Crypto markets are extremely volatile. You never know how wildly up or down the price may go or when. This turned out to be a disaster for US crypto exchange Poloniex when an obscure token that it offered peer-to-peer margin trading on suffered a flash crash.

On May 26, the price of CLAMdropped so violently that margin borrowers blew their margins multiple times over. The loss was huge: 1,800 BTC, valued at around $14 million.

Now Poloniex has to figure out how to extract the losses from the borrowers. For now, lenders will have to suck up the loss. On 14:00 UTC on June 6 — a full 10 days after the incident — Poloniex applied a 16.202% haircut to the principal of all active BTC loans. Even lenders not active at the time of the crash were affected.

David, it's straight out of the Bitfinex 2016 playbook. Haircut on unrelated lenders some time after the actual losses were incurred.

— (((Frances Coppola))) (@Frances_Coppola) June 7, 2019

Prior to announcing the haircut, Poloniex suspended trading for several hours on Wednesday as part of a “planned” maintenance. It wasn’t until trading resumed that margin lenders realized a portion of their BTC was missing.

In a Medium post, Poloniex revealed that a large part of the loans were collateralized in CLAM — so both the borrowers’ positions and their collateral lost most of their value. In other words, the funds simply evaporated, and there was nothing to repay loans with.

The exchange says it has frozen all defaulted borrowers’ accounts until they repay their loans, as spelled out in the the company’s terms of service.

“As we recover funds, we will return them to affected lenders. We’re also exploring other ways to help defray margin lender losses,” Poloniex wrote.

Naturally, the margin lenders, which only account for 0.4% of Polo’s user base, are completely pissed off. Why did Polo not have better risk management in place? Why did it not have an insurance fund set up to absorb the loss? And why did Polo allow margin trades — and collateral loans — on an extremely illiquid coin in the first place?

What is margin trading?

Margin trading is risky business, even more so when you are trading crypto assets, due to their high volatility. When you trade on margin, you put down a collateral and borrow against that, doubling, tripling, quadrupling — or whatever — your trade.

Trading on margin magnifies your profits, but also your losses. If the trade goes in your favor, you can repay the loan and tuck in a nice profit. But if the price of the asset slips enough so it looks like your trade won’t pay off, the exchange can call in your margin, and you lose all of the collateral you put down for the loan.

Bitcoin derivatives exchange BitMEX loans you the funds for margin trades. Poloniex does something different. It uses peer-to-peer margin trades, where a common pool of lenders puts up BTC, CLAM, and other coins. They get paid in interest. According to Poloniex’s website (archive), only customers who are outside of the US are allowed to loan their funds on the exchange.

As a lender, you set your own daily interest rate, and Poloniex takes a fee of 15% from the interest earned. Margin traders consume lending offers starting with the lowest rate. If your rates are too high, your funds sit in the pool, and you don’t earn any interest.

CLAM, the casino coin

If you were paying close attention a year ago, you may have heard John Oliver mention CLAM on “Last Week Tonight,” along with Titcoin, Jesuscoin, Trumpcoin and a bunch of other coins with hilarious names.

CLAM stands for “Caritas Libertas Aequitas Monetas,” which roughly translates to freedom, fairness, equality coins — whatever that means. The coin launched in May 2014, as a fork ofBlackcoin (BLK), which launched in February 2014 as a fork of Peercoin, an early proof-of-stake coin.

On May 12, 2014, CLAM was sent to all active users of bitcoin, litecoin and dogecoin —three popular coins at the time. Every unique wallet address pulled from those blockchains that had a balance above zero got about 4.6 CLAM. The total amount of CLAM distributed to those addresses was 14,897,662.

CLAM was mainly intended for use on Just-Dice, a gambling site created by a Canadian known only as “dooglus.” Originally Just-Dice relied on bitcoin. But due tonew bitcoin regulation in Canada, dooglus decided to switch to CLAM in late 2014.

The circulating supply of CLAM is only 3,624,208. Nearly all of that—99.81%—is traded on Poloniex. At one point, CLAM was listed on Bittrex and Cryptopia, but Bittrex delisted the coin in October 2018 and Cryptopia went belly up in May 2019.

According to CoinMarketCap, CLAM has a daily trading volume of less than $100,000, meaning the coin barely has a pulse. Three months ago, two traders complained on Reddit of long delays withdrawing CLAM as they waited for the lifeless network to pick up their transactions.

“I withdrew CLAM 11 days ago. Poloniex Support said ‘as soon as a miner picks up the transaction’ How f@%#$%g long is that?,” wrote Reddit user interop5. (Technically, CLAM is a proof of stake coin, so it relies on stakers, not miners.)

CLAM’s lack of liquidity makes it extremely easy to manipulate. All you need is one person to put up a large sell order to crash the price. Poloniex has yet to release details on what happened, but we can guess it was something along those lines.

How to Clams Trade 1) accumulate cheap clams in account A 2) move some to account B and long your clams w/ your clams 3) dump your account A spot clams on your account B margin clam buy orders 4) rugpull 5) make 500-1k btc in account A while burning 50-200 btc in account B

As a result of the flash crash debacle, Poloniex has removed CLAM from margin trading, along with three other coins: bitshares (BTS), factom (FCT), and maidsafecoin (MAID). The exchange outright admits these coins lacked sufficient liquidity:

“In order for margin liquidations to process in an orderly manner, the market must have sufficient liquidity, and these tokens currently lack that liquidity. We will continue to monitor them and may reinstate margin trading for them in the future”

This is not the first time Poloniex removed CLAM as a margin market and collateral coin. It was removedin early November 2017 due to low liquidity, after an earlier flash crash, despite CLAM’s liquidity never recovering, at some point, Poloniex decided to add CLAM back as a margin market and collateral coin—though I’m not sure exactly when.

And then, of course, the exact same thing happened. In February 2019, the price of CLAM started to climb rapidly on Poloniex. In a matter of six weeks, it went from around $1.50 to a high of nearly $20 on May 26. At that point, the bottom fell out with CLAM losing three-quarters of its value in the blink of an eye. It sunk down to around $5.

According to Andrew Hires, a neurobiology professor at the University of Southern California, who has been watching the exchange, Poloniex had been struggling with its CLAM wallet for months. He tweeted:

“All deposits had to be manually credited via ticket. This screwed up the sell-side liquidity. Huge bids (>500BTC), presumably margin longs, crept up over months, pushing $ price up 17x. Just after it hit $20, everything imploded.”

Spreading the loss

Socializing losses is unique to crypto exchanges. Like Poloniex, OKEx alsosocializes extreme margin losses, but literally requires customers to pass a test on their terms of service before they can trade futures, so they are absolutely clear on how it works.

According to crypto lawyer David Silver, socializing losses could open Poloniex to a lawsuit. Another lawyer, Stephen Palley, disagrees. Palley told The Block, he doesn’t think Poloniex breached its terms of service.

On the other hand, Emilien Dutang, who was pinged by the haircut and says he offered margin lending on the exchange after the flash crash, is threatening legal action.

I was NOT lending on the 26 may, I started lending on the 27th.

THERE IS ABSOLUTLY NO JUSTIFICATION FOR YOU TO TAKE MY BITCOINS TODAY.

Do not try to hide your fuck up behind the fact that it impacted "only" 0.4% of your users

None of this bodes well for Poloniex. Circleacquiredthe exchange in early 2018 with the intention of cleaning it up and dealing with a humongous backlog ofsupport tickets. But at this level, Poloniex appears only slightly more competent than QuadrigaCX.

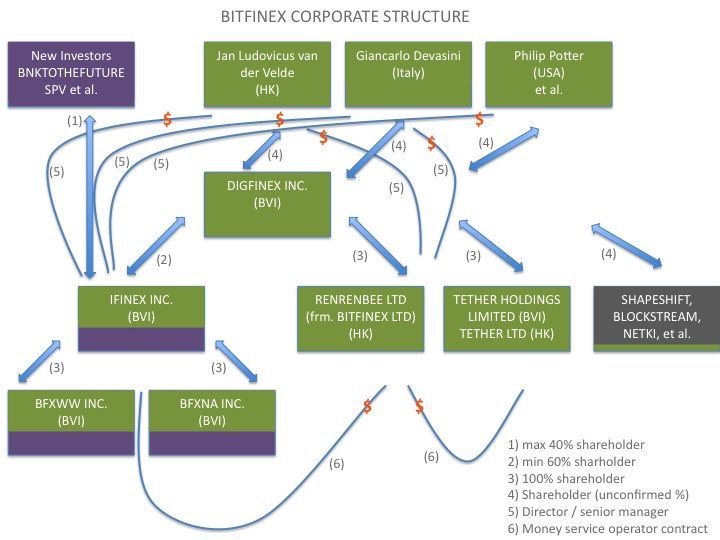

Bitfinex was not happy with the New York Attorney General’s April 24 ex parte court order, which demanded that the crypto exchange stop dipping into Tether’s cash reserves and hand over documents that were requested in November 2018. It struck back with a strongly worded motion to vacate, or overturn the order.

