Help our work: if you liked this post, please tell just one other person. It really helps!

You can also send money to our one-way ETFs! Here’s Amy’s Patreon and here’s David’s. For casual tips, here’s Amy’s Ko-Fi and here’s David’s.

Boy, those ETFs were the juice bitcoin really needed, eh?

The SEC approved 11 bitcoin spot ETFs on Wednesday, January 10, with media widely reporting what a boon this would be for the coiners. Surely this would lure piles of fresh dollars into bitcoin!

Not quite. The bitcoin price held around $46,000 — but just for long enough for the whales to start cashing out.

What the crypto world needs to understand is that bitcoin ETFs are not bitcoins. They’re a traditional finance product with bitcoin flavoring.

Except for the risk — that bit is completely bitcoin.

Number go down

The first big post-ETF price drop came on Friday, January 12. Bitcoin slipped from $46,000 to $43,500 in two hours — only one hour after the day’s printing of a billion tethers was released. A few hours after that, another dump took the price from $43,500 to $41,000.

The bitcoin market is fake and in tethers. The retail securities market is real and in actual dollars. You can’t pump bitcoin ETFs with tethers.

After years of being severely discounted from the price of the bitcoins in the fund, Grayscale GBTC finally reached net asset value. This turned out to be not so great — it looks like long-frustrated GBTC holders are finally dumping now that they can. [CoinDesk; Bloomberg, archive]

Coinbase (Nasdaq: COIN) stock went down as well. It was up as high as $186 at the end of December. It dropped to $130.78 on January 12.

ETFs have put bitcoin on steroids! Asthmatic and with shrunken balls.

Bitcoins: not so great

Bitcoins are still an awful investment for ordinary people who aren’t true believers in Satoshi and just want to grow their dollars.

The ETF S-1 filings go into considerable detail on the risks — none of which should be news to anyone here.

The main risk the ETF trusts see is that the base asset is still a completely terrible investment. Crypto is insanely volatile. A pile of crypto companies went broke from being run by crooks — the filings go into some detail on this. Everyone hates bitcoin miners. The regulators, from the White House down, increasingly just despise everything about crypto. And very few people like bitcoin anyway.

Securities broker Vanguard thinks the bitcoin ETFs are such trash that they’re not only not offering these spot bitcoin ETFs — they’re withdrawing the crypto futures ETFs they presently offer. [Axios]

What happens if the ETF bitcoins are stolen?

Unlike a bitcoin futures ETF, a spot ETF is based on actual bitcoins — and these have to be stored somewhere.

Most of it, including $29 billion face value of GBTC bitcoin, is stored by Coinbase Custody. VanEck is storing their ETF coins at Gemini. Fidelity is storing their ETF coins at their own custody subsidiary.

So what happens if a hacker gets into the digital fortress and takes all the bitcoins?

In short: too bad. Sorry, your money is gone!

Coinbase Custody advised BlackRock that it has insurance covering up to $320 million losses of custodied crypto — but that’s for all its customers’ $144 billion (face value) of cryptos in custody. That’s a whole 0.2% coverage. [SEC]

The ETF trusts themselves do not have FDIC or Securities Investor Protection Corporation (SIPC) insurance.

The ETF trusts specifically disclaim liability for lost backing assets. Valkyrie, for example, says: “Shareholders’ recourse against the Trust, Trustee, Custodian and Sponsor under New York law governing their custody operations is limited.” [SEC]

Investors would likely sue anyway. BlackRock and Fidelity could cover such a loss, though it would sting. Grayscale would be utterly unable to cover it.

If Coinbase were to go bankrupt, it’s not clear legally if crypto stored in Coinbase Custody would belong to the individual customers or would be thrown into the bankruptcy estate!

The custodian just losing all the bitcoins is not a trivial risk — two crypto custodians, Prime Trust and Fortress, went bankrupt in 2023 just from losing customer coins.

We spoke to Frank Paiano, who teaches finance and investing at Southwestern Community College, about what would happen if a bitcoin ETF’s backing assets vanished. [Frank Paiano]

He thinks that customers “will be fooled into thinking” that the ETF assets are protected, even though they absolutely are not. “That is mostly why Fidelity has set up their own trustee. I would guess that companies such as BlackRock would do the same.” (BlackRock is so far just using Coinbase.)

Loss of ETF-backing assets happens quite a lot, said Paiano. “A simple Internet search for ‘gold investments stolen’ yields several examples. Then there are the age-old anecdotes of people being duped into buying lead painted or plated with gold.”

Paiano thinks bitcoin ETFs are profoundly unwise investments: “prudent, long-term oriented investors should stay far away from these abominations”— but they’ll find customers.

