Are the pixie fairies sprinkling gold dust on bitcoin’s market again? By the looks of things, you might think so.

Like in the bubble days of 2017, the price of bitcoin is headed ever upward. On November 18, 2020, it surpassed $18,000 — a number not seen since December 2017 when bitcoin, at its all-time peak, scratched $20,000.

Of course, the market crashed spectacularly the following year, and retailers lost their shirts. But here we are once again, trying to unravel the mysteries of bitcoin’s latest price movements.

Several factors may explain it — Tether, PayPal, and China’s crackdown on over-the-counter desks — but before we get into that, let me reiterate how critical it is for bitcoin’s price to stay at or above a certain magic number.

Bitcoin miners — those responsible for securing the bitcoin network by “mining” the next block of transactions on the blockchain — need to sell their newly minted bitcoins for real money, so they can pay their massive energy bills.

Roughly $8 million to $10 million in cash gets sucked out of the bitcoin ecosystem this way every day. So, in order for the miners — the majority of whom are in China — to turn a profit, bitcoin needs to be priced accordingly. Otherwise, if too many miners were to decide to call it quits and unplug from the network all at once, that would leave bitcoin vulnerable to attacks. The entire system, and its current $345 billion market cap, literally depends on keeping the miners happy.

Now let’s jump to May 11, an important day for bitcoin. That was the day of the “halvening,” an event hardwired into bitcoin’s code where the block reward gets slashed in half. A halvening occurs once every four years.

Before May 11, miners received 1,800 bitcoin a day in the form of block rewards, which meant they needed to cash in each bitcoin for $5,000. But after the halvening, the network would produce only 900 bitcoins per day, so miners knew they needed to sell each precious bitcoin for at least $10,000.

But trouble loomed. Just months before the halvening, the price of bitcoin went into free fall. Between February and March, when the world was first gripped by the COVID crisis, bitcoin lost half its value, dropping to a low of $3,858 on March 13 — barely enough to pay the system’s energy costs post-halvening. Miners were likely pacing, wringing their hands, wondering how they would stay in business. Who would guarantee their profits?

That is when Tether — a company that produces a dollar-pegged stablecoin of the same name — sprung into action and started issuing tethers in amounts far greater than it ever had before in its five years of existence.

Tethers, for the uninitiated, are the main source of liquidity for unbanked crypto exchanges, which account for most of bitcoin’s trading volume. Currently, there are $18 billion (notional value) worth of tethers sloshing around in the crypto markets. And nobody is quite sure what’s backing them.

Due to Tether’s lack of transparency, its failure to provide a long promised audit, and the fact that the New York Attorney General is currently probing the firm along with Tether’s sister company, crypto exchange Bitfinex, for fraud, a good guess is nothing. Tethers, many suspect, are being minted out of thin air.

(Tethers were initially promised as an IOU where one tether was supposed to represent a redeemable dollar. But that was long before the British Virgin Island-registered firm began issuing tethers in massive quantities. And no tethers, to anyone’s knowledge, have ever been redeemed—except for when Tether burned 500 million tethers in October 2018, following the seizure of $850 million from its payment processor Crypto Capital.)

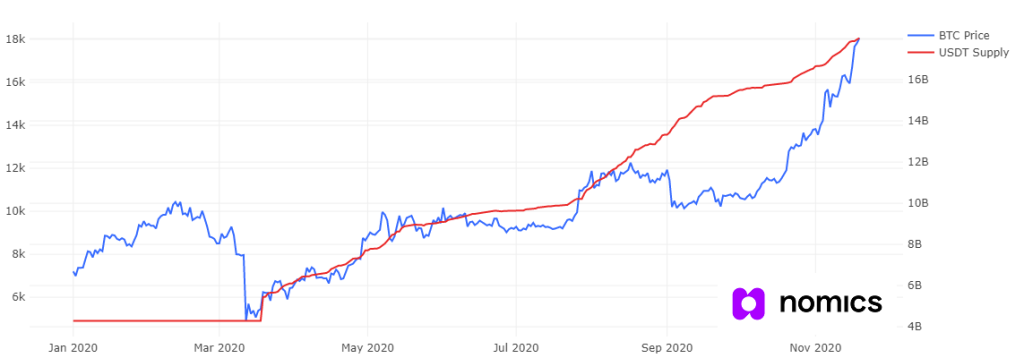

According to data from Nomics, at the beginning of 2020, there were only $4.3 billion worth of tethers in circulation. That number remained stable through January and February and into March. But starting on March 18, just five days after bitcoin dipped below $5,000, the tether printer kicked in.