On May 3, the Office of the Attorney General (OAG) submitted an opposition to that motion. The agency argues that Bitfinex violated the Martin Act, New York’s anti-fraud law, widely considered the most severe blue sky law in the country.

Legally, Tether and Bitfinex are separate entities, but they are managed by the same individuals. To note, the OAG’s order does not prohibit Bitfinex from operating. Nor does it prohibit Tether from issuing or redeeming tethers (USDT) for U.S. dollars.

The order simply prohibits Bitfinex from helping itself to anymore of Tether’s funds. This, of course, poses a problem for Bitfinex, because it desperately needs cash to stay afloat. (It’s latest effort to fill the gap is a token sale, but that is another matter.)

There are currently 2.8 billion USDT in circulation, and each of them is supposed to be backed 1:1 with the dollar, but as of now, they are only 74% backed.

The alleged fraud

The OAG began investigating Bitfinex late last year. If there is any question as to how Bitfinex allegedly committed fraud and misled its customers, the OAG spells that out clearly in its memorandum. I’m paraphrasing some this.

Bitfinex failed to disclose to its clients that it had lost $851 million of “wrongfully commingled” client and corporate funds to Crypto Capital, an overseas entity, which it used as an intermediary to wire US dollars to traders on its platform.

Bitfinex knew in mid-to-late 2018 that Crypto Capital’s inability—or unwillingness—to return the funds meant it would have problems filling out client requests to withdraw cash off the exchange. Nevertheless, it told the public that rumors of insolvency were a “targeted campaign based on nothing but fiction.”

In November 2018, Bitfinex tried to cover up the loss by moving (at least) $625 million from Tether’s legitimate bank account into Bitfinex’s account. In return, Bitfinex “credited” $625 million to Tether’s accounts with Crypto Capital. OAG says the credit was “illusory,” because the money at Crypto Capital was lost or inaccessible.

(In its motion to vacate, the OAG notes that Bitfinex contradicted itself by saying the “credit” Bitfinex gave to Tether was $675 million—a $50 million discrepancy.)

Bitfinex later shifted to a new strategy. It engaged in “an undisclosed and conflicted transaction” to let Bitfinex dip even further into Tether’s reserves. The exchange took out a $900 million loan from Tether, secured by shares of iFinex—the parent company of both Tether and Bitfinex. OAG says there is little reason to believe the iFinex shares have any real value, especially in the event iFinex itself defaults.

In March 2019, $900 million represented almost half Tether’s available reserves at the time, but Bitfinex and Tether did not disclose this to its customers. In fact, up until February 2019, Tether telling its customers that USDT was fully backed. Bitfinex told the OAG that it has already dissipated $750 million of Tether’s funds.

Bitfinex demonstrates “a pattern of undisclosed, conflicted, and deceptive conduct” that its customers would “find material, and indeed, essential to buying tethers and trading assets, like bitcoin, on the Bitfinex platform,” the OAG said.

In its motion to vacate, Bitfinex argues that the Martin Act stands or falls on whether tethers are securities or commodities. It does not, the OAG says. In fact:

“The Bitfinex trading platform transacts in both securities and commodities (like bitcoin) and is of course at the core of the fraudulent conduct set forth in the OAG’s application.”

Related events

The OAG points to other events that underscore the need to maintain the status quo.

Since the original order, two individuals, Reginald Fowler and Ravid Yosef, were charged with bank fraud in connection with their operation of a “shadow bank.” Fowler was arrested on April 30, while Yosef is still at large.

The operation processed hundreds of millions of dollars of unregulated transactions on behalf of numerous cryptocurrency exchanges and associated entities—“several of which,” the OAG says, are at the center of its own investigation.

This appears to indicate the OAG’s is looking into other exchanges, which makes sense, given it sent out a questionnaire to more than a dozen cryptocurrency exchanges in April 2018, requesting they disclose key information about their operations.

While the OAG does not specifically state that the “shadow bank” is Crypto Capital, it points to the Memorandum in Support of Detention of Fowler, which said that companies associated with Fowler “failed to return $851 million to a client of the Defendant’s shadow bank.”

There is so much going on now with Bitfinex. My eyes are burning and my head hurts from reading piles of court docs. Here is a rundown of all the latest—and then some.

The New York Attorney General (NYAG) is suing Bitfinex and Tether, saying tethers (USDT) are not fully backed—after $850 million funneled through third-party payment processor Crypto Capital has gone missing.

It’s still not clear where all that money went. Bitfinex says the funds were “seized and safeguarded” by government authorities in Portugal, Poland and the U.S. The NYAG says the money was lost. It wants Bitfinex to stop dipping into Tether’s reserves and to handover a mountain of documents.

In response to the NYAG’s ex parte order, Tether general counsel Stuart Hoegner filed an affidavitaccompanied by a motion to vacate from outside counsel Zoe Phillips of Morgan Lewis. Hoegner admits $2.8 billion worth of tethers are only 74% backed, but claims “Tether is not at risk.” Morgan says New York has no jurisdiction over Tether or Bitfinex. Meanwhile, the NYAG has filed an opposition. It wants Bitfinex to stop messing around.

Bitfinex: No one is willing to audit us because they don't want to damage their reputation by auditing us! Asymmetric risk!

New York Attorney General: We'll audit you! For free! Bitfinex: NOT LIKE THIS! New York Attorney General: Send documents. Bitfinex: NO GOD PLEASE NO!

Football businessman Reggie Fowler and “co-conspirator” Ravid Yosef were charged with running a “shadow banking” service for crypto exchanges. This all loops back to Crypto Capital, which Bitfinex and Tether were using to solve their banking woes.

In an odd twist, the cryptocurrency saga is crossing over into the sports world. Fowler was the original main investor in the Alliance of American Football (AAF), an attempt to create a new football league. The league filed for bankruptcy last month—after Fowler was unable to deliver, because the DoJ had frozen his bank accounts last fall.

The US government thinks Fowler is a flight risk and wants him held without bail. The FBI has also found a “Master US Workbook,” detailing the operations of a massive “cryptocurrency scheme.” They found it with email subpoenas, which sounds like it was being kept on a Google Drive?

Yosef is still at large. She appears to have split her time between Tel Aviv and Los Angeles. This is her LinkedIn profile. She works as a relationship coach and looks to be the sister of Crypto Capital’s Oz Yosef (aka “Ozzie Joseph”), who was likely the “Oz” chatting with “Merlin” documented in NYAG’s suit against Bitfinex.

All eyes are on Tether right now. Bloomberg reveals the Commodity and Futures Trading Commission (CFTC) has been investigating whether Tether actually had a stockpile of cash to support the currency. The DoJ is also looking into issues raised by the NYAG.

Meanwhile, bitcoin is selling for a $300 to $400 premium on Bitfinex — a sign that traders are willing to pay more for bitcoin, so they can dump their tethers and get their funds off the exchange. This isn’t the first time we’ve seen this sort of thing. Bitcoin sold at a premium on Mt. Gox and QuadrigaCX before those exchanges collapsed.

Bitfinex is still in the ring, but it needs cash. The exchange is now trying to cover its Tether shortfalls by raising money via—of all things—a token sale. It plans to raise $1 billion in an initial exchange offering (IEO) by selling its LEO token. CoinDesk wrote a story on it, and even linked to my Tether timeline.

It's funny because LEO also means law enforcement organization

Tether wants to move tethers from Omni to the Tron blockchain. Tron planned to offer a 20% incentive to Omni USDT holders to convert to Tron USDT on Huobi and OkEx exchanges. But given the “recent news” about Bitfinex and Tether, it is delaying the rewards program.

Coinbase is bidding adieu to yet another executive. Earn.com founder Balaji Srinivasan, who served as the exchange’s CTO for a year, is leaving. It looks like his departure comes after he served the minimum agreed period with Coinbase.

Elsewhere, BreakerMag is shutting down. The crypto publication had a lot of good stories in its short life, including this unforgettable one by Laurie Penny, who survived a bitcoin cruise to tell about it. David Gerard wrote an obituary for the magazine.

The Los Angeles Ballet is suing MovieCoin, accusing the film finance startup of trying to pay a $200,000 pledge in worthless tokens—you can’t run a ballet on shit coins.

Police in Germany and Finland have shut down two dark markets, Wall Street Market and Valhalla. And a mystery Git ransomware is wiping Git repository commits and replacing them with a ransom note demanding Bitcoin, as this Redditor details.

The U.S. government wants a football businessman linked to an investigation into $850 million of missing Tether and Bitfinex funds to be held without bail.

