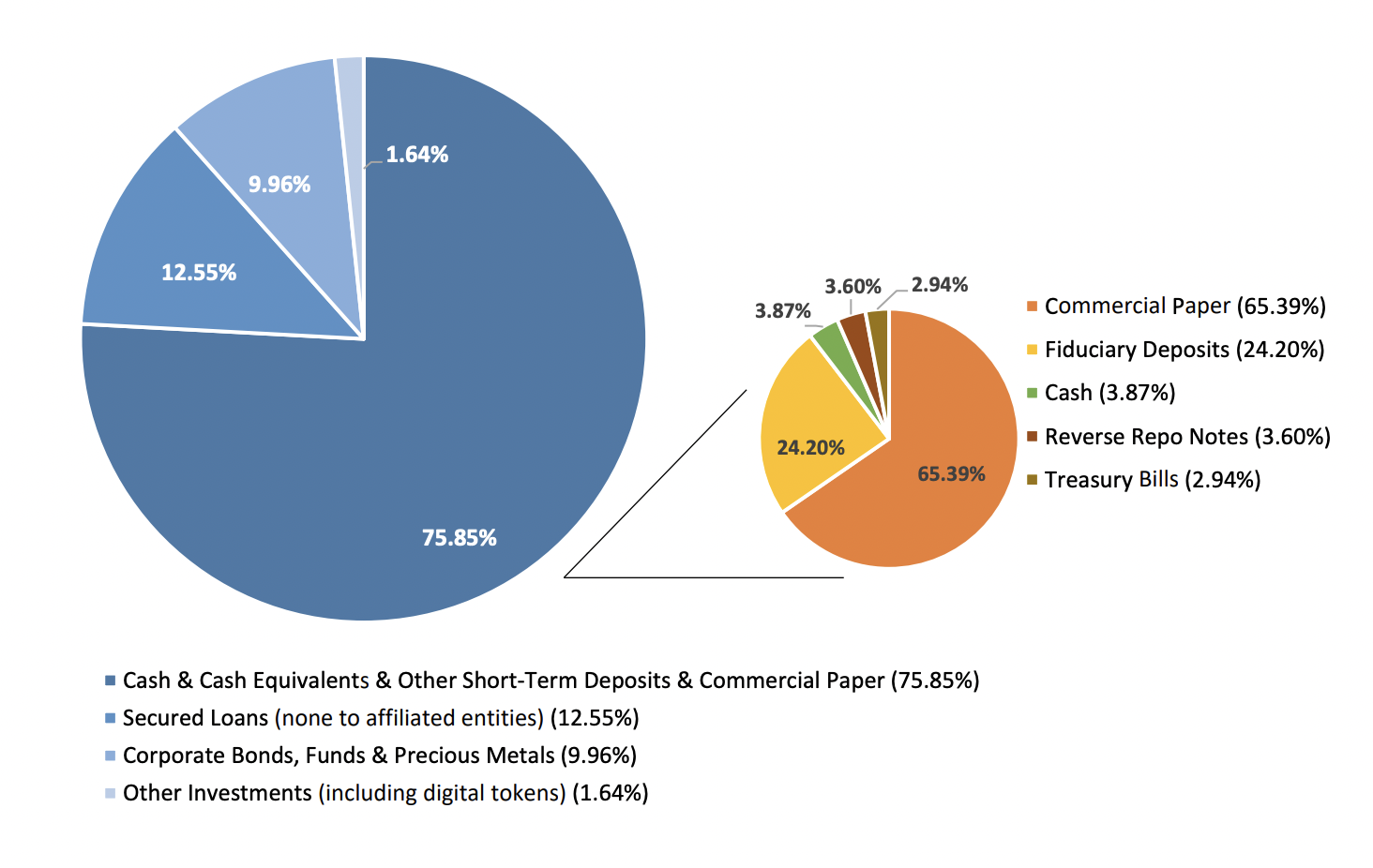

The blue pie chart

According to the first pie chart—the blue one—the majority of Tether’s assets (nearly 76%) are socked away in cash and cash equivalents. (Tether breaks all this down in a second chart, which I’ll get to in a moment. Hint: these can barely be considered cash equivalents.)

