Avid bitcoiner Peter McCormack released a podcast interview (archive) with two Tether/Bitfinex frontmen today—CTO Paolo Ardoino and General Counsel Stuart Hoegner.

McCormack is a well-known Tether apologist whose podcasts are funded almost exclusively by bitcoin companies. Tether is also paying his legal fees in a libel suit brought against him by Craig Wright. Despite that, McCormack claims to be completely objective, although he makes it clear he believes all the “Tether FUD” circulating on Twitter stems mainly from “salty nocoiners,” who are upset because everyone is getting hilariously rich with bitcoin but we’re not.

I’ve transcribed the interview and added my comments. I skip the first few minutes of the interview where McCormack lists his numerous crypto sponsors and goes on to say he thinks Tether is legit. I’ve also edited out the “uhs,” and some repeated words to make reading easier.

Peter: Can you just explain to me and for other people who are listening, because they probably don’t really fully understand it, how tethers are issued and redeemed?

Stuart: Let’s be clear on our terminology, if we’re going to talk about issuances and redemptions. We use four principal terms when we talk about this: authorized tethers, issued tethers, redeemed tethers, and destroyed.

Authorized tethers are tokens that are created on a blockchain, and they’re available for issuance to the public. This process involves multiple blockchains and multiple persons participating to sign creation transactions. Once created, they’re available for sale to third parties, but until then, they sit in Tether’s treasury as authorized but not issued.

These authorized-but-unissued tokens aren’t counted—or [are] not counted—in the market cap of tethers as they have not been issued or released into the ecosystem. You should think of them a little bit like an inventory of products that are sitting on the shelf that are awaiting purchase.

Issued tethers are authorized tokens in actual circulation, and they have been sold to customers by Tether and are fully backed by Tether and the reserves, unless, and until they’re redeemed.

As tokens are issued, the stock of authorized-but-not-issued tethers, is depleted. And they’re replenished through authorization of new tokens based on market demand. When that happens, this is what Paolo is referring to in his PSA on the replenishment of the tether inventory. This is adding to the authorized and unbacked and ready for sale, but not issued, sold and backed tethers.

(I love how Hoegner makes it clear that authorized tethers in the hundreds of millions, like this one here, which we see going out via @whale_alert, are not actually backed. They’re just tethers on the shelf. Tether has issued $24 billion in tethers to date—and nearly 20 billion of them since March 2020.)

Peter: Okay. Why do you need to do that? Because I would have thought the creation of tethers is a very simple and easy job. Why do you need to leave them on the shelf?

Stuart: It’s a straightforward job, but it’s an important job. And it’s one that comes with security risks, and Paolo can speak to this a little bit. But there are security risks involved in using sensitive private keys to create new tethers, authorized. And to have those at the ready, and not in the marketplace, not backed. That exposes those keys to less risk. That’s not just a theoretical risk—there’s a serious security risk associated with that. Paolo, do you want to speak about that?

Paolo: Yeah, I believe that we can think [of] Tether authorization, private keys as among the most important sets of private keys in our industry. If you get hold of the private keys, you can really issue any amount of tethers you want. What we want to do is to limit the number of times per week when these private keys get accessed by signers.

So, having an unsigned [ro? roll?] transaction that gets prepared with a fixed amount and then signed when they need to, that really helps tether security. Because then you can see that we are issuing round numbers, like $200 million, right?

It means that we pre-prepared a [ro?] transaction that is an authorization transaction. Then tether signers, sign that transaction and broadcast it. And as Stu said, we are leaving a bit of inventory on the shelf in order to fulfill what we think that future requests from customers could be.

(The inventory does fly off the shelf pretty quickly. You can literally watch in realtime tethers shooting off to crypto exchanges Binance, Huobi, Bitfinex, and lots of unknown wallets, where they are quickly put to work.)

In our day-to-day activity, we are always in talks with customers. So, we [have] a good sense of what they might need, or they ping us in advance and they say, okay, we might need a certain [of] this amount or we might need that amount of tethers. In time, we learned how much tethers we should authorize in advance and keep it on the shelf in order to make these tethers available as soon as they are needed. But at the same time also protecting the security of tether, not continuing to touch the private keys every single time there is just one insurance.

Peter: Okay, I’m going to just push back on you saying they’re the most important private keys in the industry. I would say, personally, my private key is the most important one. Outside of that, I would probably say wherever the biggest honeypot is, maybe it’s Satoshi, his private keys, are the most important because Bitcoin is completely censorship resistant—but Tether isn’t, right? You can, if required, censor transactions. You can, if somebody issued a bunch of fake tethers, you could block those, I believe.

Paolo: First of all, I agree that bitcoin private keys are, well, everyone’s private keys are like their own babies. No doubt about that. The difference as you said is that if someone gets ahold of the private keys in tether, they can issue anything that they want. While in Bitcoin, if someone gets hold of the private keys, they can just steal the funds of the people that got hacked, rather than minting fake bitcoins.

So this is really important, and this is the reason why we want to keep these private keys so secure and touch them as little as possible.

So, yes, we can freeze, fake tethers. But at the same time, you can imagine if someone gets ahold of the…in order to freeze tethers, someone has to have the private keys. But if someone already has the private keys, then he can unfreeze our attempt to freeze tethers.

So we will become an endless attempt of freezing and unfreezing and trying to save tether. That is not ideal. The responsible thing to do is touch the private keys as little as possible and use, of course, for our blockchain, we use a multisig approach. So there are multiple private keys held by different signers in geographical different [locations] so that we can ensure the highest security possible in all our operations.