According to a memorandum in support of detention filed with the District Court of Arizona on May 1, Reginald Fowler poses a serious flight risk due to his overseas connections and access to hundreds of millions of dollars.

The court doc also presents startling new twists in an already tangled plot—a “Master US Workbook,” which details the financial operations of the “cryptocurrency scheme,” fake bond certificates worth billions of dollars, and a counterfeit money operation.

Reggie Fowler

Fowler, 60, is a former minority owner of the Minnesota Vikings and the original main investor in the Alliance of American Football —an attempt to form a new football league. The AAF collapsed when Fowler withdrew funding—after the Department of Justice froze his bank accounts in late 2018.

I did a search on Pacer and got a number of hits showing Fowler has been in and out of courts for years. In fact, in 2005, ESPN reported that he had been sued 36 times.

Most recently, Fowler was charged with bank fraud and operating an unlicensed money services business. These crimes relate to his alleged involvement in a “shadow bank” on behalf of cryptocurrency exchanges, in which hundreds of millions of dollars passed through accounts that he controlled in jurisdictions around the world.

Fowler operated Global Trading Solutions LLC in the US, which provided services for Global Trade Solutions AG, the Zug, Switzerland-based parent company of Crypto Capital Corp, a third-party payment processor. At one time or another, Crypto Capital serviced QuadrigaCX, Bitfinex, Kraken, Binance, and BitMEX—some of the top crypto exchanges.

In October and November 2018, five U.S. bank accounts were frozen—three of them were Fowler’s personal accounts and two were held under Global Trading Solutions. On April 11, Fowler was indicted in the Southern District of New York. And on April 30, he was arrested in Chandler, Arizona, where he lives.

Fowler is looking at spending the rest of his life in prison—the bank fraud counts alone carry a maximum sentence of 30 years.

The cryptocurrency scheme was not limited to the U.S. Fowler set up bank accounts around the world and coordinated the scheme with co-conspirators in Israel, Switzerland, and Canada, according to court documents. The scheme involves a “staggering amount of money,” and the government believes that Fowler still has access to overseas bank accounts.

Master US Workbook

Even more revealing, via email search warrants, federal prosecutors have obtained a document entitled “Master US Workbook,” which details the operations of the scheme. The workbook lists 60 bank accounts. It shows the scheme received over $740 million in 2018 alone. As of January 2019, the combined bank balance was $345 million. Approximately $50 million is held in U.S. accounts. The rest is located overseas.

Apparently, Fowler had “shown a willingness to help himself to these funds in the past.” In mid-2018, he sent $60 million from scheme accounts to his personal bank accounts, feds said. Scheme members set up a “10% fund” from client deposits, available for his personal use. The government does not know the location of those accounts.

After Fowler’s bank accounts were seized in October 2018, he agreed to cooperate with FBI agents and keep the investigation confidential, which he did not do. When agents sent him emails, he would share those with other scheme members.

Other illegal activity

Fowler appears to have been involved with other illegal activities, such as wire fraud related to the 10% fund. He also tried to take out loans by presenting banks with fraudulent bond certificates worth billions of dollars.

FBI agents also found evidence that Fowler was involved in a counterfeit money operation. They found $14,000 in fake bills consisting of sheets of $100 bills in a filing cabinet in his Chandler, Arizona office.

After examining the sheets, a special agent for the U.S. Secret Service “determined that they were undergoing a process common in counterfeiting schemes to turn paper bills into passable currency. In fact, the FBI also recovered black carbon paper from the office, which is often used as part of this process for making believable counterfeit bills.”

According to an April 24 court filing, New York State Attorney General Letitia James has alleged that crypto exchange Bitfinex lost $850 million and then tried to pull the wool over people’s eyes by dipping into Tether’s reserves.

Tether issues a dollar-pegged stable coin of the same name. According to the Office of the Attorney General (OAG), Bitfinex has so far siphoned $700 million from Tether funds, meaning that tethers are not fully backed. Given that tether is an essential source of liquidity in the crypto markets—currently, there are 2.8 billion tethers in circulation—this is not good news for bitcoin.

I’ve updated my Bitfinex/Tether timeline to bring you up to speed on the full history of these companies’ past shenanigans. Bitfinex and Tether are operated by the same individuals, and their parent company is Hong Kong-based iFinex. I recommend reading the entire 23-page courtdocument. It reveals a lot about what has been going on under the covers at Tether/Bitfinex. I’ll try and summarize.

What happened

Bitfinex was allowing residents of New York to trade on its platform. This is not supposed to happen. Effective August 8, 2015, any virtual currency company that wants to do business in New York State needs to have a BitLicense. This led the OAG to launch an investigation into Bitfinex and Tether in 2018.

Banking has been an ongoing struggle for Bitfinex since April 2017, when it was cut off by correspondent bank Wells Fargo and its main banks in Taiwan. At different periods, Bitfinex has turned to Puerto Rico’s Noble Bank, Bahamas’ Deltec Bank, and more recently, HSBC via a private account with Global Trading Solutions LLC.

Meanwhile, Bitfinex has had to rely on third-party payment processors to handle customer fiat deposits and withdrawals—a fact that it has never been completely up front about. (In fact, the HSBC account turns out to be part of the shadow banking network set up by its payment processor.)

Since 2014, Bitfinex has sent $1 billion through Panama-based Crypto Capital Corp. Bitfinex also told the OAG that it had used a number of other third-party payment processors, including “various companies owned by Bitfinex/Tether executives,” as well as other “friends of Bitfinex” — meaning human-being friends of Bitfinex employees willing to use their bank accounts to transfer money to Bitfinex clients.

This is basically Bitfinex setting up shell companies and playing cat and mouse with the banks—and it sounds a lot like what Canadian crypto exchange QuadrigaCX was doing before it went belly up in January. (Quadriga also used Crypto Capital, but the payment processor is not holding any Quadriga funds.)

By mid-2018 Bitfinex customers were complaining they were unable to withdraw fiat from the exchange. This is apparently because Crypto Capital, which held “all or almost all” of Bitfinex funds, failed to process customer withdrawal requests. Crypto Capital told Bitfinex that the reason the $850 million could not be returned was because the funds were seized by government authorities in Portugal, Poland and the U.S.

Bitfinex did not believe this explanation. “Based on statements made by counsel for Respondents to AG attorneys… Respondents do not believe Crypto Capital’s representations that the funds have been seized,” the court document states.

(This is not in the court filings but Crypto Capital shared this letter with its customers in December 2018. The letter is from Global Trade Solutions AG, the parent company of Crypto Capital Corp——not to be confused with Global Trading Solutions LLC. The letter states that GTS AG is being denied banking services in the U.S., Europe, and elsewhere “as a result of certain AML and financial crimes investigations” by the FBI and cooperative international law enforcements and/or regulatory agencies.”)

In communication logs from April 2018 to early 2019 shared with the OAG, a senior Bitfinex executive “Merlin” repeatedly beseeched an individual at Crypto Capital, “Oz,” to return funds. Merlin writes: “Please understand, all this could be extremely dangerous for everybody, the entire crypto community. BTC could tank to below $1K if we don’t act quickly.” A Crypto Capital customer, who asked not to be named, told me that Merlin is Bitfinex CFO Giancarlo Devasini.

Borrowing money from Tether

Rather than admit it was insolvent, Bitfinex/Tether tried to cover up the problem. According to the court docs, in November 2018, Tether transferred $625 million in an account at Deltec in the Bahamas to Bitfinex. In return, Bitfinex caused $625 million to be transferred from an account at Crypto Capital to Tether’s Crypto Capital account.

Absolute legendary move here, Bitfinex took $625 million in real money at a real bank from Tether, and in exchange gave Tether back $625 million in fake money at a fake bank. https://t.co/llyRhT4Op2pic.twitter.com/wFPmmOnGVI

Essentially, Bitfinex tries to create the money by doing a one-for-one transfer of real money at Deltec for funds that don’t actually exist at Crypto Capital. Once they realized that this was probably a terrible idea, they re-papered the transfer as a loan.

Bitfinex then borrowed $900 million from its Tether bank accounts. The loan is secured with shares in iFinex stock. In case you didn’t quite follow that, Bitfinex and Tether are basically the same company, so you can think of this as Bitfinex borrowing money from itself—and then backing the loan with shares of itself.

According to the OAG, “The transaction documents were signed on behalf of Bitfinex and Tether by the same two individuals.”

OAG is fed up with the nonsense. It has obtained a court order against iFinex. Under the court order, Bitfinex and Tether are to cease making any claim to the dollar reserves held by Tether. iFinex is also required to turn over documents and information as the OAG continues its probe.

The court has also ordered that iFinex identify all New York and U.S. customers of Bitfinex whose funds were provided to Crypto Capital and the amount of any outstanding funds—and provide a weekly report evidencing any issuance or redemption of tethers.