“If there are foolish, greedy individuals willing to part with their hard-earned money, there will be scoundrels happy to oblige them.”

Other bitcoin ETF fallout

The day before the SEC announced its approval of 11 spot bitcoin ETFs, the official @SECGov Twitter posted a fake notice saying a bitcoin ETF was approved. SEC Chair Gary Gensler issued a statement on the fake tweet, saying that an unauthorized party got hold of the phone number connected to the account but didn’t get access to any SEC internal systems. [SEC]

What happens next?

The new narrative we’ve seen is that the real bitcoin pump is in 90 days when financial advisors are finally ready to push bitcoin ETFs on their customers, for some reason. Probably the halvening, or sunspots maybe.

We don’t expect the number to go up just from bitcoin ETFs existing — anyone who wanted bitcoins could already buy them, and “anyone” numbers one-eighth of what it did in the recent bubble.

We do expect downward pressure on the bitcoin price to continue from the GBTC holders who can finally cash out near par.

Tether pumps only work if nobody tries to cash out into the pumped-up price. Unfortunately, that only works as long as nobody wants real dollars. It turns out they do.

With these ETFs, bitcoin is the dog that caught the parked car.

Media stardom

David was quoted by Cointelegraph on bitcoin ETFs. A bitcoin ETF is a terrible idea, but we don’t think the threat model includes the issuers stealing the bitcoins. [Cointelegraph; Cointelegraph; Cointelegraph]

David spoke to Davar about bitcoin ETFs and our friends at Tether. (“Basket fund” is the local term for “ETF.”) [Davar, in Hebrew, Google translate]

David went on Logan Moody’s podcast The Contrarian just before the ETFs were approved to talk about the state of crypto as of early 2024. [YouTube]

As predicted, the SEC today approved several spot bitcoin ETFs — Grayscale GBTC, Bitwise, Hashdex, BlackRock iShares, Valkyrie, ARK 21Shares, Invesco Galaxy, VanEck, WisdomTree, Fidelity Wise Origin, and Franklin.

Fees are cut throat, some less than a quarter of a percent. These companies can run the ETFs as loss leaders for a while, but eventually they’ll have to raise the fees or quit.

Today’s post is over on David’s blog. [DavidGerard]

The SEC really doesn’t want to approve a bitcoin ETF — but we think it may be forced to. So it’s gonna make them compliant, which means they’ll suck a lot more for crypto’s purposes.

Image: Gary Gensler with Zeke Faux’s Number Go Up.

Send us money! Here’s Amy’s Patreon, and here’s David’s. Sign up today!

If you like this article, please forward it to just one other person. Thank you!

The New York Attorney General is suing crypto investment fund Genesis, its parent company Digital Currency Group (DCG), and the Gemini crypto exchange for defrauding customers of Gemini’s Earn investment product. [Press release; complaint, PDF]

Earn put investors’ money into Genesis — where it evaporated.

The lawsuit also charges former Genesis CEO Soichiro (a.k.a. Michael) Moro and DCG founder and CEO Barry Silbert for trying to conceal $1.1 billion in crypto losses with an incredibly dubious promissory note.

New York is asking the court to stop all three companies’ business in “securities or commodities” in the state. That’s all but a death sentence — bitcoin is a commodity in the US.

The NYAG says that Genesis and Gemini defrauded more than 230,000 Earn investors of more than $1 billion total, including at least 29,000 New Yorkers. New York says that thousands more lost money because of DCG’s actions.

The NYAG claims that:

Genesis and Gemini lied to investors about Earn and Genesis’ credit-worthiness;

Genesis lied to Gemini that it was solvent;

DCG and Gemini lied to the public, including investors, about the promissory note;

Earn is an unregistered security under New York’s Martin Act.

This is a complaint we recommend you read. We all knew some of what went on between Genesis, DCG, and Gemini, but this suit goes into great detail about what happened behind the scenes.

This is a civil complaint, not a criminal indictment — but the NYAG describes several crimes being committed, particularly by DCG, Genesis, Moro, and Silbert.

How Earn worked

Gemini, owned by Tyler and Cameron Winklevoss, and Genesis Capital, a subsidiary of DCG, partnered to launch the Gemini Earn program in February 2021 — just as bitcoin’s number was going up really fast. Crypto was a hot product!

Gemini and Genesis marketed Earn to the public as a “high-yield investment program” — which is just coincidentally a common marketing term used by Ponzi schemes.

Earn promised to pay up to 8% yield. Ordinary investors could deposit their crypto via the Gemini exchange. You could get your money back anytime!