Peter: Stuart, I interrupted you, you were going to talk about redemptions. We should finish that bit off.

Stuart: Sure. So redemptions are just when customers send their tokens back to tether and they get fiat back and return. Those tokens then go back into inventory, like their products that have been returned to inventory, awaiting future purchases. And then those tokens can be held by tether and its treasury or destroyed.

And then destruction is just, multisig transactions being broadcast to reduce the number of outstanding tokens existing on the selected blockchain. And those tokens are forever eliminated. Basically, that’s the reverse of authorization. So those four concepts you have the lifecycle of the tether.

(The only time we’ve seen Tethers destroyed was in October 2018 when Tether burned 500 million USDT. This was just after Bitfinex lost access to $850 million in the hands of its Panamanian payment processor Crypto Capital, and the NYAG began investigating Tether/Bitfinex for fraud. Hoegner confirms our suspicions that once tethers are created, they are generally never uncreated.)

Peter: So, Paolo, who is using tethers. What are they using it for and what is the KYC process for people who want to use tether? And actually I’ll throw another one in there: who can’t [use tether]? Who applies and who do you turn down?

Paolo: Let’s start with who uses Tether. I think Stuart can speak better about the KYC/AML process,

Tether was born in 2014. It started from the Omni Layer. And the reason why it was born is because there was an issue among crypto trading exchanges. In 2013, Bitcoin reached, for the first time, $1,000, but across different exchanges, you [could] see that the spread was $200 to $300. And the reason was pretty simple.

Bitcoin moves with the pace that is every 10 minutes because that is the average block time, while dollars and fiat in general move much slower. So you send a wire and you can take one day, five days, and that was not allowing proper arbitrage across platforms. And that is really important for healthy markets. You don’t want to have OKCoin to be $1,000 and Bitfinex to be [$1,300] and so on. That is the job of arbiters. They step in and try to close these gaps.

But with just fiat, it was really difficult in 2014. It is slightly a bit better now, but you want both legs of a trading pair, like BTC/USD, to move at the same speed, at the same pace. And the only way to do that was to use the same underlying technology. So, the Omni Layer was and is using Bitcoin transactions to move tethers on-chain. That was the perfect use case. And so tether was born for that specific reason—to solve a problem

Recently, of course, we started to look into different use cases because I believe that is the time that tether should outgrow the crypto market. That is still our main market, but we are looking to work with [inaudible] businesses that offer remittances, businesses that want to optimize their payment solutions—payments for salaries, for inventory, for anything. So we got bombarded on a daily basis [with] requests. And that’s pretty awesome because we don’t want to be only for crypto. We were born in crypto, but we want to go on a global scale. So, Stu, you may or may want to touch base about our process onboarding customers.

(Tether first started issuing tethers in large quantities in 2017, after Bitfinex lost its banking. Note that Ardoino is trying to say that Tether’s massive issuance of tethers over the course of 2020 was due to expanded growth—e.g., we want to go global. Of course, there is no evidence of Tether being used outside of crypto except for online gambling in China. And the idea that businesses would want to use tether to pay salaries makes no sense, as you can’t pay rent and buy groceries with tethers.)

Stuart: Sure. I’m always happy to discuss this, because contrary to the online characterizations in some quarters, tether has an outstanding compliance program. Our AML and our CTF sanctions program is built to exceed or meet the standards of the U.S. Bank Secrecy Act and applicable BVI laws. We work hard to detect, monitor and deter AML/CTF violations. And our program is tested periodically by independent third-party auditors. We always work to understand the identity, business type, source of funds, and the related risks of each and every customer on tether. And we conduct enhanced due diligence on all customers. We risk-rate every customer. We monitor all customers using World-Check and we deploy Chainalysis to detect potential crime related to our services and users.

We regularly help international law enforcement agencies with investigations in order to trace and potentially freeze wallets. Also, tether will share information with law enforcement when given valid legal process, and we’ve helped law enforcement and victims to freeze and return millions of USDTs. That’s a bit of an overview of our compliance and what we look to do.

(Hoegner claims Tether does due diligence and knows who its customers are, but who are its customers? Further along in this interview, he hints that Tether’s customers consist of a small group of “large customers,” likely exchanges and OTC desks, that bank with Deltec Bank & Trust. What about the hundreds of thousands of tether users? They are apparently not counted as customers. This leads me to think that Tether’s “big customers” serve a function akin to Liberty Reserve exchangers—acquiring tethers in bulk directly from Tether and then distributing them in smaller quantities to individuals who require anonymity in their transactions.)

Peter: Have any customers ever lost their account?

Stuart? Lost their account?

Peter: Yeah. Have you ever closed people’s accounts? They can’t work with you anymore. Have there been in any instances where you’ve tracked behavior and, like, you can’t work with us anymore. Or has everyone kept a clean relationship?

Stuart: We have ended relationships with customers in the past. Sure.

Peter: Okay. Interesting. In terms of the issuance of tethers, there’s a lot that seems to happen on times when banks essentially would be closed, right? So weekends and holidays. There was certainly some over the holiday break, and I’ve seen people commenting on that. How come that’s happening? How are you able to do that?

Paolo: I will take this one. So you’re right. There is a lot of misconception and FUD around this very point. You would expect that to go to HSBC on Sunday and it is closed, so you cannot move your money. Right? We, as Tether, are using Deltec as a primary bank, and most of our biggest customers are banked into the same bank.