Bitfinex responds

Bitfinex has issued a response (archive), stating that the OAG court filings “were written in bad faith and are riddled with false assertions.” It claims the $850 million are not lost but have been “seized and safeguarded.”

The exchange continues to deny any problem. It writes:

“Both Bitfinex and Tether are financially strong—full stop. And both Bitfinex and Tether are committed to fighting this gross overreach by the New York Attorney General’s office against companies that are good corporate citizens and strong supporters of law enforcement.”

What does this mean?

It means Bitfinex is in real trouble. The New York’s Attorney General is one of the most powerful in the nation. That should worry Bitfinex.

New York law allows the AG to seek restitution and damages. On top of that, there is also the Martin Act, a 1921 statute designed to protect investors. The Act vests the attorney general with wide-ranging enforcement powers. Under the Act, the attorney general can issue subpoenas to compel attendance of witnesses and production of documents. Those called in for questioning do not have a right to counsel.

The attorney general‘s decision to conduct an investigation is not reviewable by courts. As Stephen Palley, partner at Anderson Kill, points out, the iFinex action arises out of a Martin Act investigation and “Violations of the Martin Act can be civil and criminal.”

The Martin Act is a New York law that gives the N.Y. Attorney General very broad power to investigate securities fraud.

Violations of the Martin Act can be civil and criminal.

The New York A.G.' Tether/Bitfinex action arises out of a Martin Act investigation. pic.twitter.com/VsDgDcEjw8

Finally, if $850 million is really missing, not just stuck somewhere, Bitcoin is in real trouble, too. Tether could lose its peg and drop substantially below $1. Remarkably, tether’s peg seems to be holding steady now.

Since the news broke, the price of bitcoin has dropped several hundred dollars. A valiant effort is being made to pump the price back up, and it’s working, sort of—for now.

Previously, I wrote that QuadrigaCX cofounders Michael Patryn and the now-deceased Gerald Cotten worked together for a period at Midas Gold, a Liberty Reserve exchanger that ran from 2008 until May 2013, when it was pulled offline. Now it appears that their connections stretch back even further.

According to data gathered by Reddit user QCXINT, the two business partners were active on TalkGold, a popular forum for pushing high-yield investment programs, aka Ponzi schemes, as early as 2003. Likely, that is where they first met. Evidence also suggests the two were active on BlackHatWorld, a site for discussing dubious marketing strategies for websites. Cotten also appears to have been a Ponzi operator himself.

This is a long post, so here is a quick summary of what’s ahead:

Cotten began promoting Ponzi schemes in his teens.

He was posting on TalkGold under the username “Sceptre.”

Michael Patryn, aka Omar Dhanani, posted on TalkGold as “Patryn.”

“Patryn” and “Sceptre” joined TalkGold in 2003, within months of each other.

Michael Patryn also posted as “Patryn” on MoneyMakerGroup and BlackHatWorld.

“Sceptre” first appeared on BlackHatWorld in 2012, but changed his profile name to “Murdoch1337.”

“Sceptre” posted as “Lucky-Invest” on TalkGold to promote a Ponzi.

What is a high-yield investment program?

HYIP schemes typically promise ridiculously high rates of returns, but behind the scenes, no real investment is taking place. The operator simply uses money from new investors to pay off earlier ones, all the while skimming funds off the top for himself. When the supply of new investors runs dry, the scheme collapses. All Ponzi schemes collapse at some point.

Flimflam man Charles Ponzi, 1920.

Ponzi schemes are nothing new. The name stems from Charles Ponzi, an Italian immigrant who defrauded tens of thousands of Bostonians out of $18 million in 1920. Ponzi went to jail, and when he got out, the U.S. promptly deported him to Italy. New York financier Bernie Madoff ran a $65 billion Ponzi, the largest in history. His Ponzi fell apart during the financial crisis when too many customers started trying to pull their money out. Madoff was convicted in 2008.

In the early 2000s, the internet and the advent of early centralized digital currencies, like E-gold and Liberty Reserve, saw a new wave of Ponzi schemes. Operators anonymously set up their storefronts online and used e-currencies to obscure the source and flow of funds.

HYIP operators typically rely on social media and referrals to create hype and make their offerings appear legitimate. Despite the red flags, many people invest in HYIPs, thinking that if they get in early enough, they can make a buck.

An entire subculture has proliferated around HYIPs. There are sites that track and monitor HYIPs, and forums where people go to promote and learn more about HYIPs. There’s even an HYIP subreddit.

When an HYIP scheme collapses, the collapse is generally blamed on a hack, a theft, or a bad investment—some type of external event that is plausibly at arm’s length from the operator. When that happens, the HYIP operator begins issuing “refunds”—in good faith, of course.

Some HYIP operators even go to the effort of setting up long-winded spreadsheets and paying back dribs and drabs over months. Naturally, the first people to get paid back are generally insiders or the operators themselves—under different names—who then proclaim what a great guy the operator is, and how decent it is of him to spend all of his time and effort refunding everyone.

The U.S. Financial Industry Regulatory Authority (FINRA), the regulatory body charged with governing business between brokers, dealers and the investing public, writes that “virtually every HYIP we have seen bears hallmarks of fraud.”

TalkGold and MoneyMakerGroup

Starting in January 2003, TalkGold and sister site MoneyMakerGroup were two hugely popular internet forums for launching and promoting HYIPs. The sites were pulled offline on August 21, 2017, a day after the Department of Justice filed an asset forfeiture complaint against the Krassenstein brothers, Edward and Brian, who ran the sites. Homeland Security raided the twins’ Florida homes a month later.

“Since at least 2003, Brian and Edward Krassenstein … have owned and operated websites devoted to the promotion of fraudulent HYIPs. In particular, the Krassenstein run sites ‘talkgold.com’ and ‘moneymakergroup.com’ are discussion forums in which HYIP operators advertise and promote their fraud schemes to potential victims.”

Patryn on TalkGold

Michael Patryn, formerly Omar Dhanani, was arrested in October 2004 on charges related to his involvement with Shadowcrew, a cybercrime message board. Operating under the pseudonym “Voleur,” French for thief, he offered Shadowcrew members an e-money laundering service—wire him cash, and he would fund your E-gold account, helping to obscure your financial trail.

After the Shadowcrew bust, TalkGold users began to speculate that “Patryn,” a prolific poster on TalkGold, was in fact, Dhanani—and there is good reason to suspect that he was.

“Patryn” joined TalkGold on April 3, 2003. His profile linked directly to VFS Network, a network for several digital currency exchangers, including three that Patryn himself operated: Midas Gold, HD Money, and Triple Exchange. VFS Network (stands for Voleur Financial Services) was also his business.

“Patryn” also openly admits on TalkGold that he operates Midas Gold. The business registration for Midas Gold also lists “Omar Patryn” (one of Patryn’s known aliases) as its sole director.

Further, Patryn appears to have used the profile name “Patryn” on MoneyMakerGroup, with the same link to VFS Network. He joined MoneyMakerGroup on November 27, 2007, six months after he got out of a U.S. federal prison, where he served 18 months related to his earlier Shadowcrew arrest.

Sceptre on TalkGold

Cotten was likely “Sceptre” on TalkGold. Sceptre joined TalkGold on July 4, 2003, three months after “Patryn” joined. Cotten would have been 15 or 16, at the time.

TalkGold members were able to list “friends” on the site. A May 2013 profile page for Patryn shows that he had six friends—one of whom is Sceptre. Similarly, a May 2013 profile page for Sceptre shows he had one friend—“Patryn.”

The two also interacted. Many of Sceptre’s TalkGold posts appear alongside Patryn’s in the same thread, either promoting or defending VFS Network, Midas Gold, or one of the other exchanges that Patryn operated. (There is also evidence to suggest that Cotten, not Patryn, was the main operator for Midas Gold.)

On December 7, 2009, when a user on TalkGold complains that he is having issues with Midas Gold, Sceptre replies: “I’ve never had any problems with M-Gold. They are usually very efficient.” Patryn follows on the same thread with, “M-Gold does not work during weekends. What is your order reference number? I will have it taken care of ASAP.”

On September 29, 2012, “Patryn” responds to someone complaining about Midas Gold keeping their money. (This was not unusual, by the way. There were many complaints about Midas Gold withholding customer funds. See here, here and here.)

“Patryn” writes:

“To the best of my knowledge, both of us have been responding to your emails. You sent me five emails yesterday demanding that I hurry up and resolve this issue. Your issue will be resolved ASAP. Unfortunately, I cannot force the banks to speed up their investigation process.”

In the same thread, Sceptre replies to “Patryn,” almost mocking the customer.