Earn was a pass-through fund to Genesis. Retailers put their crypto in Earn. Gemini then handed the funds off to Genesis, who then lent the money to institutional investors, notably crypto hedge fund 3AC in Singapore. Genesis was substantially a 3AC feeder fund — of which there were many.

When Earn investors wanted to withdraw their funds, Genesis had five days to return the principal and the interest, minus Gemini’s agent fee.

Gemini earned more than $22 million in agent fees for running Earn, plus more than $10 million in commissions when investors bought crypto on Gemini to put into Earn.

Paper thin

3AC was Genesis’ second largest borrower. 3AC had borrowed $1 billion of crypto at 8% to 15% interest, secured by $500 million of illiquid crypto tokens.

Genesis hadn’t received audited financial statements from 3AC since July 2020. But with interest rates like that, why worry — it’ll be fine, right?

It wasn’t fine. 3AC fell over on June 13, 2022, losing Genesis $1 billion. Babel Finance, another Genesis borrower, fell over on June 17, losing Genesis another $100 million — because in June 2022, everyone was falling over.

Genesis was $1.1 billion in the red — it didn’t have the funds to pay back Earn investors. Between mid-June and July 2022, Silbert and other DCG officers met with Genesis management to work out how to fill the hole in Genesis’ balance sheets — and what to tell counterparties such as Gemini.

One problem was that some of the collateral for 3AC’s loan was GBTC shares, issued by another DCG subsidiary, Grayscale — which Genesis couldn’t sell, due to restrictions on sales of stock by “affiliates” of the issuing company.

Silbert told the board of DCG that Genesis was anticipating a run on the bank if word got out. So DCG began casting about for financing. Silbert also suggested to the DCG board on June 14, 2022, that they “jettison” Genesis.

But DCG and Genesis decided instead to act like everything was fine. On June 15, Genesis told everyone its “business is operating normally.” Two days later, Genesis CEO Michael Moro posted in a tweet reviewed and edited by DCG: “We have shed the risk and moved on.” [Twitter, archive; Twitter, archive]

Everything was not fine. The 3AC hole meant that Genesis’ loss exceeded its total equity, and Genesis couldn’t pay out Earn investors. Genesis hadn’t “shed the risk and moved on” — it still had the gaping hole in its balance sheet. It was not “operating normally” — it was floundering in a panic.

Genesis was unable to find anyone to lend them the money they needed, so they had to find a way to paper the hole before the end of the quarter.

The solution: DCG would make a loan from its right pocket to its left pocket and count the loan as an asset.

So on June 30 — the last day of Q2 2022 — DCG gave its wholly-owned subsidiary Genesis a promissory note for $1.1 billion. DCG would pay it back in ten years at 1% interest.

Both Silbert and Moro signed off on the IOU. The note was, of course, not secured by anything.

DCG never sent Genesis a penny — the note was only ever meant to be a $1.1 billion accounting entry so that Genesis and DCG could tell the world that Genesis was “well-capitalized” and that DCG had “absorbed the losses” and “assumed certain liabilities of Genesis.”

None of this was true. DCG wasn’t obligated to pay anything on the note for 10 years. And Genesis was still out $1.1 billion of actual funds.

Michael Patchen, Genesis’ newly appointed chief risk officer, said in internal documents that the promissory note “wreaks havoc on our balance sheet impacting everything we do.”

Genesis directed staff not to disclose the promissory note to Genesis’ creditors, such as Gemini. Many Genesis staff didn’t even know about the promissory note until months later.

DCG’s piggy bank

DCG made Genesis’ problems even worse by treating Genesis like its own personal piggy bank.

In early 2022, DCG “borrowed” more than $800 million from Genesis in four separate loans. When $100 million of this came due in July, DCG forced Genesis to extend the maturity date — and DCG still hasn’t paid a penny of it to date.

A DCG executive told a Genesis managing director on July 25, 2022, that DCG “literally [did not] have the money right now” to repay the loan. Genesis had no choice — the managing director replied: “it sounds like we don’t have much room to push back, so we will do what DCG needs us to do.” DCG also dictated the interest rate for this loan.

Around June 18, 2022, DCG borrowed 18,697 BTC (worth $355 million at the time) from Genesis. It partially paid this back on November 10, 2022 — with $250 million worth of GBTC! — but this still left Genesis with no cash to pay back its own creditors. And it still couldn’t liquidate the GBTC.

It’s hard to consider the deals between Genesis, DCG, and Grayscale as anything like arm’s length — it was a single conglomerate’s internal paper-shuffling.

On November 2, CoinDesk reported that FTX, one of the largest crypto exchanges, was inflating its balance sheet with worthless FTT tokens. The report brought FTX tumbling down, and FTX filed for bankruptcy on November 11, 2022.