(They claim Deltec Bank & Trust is their main bank. If most of their “biggest customers” have accounts at this tiny bank in the Bahamas, that likely means Tether doesn’t have a lot of what it considers customers.)

During the weekends, during all the days, there is always personnel from the bank that allows internal transfers between accounts. So, Tether has its own accountant, and let’s say, customer A has his own account. Customer A wants to acquire new tethers. So they ask the bank personnel to do an internal transfer from their account to Tether, a Deltec account. And that gets settled and is available immediately to tether.

So, when we issue tethers, they are fully backed because we already received the internal transfer. So, the problem that people are making fun of—the fact that we are issuing over weekends—is just pure [mis]understanding on how the financial market and the banking system works.

(It sounds here that one of the advantage of being a big Tether customer with a Deltec account is you have a close, trusted relationship with Tether. Also, we are definitely seeing a trend where the BTC price is pumped on the weekends, followed by a selloff on Mondays.)

Peter: You mentioned Deltec. Are you shareholders in the bank?

Stuart: We don’t talk about the investments that we have on the Tether side.

Peter: Okay, so are tethers fully backed?

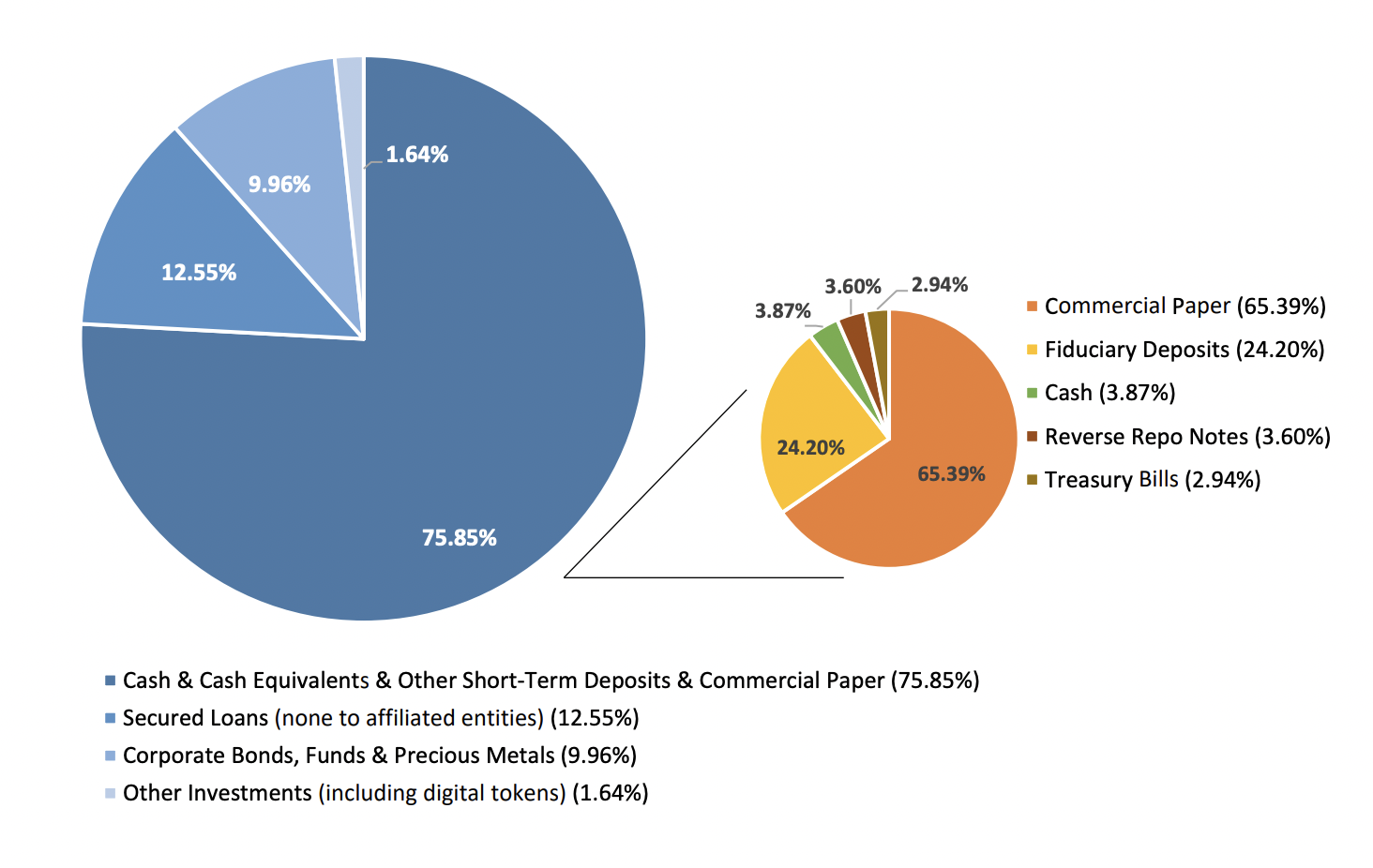

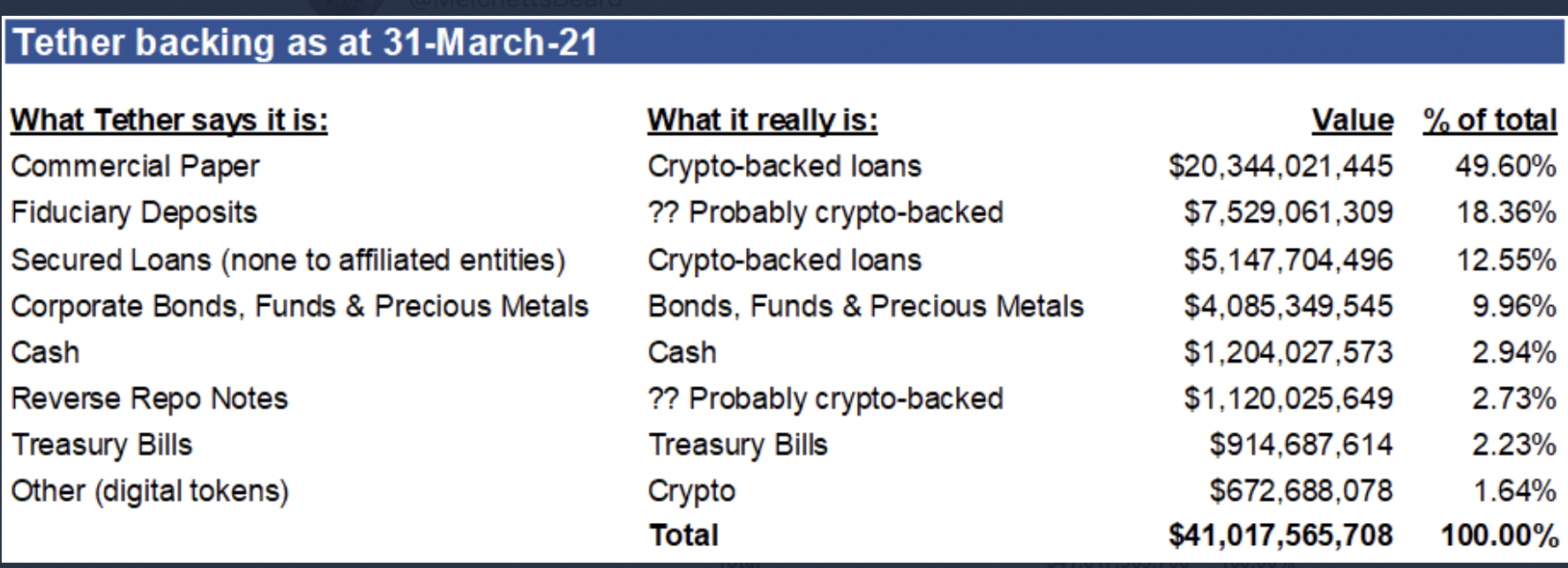

Stuart: Look. The short answer is yes. Every tether is 100% backed by our reserves. And those reserves include traditional currency and cash equivalents, and may include other assets and receivables from loans made by tether to third parties.

(Essentially, tethers are backed by cash and a bunch of other stuff that Tether won’t disclose. For years, Tether claimed that tethers were backed “1-to-1” by U.S. dollars held in cash reserve. Tether changed the rules of the game in 2019, after Bitfinex lost access to $850 million and had to dip into Tether funds. Tether’s terms of service now states that reserves means “traditional currency and cash equivalents and, from time to time, may include other assets and receivables from loans made by Tether to third parties, which may include affiliated entities.”)

Now that lending includes the loan to Bitfinex, which currently stands at a principal balance of $550 million. The principal having been paid down ahead of schedule. The loan is on commercially reasonable terms. All interest is prepaid to the end of this month, and it’s otherwise in good standing.