Tether minted 4.4 billion tethers in April 2020 — crypto’s version of an economic stimulus package. By early June, the price of bitcoin crossed $10,000. Yet the Tether printer kept printing, pushing the price of bitcoin ever skyward and giving bag holders an opportunity to cash out.

In May, June, and July 2020, Tether issued a combined total of 3 billion tethers. In August, when the price of bitcoin reached $12,000, Tether issued another 2.6 billion tethers. In September, when bitcoin slid below $10,000, Tether infused the markets with another 2.2 billion tethers, although, even that couldn’t lift bitcoin up to $12,000 again. The price just hovered in the $10,000 range.

And then in October — just after US prosecutors charged the founders of BitMEX, a Seychelles-registered, Hong Kong-based bitcoin derivatives exchange, for failing to maintain an adequate anti-money laundering program — the price of BTC started to soar. What happened?

Tether’s frenzied pumping

One theory is that Tether just kept issuing tethers, billions and billions of them, and those tethers were used to buy up bitcoin. A high demand drives up the price — even if it’s fake money.

Only unlike in 2017, the effort to drive up bitcoin’s price is requiring a lot more tethers than ever before. (At the end of 2017, before the last bitcoin bubble popped, there were only $1.3 billion worth of tethers in circulation, a fraction of what there are today.)

Nicholas Weaver, a bitcoin skeptic and a researcher at the International Computer Science Institute in Berkeley, is convinced bitcoin’s latest price moves are 100% synthetic.

“The amount of tether flooding into the system is more than enough explanation for the price as it is well more than the amount needed to buy up all the newly minted bitcoin,” he told me. “If it was organic, there would at least be some significant increase in the outstanding amount of non-fraudulent stablecoins.”

What he means is, if real money was behind tether, we’d be seeing a similar demand for regulated stablecoins. But that is not the case. Only one regulated stablecoin has seen substantial growth — Circle’s USDC — but that growth is far overshadowed by Tether, and mainly a result of the growing decentralized finance (DeFi) market — a topic for another time.

Jorge Stolfi, a professor of computer science at the State University of Campinas in Brazil, who in 2016 wrote a letter to the SEC advising about the risks of a bitcoin ETF, which the SEC published, agrees.

“As long as fake money can be used to buy BTC, the price can be pumped to whatever levels to keep the miners happy,” he told me. He went on to explain in a Twitter thread that the higher the bitcoin price, the faster real money flows out of the system — assuming miners sell all their bitcoin for cash. Multiply bitcoin’s current price of $18,600 times 900, and that’s nearly $17 million a day. Investors will never get that money back, he said.

Klyith (not his real name) from Something Awful, a predecessor site to 4Chan, explains Tether this way:

“A bunch of pixies show up and start flooding the parchment market with fairy gold, driving prices to amazing new heights. But when any of the player characters try to spend the fairy gold in other towns or to pay tithes to the king, it turns into worthless rocks.

“If you denounce the pixies to the peasants or start using dispel magic to reveal that fairy gold is rocks, the price of parchments will collapse and the peasants may stop using them altogether. But if you ignore the pixies and keep the parchment economy going, you will end up with more and more worthless rocks instead of gold. The pixies can of course tell the difference between fairy gold and real gold at a glance. So they will quickly drain all the real gold from the whole township if you don’t act. What do you do?”

Still, it is hard to imagine that outside events don’t have some impact on bitcoin’s price. Two other events are being talked about right now as reasons behind bitcoin’s price gains—and they are getting a lot more media attention than Tether.

PayPal’s shilling

One of the biggest companies in the world is now promoting crypto, giving retail buyers the impression that bitcoin is a safe investment. After all, if bitcoin were a Ponzi or a scam, why would such a well-known, respectable company embrace it? I should add that MicroStrategy, Square, Fidelity Investment and Mexico’s third-richest person, Ricardo Salinas Pliego, are also currently shilling bitcoin on the internet.