Around November 12, 2022, Genesis sought an emergency loan of $750 million to $1 billion from a third party due to a “liquidity crunch.” Its efforts were unsuccessful. On November 16, Genesis halted redemptions.

If you owe Gemini a billion dollars, then Gemini has a problem

Gemini Earn investors were supposed to be able to get their funds back at any time. This meant that those funds had to be highly liquid. Gemini told investors it was monitoring the financial situation at Genesis.

Gemini absolutely failed to do this. They lied to investors, and they hid material information.

Gemini got regular financial reports from Genesis. Gemini’s internal risk analyses showed that Genesis’ loan book was undercollateralized for Earn’s entire operating existence. But Gemini told Earn customers that Genesis had more than enough money to cover their loans.

Starting in 2021, Genesis’ financial situation went from bad to worse. In February 2022, after analyzing Genesis’ Q3 2021 financials, Gemini internally rated Genesis capital as CCC-grade — speculative junk — with a high chance of default.

Gemini also found out that Genesis had a massive loan to Alameda — secured by FTT tokens! The same illiquid FTX internal supermarket loyalty card points that were discovered by Ian Allison at CoinDesk to make up about one-third of Alameda’s alleged reserves.

Even after Genesis recalled $2 billion in loans from Alameda, the crypto lender was still full of loans to affiliates, including its own parent company DCG.

In June 2022, the crypto markets crashed and burned. But Gemini continued to reassure investors that it was safe to feed money to Genesis via Earn.

This was apparently fine when it came to someone else’s money, but according to the complaint:

During this same period, Gemini risk management personnel withdrew their own investments from Earn. A Gemini Senior Risk Associate working on Earn withdrew his entire remaining Earn investment — totaling over $4,000 — between June 26, 2022, and September 5, 2022.

Likewise, Gemini’s Chief Operations Officer [Noah Perlman], who also sat on Gemini’s Enterprise Risk Management Committee, withdrew his entire remaining Earn investment — totaling more than $100,000 — on June 16 and June 17, 2022.

This was when DCG tried to paper over the hole in Genesis’ balance sheet with a $1.1 billion IOU.

Gemini realized things weren’t good at Genesis, but it’s not clear that they realized how bad they were — not helped by Genesis lying to Gemini about their true condition.

From June to November 2022, Genesis would send Gemini false statements on their financial condition — for instance, saying that the DCG promissory note could be converted to actual cash within a year, when in fact, it was a 10-year note.

Gemini didn’t tell investors that Genesis was in trouble. Instead, they thought they’d “educate clients on the potential losses” and “properly set clients’ expectations.”

When the Gemini board was advised of Genesis’ financial state in July 2022, one board member compared Genesis debt-to-equity ratio to Lehman Brothers before it collapsed.

Gemini tried and failed to extricate itself from Genesis. They just could not get the funds back. But they knew that Genesis operated as a closely controlled sockpuppet of DCG, and they wanted Silbert to make good on Genesis’ debt.

As things at Genesis got worse, Gemini worked out how to break the news to Earn creditors.

On September 2, 2022, Gemini finally decided to terminate Earn. On October 13, Genesis formally terminated the Earn agreements and demanded the return of all investor funds.

On October 20, 2022, Silbert met with Cameron Winklevoss of Gemini. Silbert said that Gemini was Genesis’ largest and most important source of capital — meaning that Genesis could not redeem Earn investors’ funds without Genesis declaring bankruptcy.

Gemini quietly granted Genesis multiple extensions to return investor funds.

On October 28, 2022, Silbert finally let Genesis tell Gemini the true terms of the promissory note — just two weeks before Gemini cut off withdrawals.

For some reason neither we nor the NYAG can fathom, Gemini cointinued to take investors’ money and put it into Earn right up to the end!

Customer service

Gemini didn’t do anything so upsetting for Earn investors as to tell them about Genesis’ unfortunate condition — even as Gemini’s own staff closed out their positions in Earn.

One customer wrote to Gemini on June 16, 2022, three days after 3AC collapsed, asking if any of their funds were with 3AC. Gemini didn’t answer the question, but replied with vague reassurances about Genesis’ trustworthiness.

Another wrote on June 27, 2022: “with other exchanges like Celsius and Blockfi I am concerned about Gemini. Does Gemini have any similar vulnerabilities? … liquidity vulnerabilities? … risky investments/loans that would risk my assets or cause Gemini to halt withdrawals?”

Gemini responded: “Gemini is partnering with accredited third party borrowers including Genesis, who are vetted through a risk management framework which reviews our partners’ collateralization management process.”

This investor was sufficiently reassured to send in another $1,000.