“lol, I’m surprised you’re willing to help him. You offer your dispute resolution for free, and he thanks you by spamming your inbox and complaining that you don’t reply while you’re sleeping.”

In September 2012, a poster asks, “I am looking for a LR Exchanger into HD-Money.” (Basically, the poster wants to convert one digital currency, Liberty Reserve, into another, HD-Money, without having to go through fiat). Sceptre replies, “For this type of trade I would use ecashworldcard.” Patryn follows by posting a link to his HD-Money site, which lists Ecash World Card as an offering.

Cotten and Patryn on BlackHatWorld

BlackHatWorld is a forum where people go to discuss “black hat” marketing tactics. Paid shilling (paying someone to promote your product on social media), negative SEO attacks (improving your SEO ranking by destroying your competitor’s) and gaming a search engine’s algorithm are all topics of discussion on this forum.

These tactics are generally used by Websites that only plan to stick around long enough to make a quick financial gain, which is exactly what HYIPs aim to do.

Someone going by “Patryn” was also active on BlackHatWorld. This person joined on September 6, 2012, and was last active on September 7, 2017. He only posted nine messages.

Another poster—”Murdoch1337″—in BlackHatWorld, was much more active. He joined on February 12, 2012, and his last activity was January 8, 2017. This person appears to have previously been posting as Sceptre, and we believe this was Cotten.

(QXCINT also tells me that one of Cotten’s email accounts—g@mailhoose.com, which was tied to a number of Cotten’s domain registrations—has or had an active account on BlackHatWorld, but the method he used was too technical for me to confirm independently.)

Murdoch1337 appears as the original poster in a thread titled “Sceptre’s Spectacular Content Services!!! – $1.50 per 100 words” — an indication that Sceptre likely switched his profile name to Murdoch1337 sometime after he started the thread. He responds to other posters in the thread as if he is the one offering the content services. “That’s all the review copies for now,” he writes. “For everyone else, feel free to place your orders using the order info in my original post.”

On September 10, 2013, Murdoch1337 posts an ad for a developer to help him with an upcoming cryptocurrency exchange. In the ad, he writes:

“I am looking for a programmer who is familiar with Bitcoin to develop a website that is very similar to Bitstamp…Also, I’m looking to get this project built and online quickly, so if you are able to do it quickly, that is a bonus.”

This ad was posted three months before Quadriga launched in beta. The timing makes sense given that Quadriga was based on WLOX, an open-source exchange solution available on Github, which would have dramatically reduced the time it took to create a functioning crypto exchange. Alex Hanin built the Quadriga platform, though it is not clear if Cotten actually recruited Hanin via this ad on BlackHatWorld.

An almost identical ad with the title “Bitstamp clone – Bitcoin trading project” was posted on Freelancer.com.The job poster, who was anonymous, had 38 projects on the site. He left a few telling details behind on one ofthe projects:

Hi

I’m looking for programmers who are knowledgeable when it comes to Bitcoin and I found you.

I have a number of projects that need work, including a new Bitcoin exchange. Are you able to build sites like this? If so, i’d like to get in touch

Thanks

Gerry

Skype: gerrywc

email: sceptre@countermail.com.

S&S Investments and Lucky Invest

One of Sceptre’s HYIPs was S&S Investments, a website that opened for business on January 1, 2004. (“Copyright @2004 Sceptre” is written at the bottom of the page.) He promotes the scheme as a way to double your money.

“You invest a sum of money into the program and within 48 hours (usually within 18) you will receive a return of anything from 103% to 150%, possibly more.”

He is sure to point out that this is “not what is called a ponzi or pyramid scheme.” It offers returns that are far better!

In case the first offer sounded a little too far fetched, he changes the text later to something only slightly more believable. S&S now becomes a “fixed-term investment,” which pays 115% in a week….”you can invest and walk away in profit after just 7 days!”

Of course, S&S ultimately collapses, and discussion around it gets moved to the “Closed / Scammed Programs” section of TalkGold, where Sceptre continues to string along anxious investors, who continue to hold out hope for a “refund.” He writes:

“Refunds WILL take some time. I cannot guarantee that they will all be made quickly. The refund process is likely to spread over a long period of time, but I am willing to do my best to refund everyone to the best of my ability. Please be patient and you will receive a lovely surprise in your e-gold, a refund from S&S Investments,” Sceptre writes.

One TalkGold user reviewed what he considered to be the 12 biggest HYIP “scams” on TalkGold. This is what he wrote about S&S Investments:

“S&S Investments is an interesting program because it was operated by a ‘well known’ person in the HYIP arena. I use the quote marks, because this person was not well known at all, in fact he was very anonymous. No one knew his name, other than his nickname he used to post with, Sceptre. He used anonymous proxies, he was very well hidden. Yet because he had over 1000 posts on TalkGold, he earned a kind of pseudo-trust that people get from being very visible and always online.

Sceptre started off with a small little program that promised to pay back a large amount after a few days. It soon grew to become very, very popular, and it was not long before he upgraded to a fully automated script.

Sceptre wouldn’t tell people how he made the money, he just said that was his little secret. Virtually everyone invested into S&S Investments based on his post count on TalkGold. “He’s made a lot of posts on TalkGold, therefore he must be honest” seemed to be the general opinion of the investors.

S&S Investments went for sometime before cracks started to appear. First the website went offline, then was back again, but withdrawals weren’t being honoured, then the site went offline again. Finally, Sceptre made an announcement that S&S Investments were closed and refunds were to promised.

For a while, refunds did proceed, but then things started to dry up. Since the summer, no more refunds have been processed.

Hey, just because someone has thousands of posts on a forum, doesn’t mean he’s a trustworthy guy. Use your head, look at what the whole program is offering.”

In May 2004, Sceptre appears to switch to another TalkGold profile, “Lucky-Invest,” to promote a Lucky Invest HYIP.

At one point in a thread, he apparently forgets to log out of Lucky-Invest and continues responding as if he were Sceptre, until another poster calls him out:

“You forgot to sign in as ‘sceptre’. ohhhhhhhhhhhhhh . .. looks like Lucky-Invest changed their message!!! . . . too funny!!! . .. did you get caught Sceptre??? hahaha ;)”

Sceptre/Lucky-Invest replies:

“I’m not trying to hide. Lucky Invest, the Newest Investment/Game. My profits go to help pay refunds. THIS IS A GAME, IT WILL NOT HAVE ANY REFUNDS.”

This is a straight out admission that Lucky Invest was not an actual investment. It was a “game.” In other words, a fraud. Essentially, Sceptre/Lucky-Invest/Gerald Cotten is saying: When you give me your money, it is mine. There are no refunds in this game, just me sharing my profits.

Knowing that Cotten and Patryn did business together on TalkGold does not tell us where the CA$250 million worth of crypto and fiat that went missing on Quadriga went. (Only a fraction of those funds have been recovered so far.) But it does bring up questions. Was Cotten really just a starry-eyed Bitcoin libertarian? Or was he a seasoned con artist who had no qualms about taking other people’s money?

If you like my writing, consider supporting my work by subscribing to my Patreon for $5, $20, or $50 a month. Every little bit helps!

I am trying to make my news posts shorter with an effort to focus mainly on cryptocurrency exchanges, unless something else comes up that is just fun to write about. If you enjoy my stories, tips are always welcome via Patreon.

At a hearing on April 18, Quadriga’s court-appointed monitor continued its battle with the exchange’s third-party payment processors to get them to hand over transaction records and funds. The court also extended Quadriga’s creditor protection until June 28.

The stay (protecting Quadriga) is in place until June 28. The CCCA proceeding will expire at that point. It won’t be a “restructuring” any more. It’ll be a pure bankruptcy.

Dorian Nakamoto, one of those who turned out not to be Craig Wright.

Craig Wright, who claims to be Satoshi, is suing people who are accusing him of not being Satoshi. (Wright has yet to prove he actually is.) As mentioned in my last newsletter, it all started when Wright sued twitter user Hodlonaut. Wright has now followed with libel suits against Bitcoin podcast host Peter McCormack, Ethereum co-founder Vitalik Buterin and crypto blog Chepicap. (CoinGeek, a publication financed by Calvin Ayre, Wright’s billionaire backer, has a full story.)

Craig has started filing lawsuit against those falsely denying he is Satoshi….they can all have a day in court to try to prove their fake case but the judge will rule that Craig invented Bitcoin because he did and he can prove it. https://t.co/d2W44mU9Tl

Naturally, the Bitcoin community is up in arms. In response, Binance—an exchange that has been traditionally unselective in the coins it lists—has delisted BSV (stands for Bitcoin Satoshi’s Vision), the coin that resulted from the bitcoin fork spearheaded by Wright and Ayre. The move was followed by several other exchanges delisting BSV, including Kraken, ShapeShift and Bittylicious. Blockchain.info removed support for BSV from its wallet.