On Oct. 21, PayPal announced a new service for its users to buy and sell crypto for cash. And on Nov. 12, the service became available to U.S. customers, who can now buy and sell bitcoin, bitcoin cash, ether, and litecoin via their PayPal wallet.

If you are a PayPal user, you have already gone through the process of proving you are who you say you are. And that removes the hassle of having to sign up with an crypto exchange, like Coinbase in the U.S., and take selfies of yourself holding up your driver’s license or passport.

Of course, there are limitations. You can’t transfer crypto into or out of your wallet, like you can on a centralized exchange. But you can pay PayPal’s 26 million merchants with crypto — although, not really, because what they receive on their end is cash. And the transaction is subject to high fees, like 2.3% for anything under $100, so what is the point? All you are doing is taking out a bet against PayPal that the price of bitcoin is going to rise.

Stolfi describes PayPal on Twitter as “a meta-casino where you can choose to use special in-house chips with a randomly variable value.”

The broader point is that PayPal makes it easy to buy crypto for people who are less likely to understand how crypto really works or know about Tether and the risk it imposes on the crypto markets. (If authorities were to arrest Tether’s operators and freeze its assets, similar to what happened to Liberty Reserve in 2013, that could lead to a huge plummet in bitcoin’s price.)

If you think Tether doesn’t have that big of an impact on bitcoin’s price, recall that Tether/Bitfinex CFO Giancarlo Devasini (going by “Merlin”) is recorded in the NYAG’s 2019 complaint as having reached out to Crypto Capital to plead for missing funds: “Please understand all this could be extremely dangerous for everybody, the entire crypto community,” said Merlin, indicating what could happen if Tether failed to exist. “BTC could tank to below 1k if we don’t act quickly.”

PayPal this month reached 85% of the volume of Binance.US, the U.S. branch of major crypto exchange Binance. Granted the volume of Binance.US is small in comparison with Binance’s main crypto exchange, but you can see where this is going.

One thought is that PayPal’s move into crypto is a “death sentence” for bitcoin, and that Tether and the exchanges who depend on tethers are working together to pump up the price of bitcoin to lure as much cash into the system as possible while the going is good.

China’s crackdown on OTC desks

According to news coming out of the country, China’s bitcoin miners may be encountering difficulty selling their bitcoin on over-the counter exchanges.

Since China banned crypto exchanges three years ago, OTC exchanges — where buyers and sellers go to trade directly — have become the most convenient way for the country’s citizens to on-ramp and off-ramp into and out of the crypto world. It’s also the main way bitcoin miners sell their bitcoin for yuan.

Recently, as part of a move to curtail internet gambling and contain capital outflows, Chinese authorities have been targeting OTC desks. If authorities determine that your counterpart (the person on the other end of your trade) is trying to launder illicit funds, you risk getting your bank account frozen. As a result, miners may be having to take more precautions and cash out less frequently, according to The Block (paywalled).

There is some speculation that this is making it harder for bitcoin miners to offload their bitcoins, leading to a liquidity crisis. In other words, fewer bitcoin are available to buyers, thus driving up demand similar to if hoards of bitcoin were being bought up by Tether.

But ICSI’s Weaver cautions there is no way to think rationally about bitcoin’s price. “The market is completely loony,” he said.

In a rational world, he believes shutting down OTC desks would have no effect on the price of bitcoin — if the rest of the markets were efficient and honest. OTC desks are really about miners’ paying power and Chinese who want to evade capital controls by trading cash for bitcoin and moving that bitcoin overseas, he said. He added that he could envision China’s crackdown on OTC desks driving up the price of bitcoin if it resulted in fewer OTC purchasers selling their bitcoin on banked exchanges. “But really, that doesn’t make sense either,” he said. “How many banked exchanges are left?”

Meanwhile, Tether keeps up the good work.

Updated on Nov. 21 to mention that nobody has ever redeemed their tethers, meaning there is no record of anyone having sent their USDT back to Tether and received a bank wire for cash.

If you like my work, please consider supporting my writing by subscribing to my Patreon account for as little as $5 a month.