A third customer wrote on July 24, 2022, asking specifically if Gemini was involved in any of the “drama” around 3AC and if it impacted Earn. Gemini said they weren’t involved in anything regarding 3AC — even as the 3AC crash had in fact blown out Earn.

The consequences

The NYAG is asking the court that all three companies be permanently banned from dealing in “securities or commodities” in New York — e.g., bitcoin.

Some of the press coverage noted this provision — but didn’t notice that it would be a near death sentence for a crypto business. DCG’s profitable Grayscale business would have to leave New York or be sold off. Gemini would be kicked out of the state.

New York is also seeking restitution for the victims and disgorgement of ill-gotten gains.

Also, they all get fined $2,000 each. It’s possible that bit of the General Business Law could do with an update.

We’ve just come out with another crypto crash update — this one is on David’s blog, so head on over there and read it!

Before you read, please take a moment to subscribe to our Patreons — mine is here and David’s is here. Your support is important. The news is free, but we depend on donations.

In this latest update, we talk about:

How bankruptcy works and how administrative costs suck up hundreds of millions of dollars before creditors see a penny.

How the collapse of UST has hit the crypto market worldwide.

Legal ramifications for 3AC founders if they don’t play ball.

How 3AC benefited from the GBTC arbitrage opportunity — and how Grayscale and Genesis may have helped!

Why Tether may be required to return $840 million in assets to Celsius.

The FDIC and the Feds cease and desist statement to Voyager.

Be sure to subscribe to our Patreon accounts — Amy’s is here; David’s is here.

We often get asked by reporters: “Why are crypto markets crashing?” The short answer is because there’s no money left, and no more coming in. The long answer is more complicated.

Bitcoin peaked at $64,000 in April 2021 and again at $69,000 in November 2021. Many of the network effects that drove the price of bitcoin to those heights were put into place in 2020.

The same network effects are now working in reverse. Markets take the stairway up and the elevator down.

The 2017 bubble was fueled by the ICO boom and actual outside dollars entering the crypto economy. Bitcoin topped out just below $20,000 in December 2017.

The crash that followed over the next 12 months was like air being slowly let out of a balloon — much like the 2014 deflation after Bitcoin’s prior 2013 peak. ICO and enterprise blockchain promoters tried to keep going through 2018 like everything was fine, but the party was clearly over.

In contrast, the 2022 crash is like a wave of explosive dominoes all crashing down in rapid succession. How did we get here?

A long, cold crypto winter

Let’s start in early 2020. It was the crypto winter. Bitcoin’s price had spent two years bobbling up and down from infusions of tethers, and traders on BitMEX rigging the price to burn margin traders. (And, allegedly, BitMEX itself burning its margin traders.) [Medium, 2018]

But the dizzying price rises were peculiarly bloodless. There was little evidence of fresh outside dollars from retail investors — the ordinary people. The press would write how bitcoin had just hit $13,000 — but they’d also call people like us, and we’d tell them about Tether.

Throughout 2019 and into 2020, crypto pumpers were desperately trying scheme after scheme — initial coin offerings, initial exchange offerings, bitcoin futures, selling to pension funds — to lure in precious actual dollars and get the party re-started.

Then Corona-chan knocked on the door.

Act I, Scene I: Pandemic Panic

On March 13, 2020, the US government declared a pandemic emergency. The panic drove down stocks and crypto. Investors sold everything and flew to the safest, hardest form of money they could find: the US dollar! Bitcoin dropped from $7,250 to $3,858 over the course of that day.

It was an edge-of-the-cliff moment for bitcoin. Any further drop could force liquidations and create a ripple effect across dozens more crypto projects. For bitcoin miners, the price of bitcoin was now below the cost of mining.

Worse, only two months away was the bitcoin “halvening” — an every-four-year event when the number of bitcoins granted in each freshly-mined block halves. If bitcoin dropped too low in price, the miners wouldn’t be able to pay their enormous power bills. The crypto industry desperately needed to push bitcoin’s price back before May.

Tether spins up the printing press

Tether, launched in 2014, is an offshore crypto company that issues a dubiously backed stablecoin of the same name. Tether works like an I.O.U. — Tether supposedly takes in dollars and issues a tether for each dollar held in reserve. Since Tether has never had an audit, nobody knows for sure what’s backing tethers. The company has an extensive history of shenanigans — see Amy’s Tether timeline.