(Bitfinex indicated previously—here and here—that it has already paid off $200 million of the funds it took out of Tether’s reserves in early 2019. If the remaining balance is $550 million, that means the total was $750 million.* Also, he is including the loan as a legitimate part of Tether’s reserves, which makes absolutely no sense at all. This is missing money, so how can it be used to back anything? Also, note that Hoegner keeps referring to Tether’s original loan to Bitfinex and claiming it is insignificant and paying interest. But his language does not exclude the possibility that Tether has made other loans to other customers or even to Bitfinex itself.

Here’s how the “loans” part might work: Even though Tether could say that it issued USDT—say to Bitfinex—in exchange for USD or BTC, Bitfinex does not have to actually hand over the USD or BTC right away. It can just promise to do so. Then that promise can be counted as a loan that backs those USDT.

And one more thing—what happened to the $1 billion that Bitfinex raised when it sold all those LEO tokens? I would have thought that would have been plenty to cover the $700 million loan.)

Every USDT is also pegged one-to-one to the dollar. So USDT is always valued by tether at one USDT to one USD. Tether has always been able to honor redemption requests, and to put it simply, there’s never been a single instance in which tether could not honor a redemption and our detractors can’t point to one because one doesn’t exist.

And in fact, there’s considerable evidence of USDT being redeemed by our customers, freely. [Cofounder of CMS Holdings] Dan Matuszewski has talked about this before. [Head of OTC-APAC at Alameda Research] Ryan Salame just recently spoke about this, confirmed.

We can’t share specific information about customers because of confidentiality concerns. But they are free to share that information with the market, if they wish.

(Ryan Salame said in a tweet that he has been redeeming tethers for three years, but he doesn’t say for what, so we don’t know if it was an actual dollar redemption. Matuszewski said in the past that he “created and redeemed billions of tethers” when he was head of Circle’s OTC desk.)

So let me just ask if anyone seriously believes after we, you know, that we could be put under the microscope in the way that we have and still be operating if we weren’t backed. Defies logic.