Kraken’s BSV delisting was in response to a poll it put up on Twitter. This quote from Kraken founder Jesse Powell is priceless. He says:

“In this case, it is a unique case for us, we haven’t delisted any other coins because the founders, people who are promoting it turned out to be total assholes.”

Angela Walch, a law professor at St. Mary’s University School of Law, compared the #DelistBSV movement to Visa and PayPal not processing Wikileaks transactions and expressed surprise the crypto world was cheering it.

Thanks for all the comments! Yes, I know that exchanges are centralized and I know what people say about BSV.

From the outside, this looks an awful lot like a Visa/Paypal not processing Wikileaks transactions, so it's fascinating to see the crypto world cheering for it.

Meanwhile Gemini’s Tyler Winklevoss says Gemini never listed BSV in the first place, and Chandler Guo, a Chinese miner who has made a fortune on ICOs and Bitcoin forks, announced that he would do the opposite and list BSV.

Crypto exchanges just aren’t pulling in the gazillions they used to. Binance generated about $78 million in profit last quarter, up 66 percent quarter-over-quarter. But that still falls short of full year 2018, when the exchange made $446 million in profits. Coinbase brought in revenue of $520 million in 2018, down 44 percent year-over-year.

2018 has been an absolutely brutal year for Coinbase. In mid-2018, they had projected $1.3 billion of revenue for 2018, which means they generated 60% less than they originally projected. Yikes. IPO prospects looking really bleak now

Hacks, inside jobs and irreversible goof-ups are pushing some crypto exchanges to the brink. Coinnest, once South Korea’s third-largest exchanges, is closing. Users have until April 30 to get their funds off the exchange. Coinnest lost $5.3 million in a botched airdrop in January, though it blames its closure on low trading volume.

Elsewhere, on April 10, Bittrex’s application for a BitLicense (required to do business in New York State) was rejected—in part, because Bittrex customers were using fake names, like “Give me my money,” “Elvis Presley” and “Donald Duck” to trade.

Bittrex says the NY Department of Financial Services (DFS) “sent four people who didn’t know anything about blockchain.” DFS responded again, saying the exchange “continues to misstate the facts” and “presents a misleading picture about the denial.”

if only they'd sent people who understood so much about Blockchain that they knew that "Donald Duck", "Elvis Presley" and "Give Me My Money" were legitimate customers

Binance is about to begin the process of moving its BNB (currently an ERC20 token) off the Ethereum network and onto Binance Chain, its custom blockchain. Interestingly, The Block’s Larry Cermak notes that Binance has quietly changed its white paper to remove a clause about the exchange using 20 percent of its profits to buy back BNB.

Arwen, a self-custody solution that uses on-blockchain escrows and off-blockchain atomic swaps to allow traders to maintain control of their keys while they trade, launched on Singapore’s KuCoin earlier this week. KuCoin raised $20 million in VC funding last year, and it is the first exchange to partner with Arwen, created by a company of the same name based in Boston.

Finally, Intercontinental Exchange (ICE), the owner of the New York Stock Exchange, is reportedly eyeing a New York license for its crypto exchange Bakkt. The launch date for Bakkt has been delayed for months due to skepticism from the CFTC. The regulator appears most concerned over how tokens will be stored.

POSConnect, a third-party payment processor holding funds on behalf of failed Vancouver-based crypto exchange QuadrigaCX, has come up with more excuses to delay handing over the money.

Today, at a short and mostly procedural hearing held at the Supreme Court of Nova Scotia, the main topics were extending Quadriga’s creditor protection and dealing with lingering issues related to Quadriga’s third-party payment processors, mainly POSConnect.

Justice Michael Wood agreed to extend the stay until June 28, unless Quadriga’s Companies’ Creditors Arrangement Act (CCAA) proceedings are terminated before then. Quadriga officially entered into a bankruptcy earlier this month.

The stay (protecting Quadriga) is in place until June 28. The CCCA proceeding will expire at that point. It won’t be a “restructuring” any more. It’ll be a pure bankruptcy.

The rest of the 30-minute proceeding was mostly taken up by a back-and-forth between POSConnect’s lawyer and Elizabeth Pillon, a lawyer for Ernst & Young, the court-appointed monitor in Quadriga’s CCAA procedures.

At issue, POSConnect is sitting on CA$281,000 of Quadriga funds. EY wants the payment processor to deliver CA$278,000 right away. The plan is to leave CA$3,000 to cover rolling monthly fees associated with keeping the account open.

POSConnect recently granted George Kinsman, EY’s senior vice president, online access to Quadriga’s documents and transaction data on the platform, and EY would rather pay POSConnect CA$500 a month than risk the firm cutting off all online access.

Pillon said more than 500,000 transactions worth CA$400 million in Quadriga funds were funneled through POSConnect—and sorting all that out is going to take time.

Meanwhile, POSConnect is reluctant to hand over any funds at all. The firm argues that it is due CA$22,000 in legal fees—an amount the POSConnect lawyer called “insignificant” compared to the hundreds of thousands of dollars spent so far in efforts to put Quadriga’s financial affairs in order.

EY is running short on patience. “POSConnect has thrown out more hurdles in respect to their obligation to delivers statements and property than any other third-party payment processor,” Pillon told the judge.

As she explained, EY has been reaching out to POSConnect since February 6 to find a means to get information and funds. Yet it wasn’t until late yesterday that POSConnect put forward $22,000 for legal fees and an administrative cost of $350 an hour to provide reporting—without providing any accounting to support those fees.

Justice Wood said he did not have enough information before him to determine what reasonable legal fees would be for POSConnect. POSConnect will be added to an existing order for other third-party processors, which will require another hearing anyway.

Wood expressed regret that he would no longer be overseeing the Quadriga proceedings. He has been promoted to chief justice of the Appeal Court of Nova Scotia.

Thanks to TheWholeTruthXX for sending me an audio of the hearing.

Spring is in the air! What are your summer plans? If you are considering buying a boat—or maybe even an “almost new” 51-foot Jeanneau with “very, very few hours” for half a million USD—now would be the time!

The yacht belonged to Quadriga’s now-deceased CEO Gerald Cotten. Here is a video of him putting Canada’s plastic money into a microwave. Here he is tossing Winnie the Pooh into a bonfire. And this is him playing with Pokémon cards.

The latest on QuadrigaCX

I wrote about how Michael Patryn and Cotten appear to have been working together at Midas Gold, a Liberty Reserve exchanger, prior to founding Quadriga. David Z. Morris at Breakermag covered the topic as well. (He credited me, so I’m real pleased about that.)

At a court hearing on April 8, Quadriga was given the go-ahead to shift into bankruptcy. The move will save costs and give Ernst & Young (EY) more power as a trustee.

“The trustee can also sell QuadrigaCX’s assets and start lawsuits to recover property or damages,” Evan Thomas of Osler, Hoskin & Harcourt told Bitcoin Magazine. “The trustee will collect whatever it can recover for eventual distribution to creditors.”

An “Asset Preservation Order” for Jennifer Robertson, Cotten’s widow, was filed on April 11. Law firm Stewart McKelvey is setting up three separate trusts to “collect and preserve” any surplus funds from estate assets, personal assets and corporate assets. Depreciable assets, such as Cotten’s yacht, will be sold.

Per the order, Robertson will continue to receive her drawings from her business Robertson Nova Property Management “in accordance with current levels, for the purposes of satisfying ordinary living expenses.” She will also have access to cash from the “personal assets” account to maintain her properties and to cover legal expenses.

Robertson has 10 days from the court order to provide EY with a list of all her assets—including cash on hand.

A cap on pay for Miller Thomson LLP and Cox & Palmer has been raised from CA$250,000 to CA$400,000. The team will continue to represent Quadriga’s creditors in the bankruptcy.

Quadriga’s third-party payment processors now have 10 business days (as opposed to five previously) from when they receive this court order to deliver the following to EY:

VoPay—CA$116,262.17.

Alto Bureau de Change—assets and property.

1009926 BC—all records and transaction-related information.

POSConnect—access to Quadriga’s online account to George Kinsman, who is a partner at EY.

WB21 (now Black Banx)—all records and account statements related to its Quadriga dealings.

The next hearing to discuss issues remaining from the Companies’ Creditor Arrangement Act, including those tied to third-party payments processors, is scheduled for April 18.

Other crypto exchanges

Popular US-based crypto exchange Coinbase suspended trading of BTC-USD pairs for two hours on April 11 due to a “technical issue” with its order book. BTC-USD is a critical trading pair due to its volume and its impact on bitcoin price measures.

It appears that somebody dumped a load of BTC into the exchange’s buy orders causing liquidity to dry up. Coinbase doesn’t want that to happen, so likely that is why it wiped the books, cancelling any outstanding buy or sell orders.