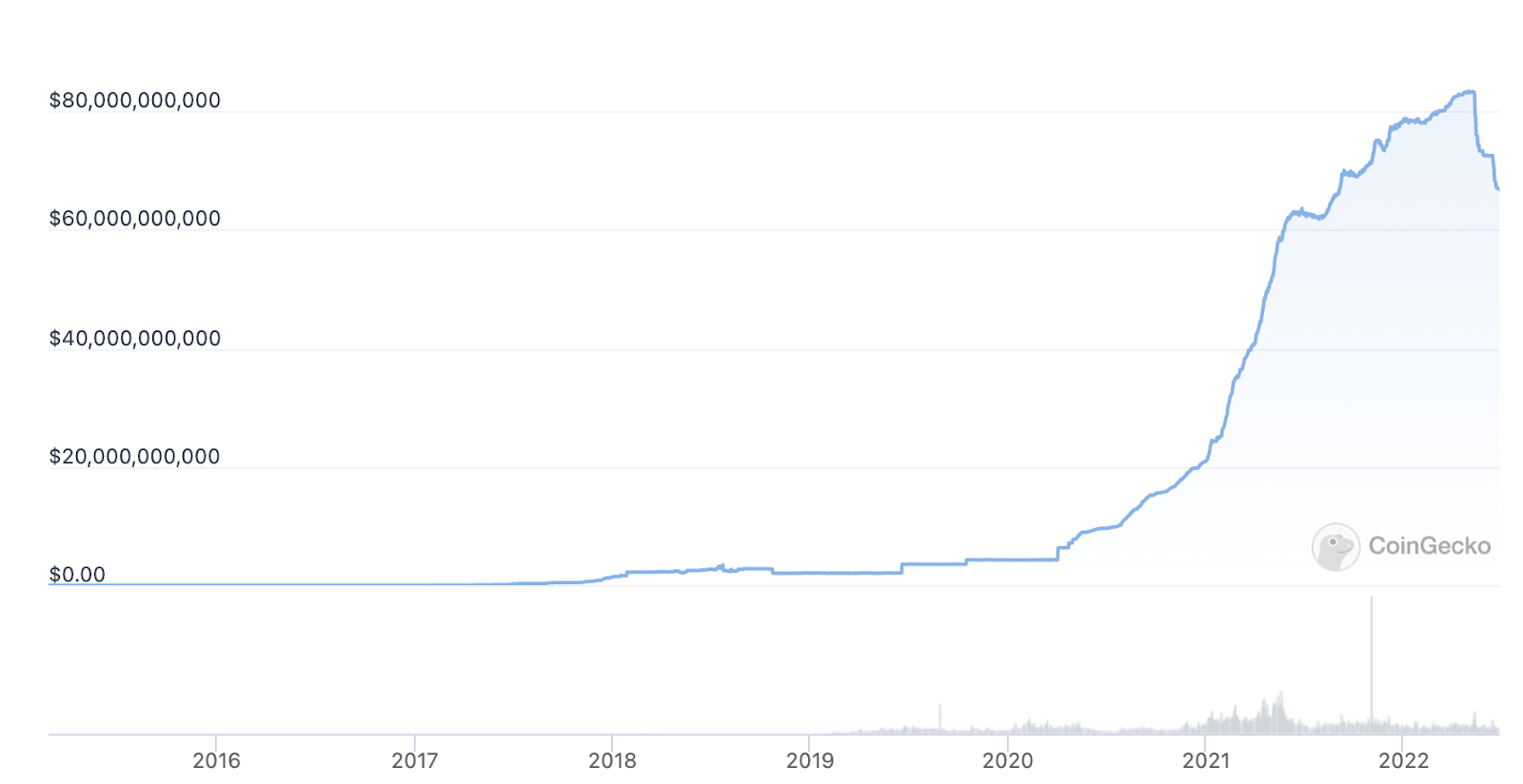

The issuance of tethers in March 2020, was 4.3 billion, but that’s when the Tether printer kicked into overdrive — minting tethers at a clip nobody had ever seen before.

Tether minted 4.4 billion tethers in April 2020 — crypto’s version of an economic stimulus package. By May, Bitcoin reached $10,000, just in time for the halvening.

Once the price of bitcoin goes up, though, there’s no way to turn off the Tether printing press. It has to keep printing. If the price of bitcoin goes down, people will sell, creating an exodus of real dollars from the system. So Tether kept printing, pushing the price of bitcoin ever skyward.

In May, June, and July 2020, Tether issued a combined total of 3 billion tethers. In August, when the price of bitcoin reached $12,000, Tether issued another 2.6 billion tethers. In September, when bitcoin slid below $10,000, Tether issued another 2.2 billion tethers.

By the end of 2020, Tether had reached a market cap of 21 billion. The printer kept going. In 2021, Tether pumped out 60 billion more tethers. By May 2022, Tether’s market cap had reached 83 billion. Bitcoin’s price peaks in April 2021 ($64,000) and November 2021 ($69,000) both coincided with an influx of tethers into the market.