But first, let’s look at what else is here:

12.55% is in secured loans — Loans to who, secured by what? We have no idea. These could well be loans to large tether customers backed by shitcoins, other worthless assets, or promissory notes.

9.96% is in corporate bonds, funds, and precious metals — A corporate bond is a bond issued by a corporation in order to raise financing. The question is, who is issuing these bonds? If it is a blue chip company, great. But if it’s some dodgy crypto start-up, these are likely worthless.

1.64% is in other investments, including digital currency — Tether wants us to believe that only a fraction of Tether’s reserves are in bitcoin. (Tether/Bitfinex general counsel Stuart Hoegner told The Block that “digital tokens” refers exclusively to bitcoin.) I have a funny feeling Tether will get into a great deal of trouble if it admits to using tethers to purchase bitcoin en masse. (Recall this interview, where Hoegner completely avoids the question pertaining to, are you using tethers to buy bitcoin?”)

The orange pie chart

Tether further breaks down the largest slice of its blue pie chart—which shows that more than three-quarters of its reserves are in cash and cash equivalents. Just a tiny bit is in cash and there’s a big question as to whether any of the non-cash items are cash equivalents at all.

Here’s how Tether divvies it up:

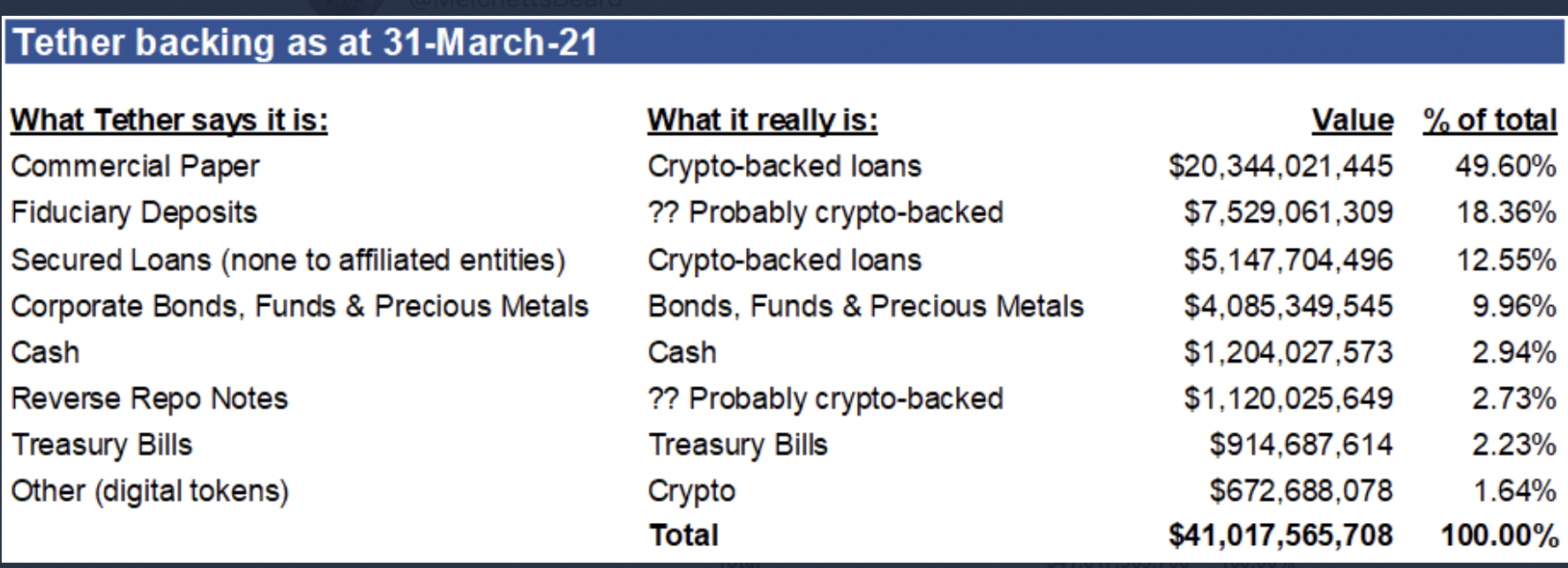

65.39% is commercial paper — Commercial paper refers to a short-term loan for up to 12 months. It is similar to a bond in that you have the ability to transfer and trade it. The problem is we don’t know who the issuer of the commercial paper is. If it’s IBM or Amazon, that’s as good as cash. But if Tether is giving tethers away to their largest customers (FTX, Binance) and counting that as loans, this is meaningless rubbish.

Frances Coppola, an economist and bitcoin skeptic, suggests Tether’s commercial paper is probably unsecured. “In which case it is NOT a ‘cash equivalent’ as the analysis says. It’s a current asset with significant credit risk.”

25.2% is fiduciary deposits — These are deposits placed by a customer with a third bank (recipient bank) through an agent bank. Who are the holders of these fiduciary deposits? We have no idea.

3.87% is cash — This is such a tiny bit of cash. What happened to all the cash backing tethers? Recall that up until a few years ago, Tether maintained tethers were fully backed by cash.

3.6% is reverse repo notes — This appears to be a made-up term. Martin Walker, a director for banking and finance at the Center for Evidence-Based Management, isn’t familiar with the term either. “I’ve never heard of a Reverse Repo Note before, and I am the product manager for a couple of repo trading systems and used to run repo technology at an investment bank,” he said in a private chat.