Let me touch on one issue here that might be of interest to your listeners. The 74% number that’s come up from time to time, specifically in the context of tether’s backing. This is another number that’s been talked about a lot, and I want to be clear about this and give some context.

I swore out an affidavit in New York, in the New York litigation with the AG on April 30th of last year. And that affidavit contained a number of items, including touching on tether backing.

And in a statement, I said that of the then $2.1 billion in reserves. And today, just for context, that amount has grown to $22 billion.

Tether had cash and cash equivalents on hand representing approximately 74% of the current outstanding tethers. And that referred to issued tethers. You remember, we were talking about authorized and issued tethers, et cetera? That was issued tethers.

People took from that, that I said, this means they’re only 74% back. But that’s not correct. And that’s not what I said. It meant and means that the reserves were 74% cash and cash equivalents. Tethers were and are 100% backed by reserves.

So the loan to Bitfinex is still good backing. Interest has been paid ahead of schedule, as I said, and the principal has been repaid again, ahead of schedule.

So that forms part of tether’s reserve backing. So maybe people object to the amount of the backing, but it’s not nothing. It’s a valuable and productive asset. And just note that that loan is now $550 million, out of almost $22 billion in reserves, or 2.5% of the total. So I just want to be clear about the nature of the backing and the context and our overall asset mix on that point.

(Hoegner is backtracking and doing his own math to now claim that Tether has always been 100% backed. This is nonsense. He said in an affidavit in April 2019 that tethers were 74% backed. The truth is nobody really knows what is behind tethers and what difference does it make anyway? Tether makes it clear that it is not obligated to redeem tethers at all, and if it does, it can hand you back whatever useless assets it wants.

According to its terms of service, “Tether reserves the right to delay the redemption or withdrawal of Tether Tokens if such delay is necessitated by the illiquidity or unavailability or loss of any Reserves held by Tether to back the Tether Tokens, and Tether reserves the right to redeem Tether Tokens by in-kind redemptions of securities and other assets held in the Reserves.”

Peter: Okay. So you talk about the backing of currencies and different currencies. Is any of the backing in Bitcoin?

Stuart: We were very clear last summer in court that part of it is in bitcoin. And if nothing else, there are transaction fees that need to be paid on the Omni Layer. So bitcoin was and is needed to pay for those transactions, so that shouldn’t come as a surprise to anyone. And we don’t presently comment on our asset makeup overall as a general manner, but we are contemplating starting a process of providing updates on that on the website in this year, in 2021.

Peter: But you have to manage the assets that back the tether. Are there any instances where you are buying bitcoin because you think it’s a good asset to hold within the basket?

Stuart: Again, we don’t comment on the basket of assets in a general manner, but we are exploring providing updates on that on the website in 2021.

(Hoegner won’t reveal what sort of assets are backing tethers. If it’s only partly cash, what part is cash? And what is the rest made up of? Tether has so far issued $24 billion worth of tethers, but it is not telling customers what is behind those tethers—for all we know, nothing but a lot of worthless assets.

Peter: Okay. Because that’s one of the areas where people will be like, hmm, they can issue tether. They can buy the bitcoin, which backs the tether, at the right time in the market. And that’s where people might say that you have the ability to essentially pump the market.

Stuart: Well, hold on, we don’t have the ability to buy the bitcoin at the right time in the market. We’re not prognosticators about whether the market’s going to go up or down. That presumes some level of clairvoyance that we know when markets go down, which we don’t have.

Peter: No, it doesn’t mean that. I just mean that if you have to manage your basket of assets and if bitcoin, was say…any investment you have to make, you have to make a decision. You could make a decision and say, look, we believe that bitcoin would be a good investment right now. And you could issue tethers to buy bitcoin.

Stuart: No, no, we don’t issue tethers to buy bitcoin. We issue tethers to customers that want tethers.

Peter: So how does bitcoin end up within your basket?

Stuart: Well, as I said, if nothing else, bitcoin is there to pay for transactions on the Omni Layer.

Peter: No, no, but how does it get there? How does, what’s the process of the bitcoin reaching your basket?

(This is a good question. If bitcoin is backing tethers, what is Tether using to buy those bitcoin with? Notice how Hoegner is being very careful not to say that they are buying BTC with tethers. Well, what else would they be buying them with? Why not hand tethers out to Tether customers in exchange for BTC? Or you could set up an account on Bitfinex, fund it with tethers, and use those to buy BTC from your own customers on the exchange.)

Stuart: Oh, Paolo, do you have any comments on that?

Paolo: I’m not sure if the question is really clear. We talked about the fact that how we acquire the bitcoin that we need in order to fulfill the Omni Layer transactions.

(Ardoino is pretending like he doesn’t understand the question.)

Stuart: So how do we get that bitcoin, Paolo?

Paolo: I would say that [there] are a good amount of bitcoin remaining from past acquisitions that we likely did in 2015, 2016. That with the fact that the Omni Layer is slowing a bit down compared to the other blockchains that we are supporting…the amount of bitcoins that we luckily got a really good price in 2015 and 16, is probably enough for perpetuity.

(Now he is saying that they happened to have a stash of BTC lying around from five or six years ago, and that’s what they are using to back tethers. If Tether had a stash of bitcoin that large, it could have sold them long ago and taken care of the $850 million hole left when the money disappeared from its payment processor.)

Stuart: But again, Peter, let me emphasize, this has been in the public records since at least last summer. In my view, this isn’t new or shouldn’t be new to anyone.