You can’t just redeem tethers. Only Tether’s big customers — it has about ten of them — can redeem. You can try to sell your tethers on an exchange. But you can’t just go up to Tether to redeem them for dollars. There were no redemptions of tethers, ever, until May and June 2022 — the present crash.

This suggests that the rest of the reserve over that time was made up of whatever worthless nonsense Tether could claim was a reserve asset — loans of tethers, cryptocurrencies, and dubious commercial paper credited at face value rather than being marked to market.

Dan Davies, in his essential book Lying for Money, marks this as the key flaw in frauds of all sorts: they have to keep growing so that later fraud will keep covering for earlier fraud. This works until the fraud explodes.

Tether marketcap, CoinGecko

GBTC’s ‘reflexive Ponzi’

Grayscale’s Bitcoin Trust (GBTC) played a huge role in keeping the price of bitcoin above water through 2020. It offered a lucrative arbitrage trade, an exploitable inefficiency in markets, that a lot of big players went all-in on.

GBTC was an attempt to wrap Bitcoin in an institutionally compatible shell. All through 2020 and into 2021, GBTC was trading at a premium to bitcoin on the secondary markets. Accredited investors would acquire GBTC at net asset value — some large proportion being in exchange for direct deposits of bitcoins, not purchases for cash, although all the accounting was stated in dollars. After a six-month lock-up, the accredited investors would sell the shares to the public at a 20 percent premium, sometimes more. Rinse, repeat, and that’s a 40 percent return in a year.

GBTC functioned like a “reflexive Ponzi.” When Grayscale bought more bitcoin for the trust, that drove up the price of bitcoin, which pushed up the GBTC premium, which resulted in investors wanting more GBTC and Grayscale issuing more shares.

Grayscale ran a national TV advertising campaign at the time, targeted at ordinary investors. The ads warned that disaster was imminent, inflation would eat your retirement, and bitcoin was better than gold — so you should buy bitcoin. Or, this shiny GBTC, which was implied to be just as good! [YouTube, 2019]

In a bull market, retail investors didn’t mind paying a premium — because the price of bitcoin kept going up. The market treated GBTC as if it was convertible back to bitcoins, even though it absolutely wasn’t. [Adventures in Capitalism]

Grayscale ultimately flooded the market with GBTC. When an actual bitcoin ETF became available in Canada, GBTC’s premium dried up. Since February 2021, GBTC has been trading below the price of bitcoin. As of March 2022, the trust holds 641,637 bitcoins. And they’re staying there indefinitely — leaving GBTC holders locked in on an underwater trade.

The rise of decentralized finance

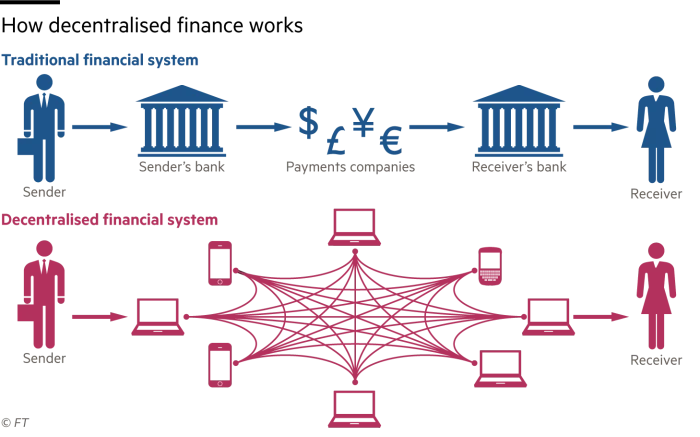

Decentralized finance, or DeFi, didn’t directly pump the price of bitcoin in 2020. But DeFi was one of the stars of the 2021 bubble itself, and eventually caused the bubble’s disastrous explosion. All of the structures to let that happen were set up through 2020.

DeFi is an attempt to put traditional financial system transactions — loans, deposits, margin trading — on the blockchain. Regulated institutions are replaced with unknown and unregulated intermediaries, and everything is facilitated with smart contracts — small computer programs running on the blockchain — and stablecoins.

All through 2019 and 2020, DeFi was heavily promoted as offering remarkable interest rates. At a time of low inflation, this got coverage in the mainstream financial press. Here’s the diagram the Financial Times ran, depicting DeFi as a laundromat for money: [FT, paywalled, archive]

The key to DeFi is decentralized exchanges, where you can trade any crypto asset that can be represented as an ERC-20 token — such as almost any ICO token — with any other ERC-20 token.