2.94% is treasury bills — T-bills are a short-term financial instrument issued by the U.S. Treasury with maturity periods from a few days up to 52 weeks. These are as good as cash. In fact, this is the only slice of pie, other than cash, that can be considered cash.

The bottom line

For a company with nearly $60 billion in assets, these pie charts are pathetic. I’m sure the folks at the Office of the NY AG are rolling their eyes. The only thing backing tethers is once again, smoke and mirrors.

To be clear, Tether has no obligation to redeem any money in the Tether bank accounts. Per its terms of service:

“Tether reserves the right to delay the redemption or withdrawal of Tether Tokens if such delay is necessitated by the illiquidity or unavailability or loss of any Reserves held by Tether to back the Tether Tokens, and Tether reserves the right to redeem Tether Tokens by in-kind redemptions of securities and other assets held in the Reserves. Tether makes no representations or warranties about whether Tether Tokens that may be traded on the Site may be traded on the Site at any point in the future, if at all.”

With that in mind, we may as well consider these pie charts a window into the personal bank accounts of the Tether/Bitfinex triad. The crumbs of remaining cash? It is just their “bonus” money that they haven’t withdrawn yet.

Jorge Stolfi, a computer scientist from Brazil, quoted privately: “If someday [Tether/Bitfinex] get tired of making real money with their sucker mining machine, they can just close Tether Inc and divide its assets among them. They won’t even have to leave the traditional crypto good-bye word on their website.”

David Gerard offers further analysis of Tether’s pie charts.

Related stories:

The curious case of Tether—a complete timeline of events

Updates on March 13— Added quote from Martin C. Walker on Reverse repo notes, as even he is not familiar with the term. Defined treasury bills, and noted they are the only cash equivalent in the mix, and added Trolly’s brilliant tweet. Also, added a link to Gerard’s post and later, the graph.

If you enjoy my work, please support my writing by becoming a patron.

As far as “Reverse Repo Notes”, maybe they mean Reverse Repo Agreement? Meaning some other entity has sold them collateral (of what kind?) with the agreement that the other entity will buy them back later with interest? Their risk on that portion will be based on the collateral that is being used to back them. If it is crypto, it may as well be more unsecured lending. But I have no idea – just spitballing.