Peter: What I’m trying to understand is, if it’s only bitcoin, that’s held for transactions on the Omni Layer. I understand that. But if bitcoin is held within the basket because it’s seen as a good asset to hold, then how does it end up there? I’m just trying to understand that.

Paolo: So, but why we should issue—even in the case someone would like to add the bitcoin to its own basket. Why issuing tethers to do that? Right. So there are fiat exchanges. So why, if someone wants to manage his portfolio would just take part of dollars and buy bitcoins. So why issue tether to do so?

Peter: I don’t know. That’s why I’m asking.

Paolo: In any case, the entire concept of us issuing tether to buy bitcoin for ourselves, doesn’t make sense. So why issuing tethers when we already have the dollars and we have the ability to manage our inventory and our portfolio, so we could just use the dollars, right? So the entire narrative is completely nonsense, right? So why we have to do two steps when we can do one?

(Ardoino wants us to believe that if Tether wanted to buy bitcoin, it would simply go to a banked exchange and buy BTC with cash. But why would Tether use cash to buy its stash of bitcoin if it has copious tethers on hand? He is doing a terrible job of trying to evade this question. )

Peter: That’s fair. Okay. Okay.

In terms of an audit, this is something that comes up over and over. And I discussed this with Phil Potter a long time ago. I know you’ve got it on your website, but people don’t trust your own lawyers providing the audit. Is there anything stopping you from having a full and independent audit?

(The only thing that would remove all doubt that Tether has any cash or reasonable assets backing tether at all, would be an independent audit. But Tether and Bitfinex have consistently avoided this over the years, and they always have some excuse.)

Stuart: We spoke about this two and a half years ago when we said that we couldn’t get an audit in part because of the amount of business that we had at a single financial institution at that time.

We have provided consulting reports from our accounting firm. I think you’re referring to these in your question, from a law firm, Freeh Sporkin Sullivan, a firm of ex-federal judges and an ex-director of the FBI, and a letter from our bank.

And those were good faith efforts to try to provide transparency, and some of the comfort that assurance services would provide. We said at the time that we continue to search for new ways to bring more information to the community. I mentioned Ryan Salome’s remarks earlier, that’s part of those efforts. Interviews like this are part of those efforts, public comments from our bankers are part of those efforts.

So we continue to look for useful ways to share information with the community, to be more open and transparent. And we have important plans in that regard for the coming year. But I can’t get into specifics on that just now. So all I can say on that one is stay tuned.

Peter: Well, we can keep talking. Okay. So the reason I reached out to you is I get a lot of DMs, a lot of emails, and just suddenly over the last couple of weeks, I’ve had so many about tether and I’m posting things online and people say, it’s tether manipulation, and I haven’t seen it in a long time.

Now that I’ve done my own research. I don’t believe tether is manipulating the market.

Stuart: Few serious people do.

Peter: And that’s what I realized, few serious people do. So my question really is for you is where do you think this is coming from?

(I love how McCormack is acting like it is a complete mystery why anyone would think Tether is anything but a completely legitimate operation.)

Stuart: That’s a good question. I couldn’t hazard a guess. I think it’s probably nocoiners that just don’t believe in the bitcoin project and by extension, they don’t believe in Tether. It could be people with their own agenda. That’s really not for me, for us to speculate.

But, we’ve noticed the same thing, Peter. Like this comes up from time to time. It’s almost a six months schedule. Every six months or so, there’s some kind of huge push to get a whole bunch of FUD out there. And it can vary as to the reasons why. This current batch might be related to the January 15th date that people have been talking about in the NYAG litigation.

Peter: Well, I’m going to ask you about that, but you’ve got people like Nouriel Roubini, Amy Castor, Frances Coppola, all quite openly accusing you of manipulating the market and running a pump with tether to pump bitcoin. So they’re quite serious allegations from quite known profiles. Have you not considered any litigation against them for libel?

(I’m truly flattered my name would come up here. Nocoiners believe Tether has printed billions of unbacked tethers out of thin air because Hoegner has flat out admitted in court documents that tethers are not fully backed. And he is telling us here, again, in this interview, that they are backed by mysterious assets, nonsense loans and goofy math. We believe Tether is manipulating the markets because we know for a fact that more BTC are traded against USDT than fiat. I find it amusing McCormack is suggesting Tether sue us all for libel.)

Stuart: Look, we don’t believe in suing our critics into silence. We have never made a claim against anyone for defamation. It’s not to say that we wouldn’t ever, but it would be a high bar. We think it’s better to try to counter fiction with facts and truth. And in fact, contrary to what some may think we’re not particularly litigious people. And that obviously, for what it’s worth, extends to journalists as well. We’re not about to hail Forbes media into federal court in New Jersey. As to why Nouriel, why Frances, why Amy, are engaging this kind of discussion, these kinds of statements. You’d have to ask them.

(We engage these kinds of discussions because Tether/Bitfinex have failed to provide evidence that Tether is fully backed and the companies have a long history of shenanigans. Also, the NYAG is investigating you for fraud.)

Peter: Yeah, fair enough. Okay. If you look back historically, because you’ve had all these accusations, you have to deal with all this pressure. Is there anything where you look back and you think, okay, we did that wrong? We’ve handled this in the wrong way. Are there things you should have done better, should have done differently?

Stuart: Absolutely. Look, for people out there that are true skeptics, and I’m not talking about deniers, not haters, that it will never be convinced. I think one thing that we could have done better in the past and we’re getting better at now is communications.