The books are wiped. You can also pump up the price by $900 with just… 70 Bitcoins.

The entire liquidity of Coinbase basically completely vanished. That's why they froze trading. Incredible. pic.twitter.com/AxsrhxhtzB

— Bitfinex'ed 🔥🐧 Κασσάνδρα 🏺 (@Bitfinexed) April 11, 2019

Coinbase Pro, Coinbase’s professional exchange, is continuing to expand its altcoin reach. The exchange is listing three more altcoins: EOS (EOS), Augur (REP), and Maker (MKR). Coinbase first committed to listing MKR in December, but according to The Block’s Larry Cermak, due to low volume, Coinbase decided to hold off listingMKR.

Crypto credit cards are back in vogue. Coinbase has launched a Visa debit card. The “Coinbase Card” will allow customers in the U.K. and EU to spend their crypto “as effortlessly as the money in their bank.” The exchange says it will “instantly” convert crypto to fiat when customers complete a transaction using the debit card. PaySafe, a U.K. payment processor, is the issuer of the card. In the past, these crypto Visa cards have been known to suddenly lose access to the Visa network, so fingers crossed.

Another executive is leaving Coinbase. The firm’s institutional head Dan Romero has announced he is leaving after five years. This is the third executive to depart Coinbase in six months. Director of institutional sales Christine Sandler left last month, and ex-vice president and general manager Adam White quit in October.

Switzerland-based crypto exchange Bitfinex has lifted its $10,000 minimum equity requirement to start trading. This will undoubtedly bring more cash into the exchange. “We simply could not ignore the increasing level of requests for access to trade on Bitfinex from a wider cohort than our traditional customer base,” CEO Jean-Louis van der Velde said in a blog post (archive).

Meanwhile, Bitfinex customers are complaining (here and here) that they are unable to get cash out of the exchange. Nowsome are saying they are having trouble getting their crypto out of Bitfinex as well.

Reddit user “dovawiin” says, “Ive been trying repeated attempts for 2 weeks to withdraw funs and it always says processing. Ive submitted multiple tickets with delayed answers. Ive cancelled and attempted again a few time after waiting 48Hours with no results. Im currently trying again and nothing for over 24 hrs. This is ridiculous.”

Bitfinex also enabled margin trading on Tether. Margin pairs include BTC/USDT and ETH/USDT. Tether has already admitted to operating a fractional reserve, so this is basically adding more leverage to what’s already been leveraged. I’m sure it’s fine though—nothing to worry about here.

Johnathan Silverman, a former employee of Kraken, is suing the crypto platform for allegedly failing to pay him for work he did. Kraken says it got out of New York in 2015. Silverman says the exchange still maintained an over-the-counter trading desk in the state, which requires licensing for crypto businesses. Kraken told Bloomberg, Silverman “is both lying and in breach of his confidentiality agreement.”

Finally, Malta-based Binance, one of the largest crypto exchanges by volume, is partnering with blockchain analytics firm CipherTrace to boost its AML procedures.

That's why Binance flees from every single jurisdiction, because they want to comply.

— Bitfinex'ed 🔥🐧 Κασσάνδρα 🏺 (@Bitfinexed) April 11, 2019

Other interesting stuff

All hell broke lose on Twitter Friday when news got out that Craig Wright is making legal threats against Twitter user “Hodlonaut,” who has been publicly calling Wright a “fraudster” and a “fake Satoshi.” Wright has never been able to prove that he is Satoshi.

In a letter shared with Bitcoin Magazine, SCA ONTIER LLP, writing on behalf of Wright, demands that Hodlonaut retract his statements and apologize, or else Wright will sue him for libel. The letter even includes this bizarre prescribed apology:

“I was wrong to allege Craig Wright fraudulently claimed to be Satoshi. I accept he is Satoshi. I am sorry Dr. Wright. I will not repeat this libel.”

Hodlonaut deleted his Twitter account upon receiving the news. And the crypto community formed a giant backlash against Wright. Preston Byrne is assisting Hodlonaut pro-bono, Peter McCormack is selling T-shirts that say, “Craig Wright is a Fraud,” and Changpeng Zhao, the CEO of crypto exchange Binance threatened to delist Bitcoin SV—the token spearheaded by Wright and billionaire backer Calvin Ayre.

Ayre is also demanding apologies related to some photos of him circulating on Twitter with extremely young-looking women. Coin Rivet writes, “We have agreed to pay Mr Ayre substantial damages for libel. We have also agreed to join in a statement to the English High Court in settlement of Mr Ayre’s complaint.”

China’s National Development and Reform Commission (NDRC) released guidancethat includes shutting down Bitcoin mining. “The risk to Bitcoin in the longer term is other governments taking their cue from China—and taking proof of work more seriously as a problem that needs to be dealt with,” writes David Gerard.

Another Bitcoin mining company has gone belly up. Bcause llc filed for Chapter 11 in Illinois. (Steven Palley uploaded the docs on Scribd.) The company is based in Chicago, but its mining rigs are in Virginia Beach. In January 2018, Virginia Beach Development Authority gave the firm a $500,000 grant to build the $65 million facility. Bcause promised to create 100 full-time jobs, with average salaries of $60,000 a year.

But by January, the price of Bitcoin was already on its way down—so much for all those jobs. At least the neighbors won’t have to suffer the noise anymore.

Last summer, Virginia Beach resident Tommy Byrns, told Wavy News:

“The issue is the noise, the relentless noise … it’s kind of created an atmosphere where we can’t talk to each other in the backyard. You have to go in the house to talk … this was pushed through without any warning into anybody … and now look what we have.”

Crypto, the movie, is out. Gerard wrote a full review for DeCrypt on his new battery-powered AlphaSmart Neo 2 keyboard—a 1990s flashback that keeps him from shit posting on Twitter. The film was mediocre—but it stars KURT RUSSELL.

The now-defunct Canadian crypto exchange QuadrigaCX was founded in November 2013. Where did its co-founders, Michael Patryn and the now-supposedly-deceased Gerald Cotten, first meet? Did they exchange pleasantries in the Vancouver Bitcoin community earlier that year? Did they meet online in some bitcoin chat forum? Or did they have other prior business dealings even further back?

New evidence uncovered by Reddit user QCXINT suggests that Cotten appears to have been involved with Patryn at Midas Gold, a Liberty Reserve exchanger, set up by Patryn in 2008.

Patryn and Midas Gold

Formerly Omar Dhanani, Patryn is a convicted felon who wasarrested in connection with online identity theft ring Shadowcrew.com in October 2004. He was 20 at the time. Working out of his parent’s home in Southern California, he was a moderator on the forum. He also offered forum members an electronic money laundering service. Send him a Western Union money order and—for a fee of 10% of a transaction—he would filter your money through E-gold accounts. E-gold was an early centralized digital currency. Dhanani served 18 months in a US prison and was released in 2007.

After the US deported him to Canada, Patryn picked up where he left off. In April 2008, he founded Midas Gold Exchange. He was listed as the company’s sole director under “Omar Patryn,” with a company address in Calgary—though he was living in Montreal at the time. A few months earlier, the digital currency exchange service launched on M-Gold.com. (Here is an archive of the site taken in its early days, and here is an archive showing an updated design taken just before things took a dive).

In January 5, 2008, the earliest entry on the website reads:

“We have finally launched this website, and are requesting that clients place all future orders through the Contact Us page. We have, of course, been in business since 2005 and hope to continue providing you with the same great service throughout the new year. Thank you once again for your business, and have a happy New Year!”

There are no names of actual people anywhere on the site. But an October 17, 2009, entry gives the impression that a whirl of activity is going on behind the scenes.

“We apologize for the delays experienced for many clients during the course of this week. We are currently undergoing a massive corporate restructuring. During this time, some exchange directions are temporarily disabled. All pending orders should be processed within one business day.”

Digital currencies listed on the site included E-Gold, HD-Money, WebMoney, WMZ E-Currency and AlterGold E-Currency. Midas Gold even started accepting bitcoin inJune 2011, but Liberty Reserve was by far its main money maker.

How Liberty Reserve worked

A Costa Rica-based centralized digital currency service, Liberty Reserve was like PayPal for criminals. You could use it to anonymously transfer the system’s digital currency LR, worth $1 apiece, to anyone who had an account on the system. The system served millions of users around the world before May 2013, when it was shut down by the U.S. government.

To set up an account on libertyreserve.com, all you needed was a valid email address. You could make up whatever fake name you wanted because the site had virtually no KYC/AML to validate identities. You could, literally, use the service to send huge amounts of money around the world without anyone batting an eyebrow.

There was one caveat. You could not fund your Liberty Reserve account directly. If you wanted to buy LR, you had to go through a third-party exchanger, such as M-Gold. Conversely, if you wanted to redeem your LR for cash, you also had to go through an exchanger.