And that’s not a reflection on anyone. Paolo’s brilliant at this stuff, just like he is with everything else. He’s a brilliant guy. Joe Morgan is great whom, you know. And we have very capable defenders out there, making our case for us. But we’ve been so focused on building cool things that we have—and I’ve said this publicly–we have neglected our comps. We have always known that we are a tech firm or not a law firm. We’re not a PR shop. We’re not a compliance shop. Although compliance is very important.

And mea culpa. I want to be clear I’m as guilty of this as anyone else to the extent that I haven’t prioritized public communications. And I’ve said in the past, some of the FUD, it will just go away. You know, let’s not give it oxygen. I was wrong about that. So you can blame me for that. But we are getting better at communicating with people. We’re getting better at this. We’re learning. We’ll continue to learn, and we’ll continue to improve and get the facts and evidence out there.

Peter: All right. Let’s talk about the NYG case. For those people who don’t know, because it is quite complicated, how would you summarize the accusations?

Stuart: Let’s start with some baseline information on NYAG. First, there is no lawsuit or complaint that’s been filed against Bitfinex or tether in New York by the AG.

Second, this is not a criminal investigation. And third, the special proceeding is only directed at getting information and keeping the injunction in order for the AG to conduct her investigation.

Now, Bitfinex and Tether have cooperated with the AG’s office for over two years and have produced approximately 2.5 million pages of materials. While the AG’s office originally obtained an injunction relating to Tether’s reserves, in April of 2019, that injunction was substantially narrowed in the ensuing weeks and has not disrupted the day-to-day business of either Bitfinex or tether. And the injunction in the order for information is what we’ve been referring to online when we speak about the 354 order.

So the injunction set to expire by its terms on January 15th, which is the January 15th date that I referenced earlier that people have been talking about. And by that time, the companies expect to have finished producing documents to the attorney general.

So we’ve seen a lot of FUD and fear-mongering about January 15th, much of it by those who hate, not just tether, but the entire digital token ecosystem. Despite those rumors and attacks, let me assure you that the business of tether and Bitfinex will remain the same after January 15th. I think our discussions with the AG are going well. I think they’re constructive. And we look forward to continuing that conversation with them.

(The Jan. 15 date he is speaking of refers to the date Tether/Bitfinex are supposed to handover their financial records to the NYAG, so the investigation into their business can proceed. The NYAG letter to the court is here.)

Peter: But what is it they’re pursuing here, particularly?

Stuart: The original order had an injunction component, enjoining us from doing certain things, which doesn’t affect our day-to-day business, at this time. It also sought information. So if you go through all of the requests that were in the original order from last April, they set a series of things that they wanted, a series of documents, information they wanted from us.

We pushed back on that. We appealed the New York Supreme Court’s ruling on that. We lost. We accept that, and we’ve mediated our disputes as the attorney general said in their letter to the courts a few weeks ago. So again, they’re looking for that information. We are in the course of providing that. That’s going to be done by the 15th and we’re continuing to talk with them.

Peter: So what, what happens after the 15th? What are the next steps in this, because two years is a long time. I’m sure you want this wound up as quickly as possible. What are the next steps after that?

Stuart: Time will tell. Again, our discussions with them are constructive. We’re on track to give them everything they’re looking for. And we’ll see where it goes.

Peter: Okay. I’m trying to understand what the various possible outcomes are from this and whether you can even talk about them. Is there a scenario where Tether is wound up? Is there a scenario where Tether is just fine and is there a scenario where they actually complete their investigation, and there’s no action to be taken?

Stuart: Certainly. They may complete their investigation and they may bring a complaint. They may complete their investigation and think that there’s nothing further to be done. There may be some kind of settlement between the parties. There are any number of things that could happen.

Peter: What about the other lawsuit? What about the other one I read about, there’s a class-action lawsuit regarding the traders. Where are you at with that? You applied to have that ended, right?

Stuart: Yeah, so we have filed our motion to dismiss and the plaintiffs have given a reply in that, and we are waiting at this point to see if there’s going to be oral argument on the motion.

Peter: Okay. Just on the regulation side. It’s quite an interesting time for, I’m going to say crypto, and I hate that word, but crypto slash bitcoin slash stable coins and very interesting things that happened with the OCC recently. It feels like there’s more regulation coming, but some of it’s quite open regulation that’s actually allowing this industry to continue, but with a lot of oversight. Specifically, regarding Tether, what are the regulations you have to follow? What are the agencies you have to work with?

Stuart: Tether is registered with FinCEN as a money services business. That means the tether has to make reports up to FinCEN, have a compliance program, which I referred to earlier, just in passing, subject to examination by FinCEN, that kind of thing.

Tether also makes reports to the BVI’s financial investigation agency under applicable law there, as most of the corps in the Tether group are BVI companies. So the bottom line is that Tether is regulated. So this notion, you’ll see sometimes that tether is quote “unregulated,” which a big word in some mouths, in my view is just flat wrong. And it’s a little bit irritating, but those are the baseline rules that that Tether has to follow. And our compliance program has been built to match or exceed those standards.

(Tether is not regulated in any meaningful sense. The company is registered in the British Virgin Islands. In fact, the reason it got into hot water with the NYAG, is because it was allegedly doing business in NY without a BitLicense, required for crypto companies to do business in the state, and it violated the Martin Act by misleading customers into believing that tethers were fully backed when in fact, they were not.)

Peter: So what did you make of the OCC letter? Because it was quite interesting, the idea that banks can start issuing stablecoins. I imagine for someone like you guys, that’s quite interesting because could you see a scenario where they’re working directly with Tether?