LR exchangers would buy LR in bulk and sell them in smaller quantities, typically charging a 5% transaction fee. This setup allowed Liberty Reserve to avoid collecting banking information on its users, which could leave a financial trail—exactly what criminals want to avoid when choosing a digital currency.

Founded by Arthur Budovsky and Vladimir Kats, Liberty Reserve went into operation in 2005. Eight years later, the system had more than 5.5 million users worldwide and processed more than $8 billion. Most of that volume came from the U.S.

During 2009 to 2013, Liberty Reserve was in full swing. These were the sunshine days of its criminal activity. A huge number of transactions were related to high-yield investment programs—better known as Ponzi schemes—credit card trafficking, stolen ID information and computer hacking.

Cotten’s email

A data dump—in one of the USA v. Kats et al. court exhibits (see attachment #180 for GX 1305) related to the takedown of Liberty Reserve—shows that Midas Gold ranked 342 of the top 500 Liberty Reserve accounts in volume.

The name on the Midas Gold account is Omar Patryn, but the email address linked to it is geraldcotten@gmail.com. What does this mean? It means whoever owned that email had the authority to operate the Midas Gold account for Liberty Reserve. They could reset the password, enable or disable 2FA, and authorize transactions.

The data indicates Midas Gold bought up more than $5 million worth of LR. At 5% of a transaction. That equates to profits of around $250,000—not a lot, but decent wages.

Rank: 342, Category: Exchanger, Associated website: http://www.m-gold.com, All currencies: $5,221,489.02, LR: $5,081,353.88, Account name: Midas Gold Exchange, First name: Omar, Last name: Patryn, Email: geraldcotten@gmail.com

The email suggests that Cotten and Patryn may have worked at M-Gold.com together—though its not clear if Cotten was involved from the beginning or joined later. If anything, this could even suggest that Cotten had more control over Midas than Patryn.

Let’s pause for a moment. If you were going to be involved in a dodgy business, why would you use an email address that pointed directly to you? That seems like a dumb thing to do, but then Cotten was still a young con at this stage. Maybe this was a rookie mistake. Also, is this really Cotten’s email? Quite likely, yes.

We think this is his email because he appears to have used the same email address for several domain registrations, including,cloakedninja.com, where you could buy proxy sites to hide your IP address, andcelebritydaily.net, an entertainment news blog. A historical WHOIS data snapshot of these site reveals they both have a registration address of 346-1881 Steeles Ave W Toronto. Quadriga Fintech Solutions, the owner and operator of QuadrigaCX, is linked to the same address.

Patryn’s Liberty Reserve account

In addition to the Midas Gold account, Patryn had his own account on Liberty Reserve, but his account had no associated website. He appears to have had at least three other exchangers at the time—HD Money,E-cash World and Triple Exchange. It’s possible he was selling LR through those sites as well as Midas Gold, and was just using the one account. Or else, Cotten could have operated Midas alone, while Patryn handled the other businesses.

Approximately $18.4 million worth of LR went through Patryn’s Liberty Reserve account. Of Liberty Reserve’s 500 largest accounts by volume, his ranked 88. If he took a 5% cut of every transaction, he would have pulled in $920,000.

Rank: 88, Category: Exchanger, Associated website: [field empty], All currencies: $18,653,708.71, LR: $18,416,444.50, Account type: Currency, First Name: Omar, Last Name: Patryn, email: admin@patryn.com

A passage from the court filing explains:

“Data obtained from Liberty Reserve’s servers reflects the extensive use of the company’s payment system by criminal websites. The Government analyzed the top 500 accounts by transaction volume, i.e. funds sent and received, to attempt to determine the type of activity associated with each account. The total transaction volume for these accounts is approximately $7.26 billion, or approximately 43% of the total volume of transactions on Liberty Reserve’s entire system.”

Also according to the analysis, of the top roughly 500 accounts, 44% were associated with exchangers, 18% could not be categorized, and the remaining 38% were categorized as follows:

“157 of the accounts, accounting for approximately $2.6 billion in transactions, were associated with some form of purported ‘investment’ opportunity. The vast majority of these accounts were linked to websites that, on their face, were clearly ponzi schemes, i.e., HYIPs. Others, at best, were associated with unregulated ‘forex’ (foreign currency trading) websites—which are likewise known to be prominent sources of fraud.”

The demise of Liberty Reserve

Good things never seem to last, and in May 2013, Budovsky was arrested in Spain for running a massive money laundering enterprise. Kats was arrested in Brooklyn, and the the domain libertyreserve.com was seized.

Shortly afterward, US authorities seized more than 30 domains registered as Liberty Reserve exchangers in a civil forfeiture case, including M-Gold.com. According to court docs: “The defendant domain names were used to fund Liberty Reserve’s operations; without them, there would not have been money for Liberty Reserve to launder.”

Following the shut down of Liberty Reserve, users were told to contact the court to recoup their lost funds—on the basis they were conducting legitimate business. According to court docs filed in April 2016: “Notwithstanding that Liberty Reserve had more than 5 million registered user accounts, only approximately 50 individuals have contacted the Southern District Court of New York since May 2013.” Most appeared to be victims of HYIPs and other scams. And only one Liberty Reserve exchanger contacted the court about a potential claim—and that claim was not pursued.

A few months after M-Gold.com was seized, QuadrigaCX launched in beta. The rest is history—or history in the making—depending how you look at it.

Did you like this story? Please support my work onPatreon, so I can keep on doing it.

I had to take my website offline for a few hours Tuesday, so if you were searching for one of my stories and got a weird message, my apologies. I asked WordPress to downgrade my site from a business plan to a premium plan, and when they did, a bunch of my content disappeared, so I had to put Humpty-Dumpty back together again.

Big thanks to my now 18 patrons, who are making it easier for me to focus on writing about crypto. If you like my work, please consider supporting me on Patreon, so I can keep doing what I am doing.

Now onto the news, starting with Quadriga, the defunct Canadian crypto exchange that I won’t shut up about. (Read my timeline to get up to speed.)

Ernst & Young (EY), the court-appointed monitor charged with tracking down Quadriga’s lost funds, released its fourth monitor report, which reveals more money going out then coming in. The closing cash balance for March was CA$23,268,411. Incoming cash for the month was CA$4,232, and total disbursements was CA$1,463,860—most of which was paid to professionals. A full half of that (CA$721,579) went to EY and its legal team.

EY is trying to chase down money held by Quadriga’s payment processors. It has drafted a “Third Party Payment Processor Order” for the court to approve on Monday. If that goes through as is, several payment processors, including WB21, will have five business days to handover funds and/or Quadriga documents and transaction data. If they don’t comply, they will be in contempt of court. A shift from CCAA to bankruptcy proceedings will also give EY more power to go after funds as a trustee.

Christine Duhaime, a financial crimes lawyer who worked for Quadriga for six months in 2015 to early 2016, wrote “From Law to Lawlessness: Bits of the Untold QuadrigaCX” for CoinDesk, where she talks about how Quadriga went off the rails following its failed efforts to become a public company.

In the article, Duhaime—who in February called for a government bailout of Quadriga’s creditors (archive)—openly admits to having lost CA$100,000 in funds on the exchange. She claims her involvement with the exchange stopped in early 2016. “I’m glad we were let go by QuadrigaCX for being one of the ‘law and order’ folks,” she said.

I have been corrected on detail here:

She does not mention this in her article, but in 2015, she also owned 20,000 shares of Quadriga stock. It is possible she has since sold the holdings.

Preston Byrne, an attorney at Byrne & Storm, PC,tweeted, “No offense to @ahcastor but this claim that @cduhaime may have owned shares in Quadriga looks to be incorrect. She’s listed as the principal contact for an SPV, and the SPV is the named purchaser. A retraction is in order.”

SPV stands for special purpose vehicle, typically used by firms to isolate them from financial risk. I’ve reworded the paragraph as follows:

This 2015 British Columbia Report of Exempt Distribution, a document of Quadriga Financial Solutions’ ownership, lists Duhaime as the contact for 1207649 B.C. Ltd, which owns—or owned—20,000 shares of Quadriga. I was unable to find the corporate files for 1207649 B.C. The address in the report matches that of Duhaime’soffice.

Update (April 9): I found the corporate files. The actual company name appears to be 1027649 B.C. Ltd.—with the numbers “2” and “0” transposed. The company was founded on February 16, 2015 and dissolved on August 1, 2017. The sole director is “Anne Ellis,” and the registered office is Duhaime Law.

According tocourt documents, Cotten and Quadriga co-founder Michael Patryn had been seeking to buy back shareholdings after Quadriga’s public listing failed, so it is possible one of them may have bought back those shares as well. I reached out to Duhaime for comment a few times, but she has not responded.