Stuart: I think it’s premature to say that. I agree that the OCC letter was very interesting. Other people far smarter than I am, have talked about that and opined on it already. And I’ll certainly defer to our U.S. counsel on that. But it’s very interesting and look, we always are interested in working with and cooperating with and teaching and learning from regulators and policy-makers and law enforcement agents around the world, not just in the United States.

That’s another step on that road. I think you’re right. I think increased regulation in this space is coming. I think it’s going to be different, depending on where it is. We don’t take U.S. customers. But we are still registered with FinCEN, so that’s something that we need to pay attention to. And we’ll continue to engage on a worldwide basis with anyone who wants to work with us to help develop their own policies, help develop their own regs and figure out what they can learn from us and what we can learn from them.

(If you are registered with FinCEN but you don’t take U.S. customers, what is the point of being registered with FinCEN?)

In that kind of context. We just think that other people are better qualified to do the last mile and we’re happy to cede the field to them.

Peter: This might be a question for you Paolo, but are there scenarios where Tether can fail, any form of catastrophic failure?

Paolo: I think that the only one that I’m not worried about, but due to my technical nature, I’m working every single day and second of my life to prevent, is ensuring that the private key stays safe. That’s it, right? So what we do is choose the blockchains that we allow tether on in a really careful way. So we choose blockchains that are, first of all, supported by a wide community. We choose blockchains that have a native type of token support, if possible, that has a built-in multisig pattern that we can use and have support for hardware wallets.

So these are basically the key requirements for us to operate safely on a specific blockchain. We do have the capability of freezing accounts on most of the blockchains. That is really important. As Stu said, we save tens of millions of dollars. Part of those were also some of these situations were public when we did that. Recall one exchange hack, for example. So, yeah, basically my life is all about thinking how things can go wrong and try and make sure that we can prevent those from happening.

Peter: Which blockchains are you currently supporting?

Paulo: We support bitcoin two ways, from Omni Layer and Liquid. Then we support EOS, Ethereum, Tron, Algorand. [Speaking to Peter] Don’t do that face please. [Laughs]

Peter: Fucking Tron.

Stuart: On a podcast called What bitcoin did, you’re going to get the grimace, Paolo.

Paolo: Ethereum fees were $16, mate.

Peter: In fairness, you’ve answered all the questions that I wanted to ask you, and these were based on a lot of the questions that were coming out in Twitter, when I put it out there. Most of them are related to, is it fully backed, blah, blah, blah. I personally still think there’s work to be done there. So I’m going to keep pushing you on that.

Stuart, is there anything I’ve not asked that you kind of wish I had?

Stuart: No, I don’t think so, but I do want to just jump back to your comment. I actually agree with you. I think that there is work to be done. I think you should continue to push us and nothing is perfect. We can always do better and we look forward to doing better this year and beyond, but we’re really excited about 2021. And we look forward to being pushed. We look forward to these questions. We look forward to engaging with the community and putting the facts out there on the table.

Peter: How comfortable would you be doing one in the future, give a couple of months and perhaps allow people to submit questions in and take the questions submitted?

Stuart: I would have to talk to our PR folks. But personally, I’m very comfortable with that. I’m fine with that.

Peter: I think we should do that. As I said in the start, and for full transparency, people should know that I’m in a legal situation and Tether has helped support that at some points

But, at no point, does that change the line of questioning. I told you beforehand, I’m only doing this if I can ask any question I want. People should know that. I wanted to do it because whilst people say, Oh, you’re a journalist Pete, you should be completely impartial.

I think this is all FUD. And, I’m finding it really annoying. And I’m finding a consistent pattern and who it’s coming from. And it’s coming from people who’ve had an agenda against bitcoin for a long time. And it’s coming from people who I think are nocoiners and they’re salty.

I haven’t found anyone, I actually respect doing this, so I can be impartial at best with my questions, but I’m not impartial because I believe this is FUD. But I will continue to push you. I’ll continue to ask you questions. And I appreciate you coming on, man. And yeah, hopefully, we’ll do this again in a couple of months and, if that’s okay with you guys, I’ll open up to the floor and see if questions in the community.

*Update Feb. 6: Previously, I said Bitfinex borrowed $700 million of Tether’s money, but it looks like they are now saying it is $750 million. (The NY AG said in April 2019 that Bitfinex had taken “at least $700 million.”)

Update Jan. 12: An earlier version of this story stated that Tether had minted 20 billion tethers this year alone. That’s incorrect—it’s 20 billion since March 2020.

Related stories:

Nocoiner predictions: 2021 will be a year of comedy gold

Are pixie fairies behind Bitcoin’s latest bubble?

The curious case of Tether: a complete timeline of events

If you like my work, please consider supporting my writing by subscribing to my Patreon account for as little as $5 a month.

Basically, that equates to, you could get shares of iFinex (Bitfinex and Tether’s parent company) or LEO tokens (a new token Bitfinex recently created) or whatever is in the soup bowl that day. And you may end up with something that has as much real world value as horse manure—just not as good for the roses.

Basically, that equates to, you could get shares of iFinex (Bitfinex and Tether’s parent company) or LEO tokens (a new token Bitfinex recently created) or whatever is in the soup bowl that day. And you may end up with something that has as much real world value as horse manure—just not as good for the roses.

It’s still not clear where all that money went. Bitfinex says the funds were “

It’s still not clear where all that money went. Bitfinex says the funds were “

{kind=link}