DeFi also lets you take illiquid tokens that nobody wants, do a trade, assign them a spurious price tag in dollars, then say they’re “worth” that much. This lets dead altcoins with no prospective buyers claim a price and a market cap, and attract attention they don’t warrant. If you put a dollar sign on things, then people take that price tag seriously — even when they shouldn’t.

You can also create a price for a token that you made up out of thin air yesterday and use DeFi to claim an instant millions-of-dollars market cap for it.

This was the entire basis for the valuation of Terraform Labs’ UST and luna tokens — and people believed those “$18 billion” in UST were trustworthily backed by anything.

You can also use those tokens you created out of thin air as collateral for loans to acquire yet more assets. An unconstrained supply of financial assets means more opportunities for bubbles to grow, and more illiquid assets that you can dump for liquid assets (BTC, ETH, USDC) when things go wonky.

By September 2020, five hundred new DeFi tokens had been created in the previous month. DeFi hadn’t hit the mainstream yet — but it was already the hottest market in crypto. [Bloomberg]

The problem was that in 2020, to use DeFi you had to know your way around using the actual blockchain. Retail investors, and even most institutional investors, haven’t got the time for that sort of dysfunctional nonsense.

Retail was more attracted to the “CeFi” (centralized DeFi) investment firms, such as Celsius and 3AC, offering impossible interest rates. These existed in 2020 but didn’t gain popularity until the following year when the bubble had started properly.

A new grift: NFTs

By late 2020, crypto promoters were searching for a new grift to lure in retail money, one that would have broader mainstream appeal. They soon found one.

NFTs as we know them got started in 2017, with CurioCards, CryptoPunks, and CryptoKitties. NFT marketing had continued through the crypto winter — in the desperate hope that ordinary people might put their dollars into crypto collectibles.

The foundations of the early 2021 burst of art NFTs were laid in late 2020, when Vignesh Sundaresan, a.k.a. Metakovan, first started looking into promoting digital artists, such as Beeple — whose $69 million JPEG made international headlines for NFTs in March 2021, and officially kicked off the NFT boom.

Late 2020 also saw the launch of NBA Top Shot, the only crypto collectible that ever got any interest from buyers other than crypto speculators. Top Shot traders were disappointed at how incredibly slow Dapper Labs was at letting them withdraw the money they’d made in trading — and became some of the first investors in the Bored Apes.

Coiner CEOs

By late 2020, several big company CEOs started promoting the concept of bitcoin on the company dime. These included Jack Dorsey at Twitter, Dan Schulman at PayPal, and Michael Saylor at business software company MicroStrategy.

In October 2020, Saylor revealed his company had bought 17,732 bitcoins for an average of $10,000 per coin. Over the next 18 months, Microstrategy would plow through its cash reserves and take on debt to funnel more money into bitcoin, spending $4 billion in the process. Buying MSTR shares become the newest way for retail investors to bet on bitcoin. Saylor also put himself forward as bitcoin’s latest prophet and crazy god.

PayPal set up bitcoin trading in 2020, though only as a walled garden, where you couldn’t move coins in or out. Still, it made gambling on crypto more accessible to retail investors.

Bitcoin miners start ‘hodling‘

By late 2020, we suspect there was very little actual cash in crypto. But bitcoin needed to continue its upward ascent.

The biggest tip-off that the fresh outside dollars had stopped flowing was when bitcoin miners stopped selling their coins. Bitcoin miners mint 900 new bitcoins per day. They typically sell these to pay their energy costs — power companies don’t accept tether — and buy new mining equipment, which becomes obsolete every 18 months. At $20,000 per bitcoin, that would equate to $18 million, in actual dollars, getting pulled out of the bitcoin ecosystem every day.

In October 2020, Marathon Digital (MARA), one of the largest publicly traded miners, stopped selling its bitcoins. They took out loans, which allowed them to buy their equipment and hold their bitcoins. Marathon even bought additional bitcoins!

Borrowing against mined bitcoins, and not selling them, reduced selling pressure on bitcoin’s price in dollars. US-based miners used this model heavily from July 2021 onward — taking low-interest loans from their crypto buddies, Galaxy Digital, DCG, and Silvergate Bank. Although, in 2022, the loans started running out and they had to start selling bitcoins.

This also set Marathon up for potential implosion when energy prices went up and the price of bitcoin dropped in 2022. Marathon is presently losing $10,000 on every bitcoin they mine.

Easy money?

2020 was a weird year of market panics, bored day traders, and easy money — for some.

The Federal Reserve dealt with the pandemic panic by showering the markets with stimulus money. At the retail end, $817 billion was distributed in stimulus checks (Economic Impact Payments), $678 billion in extended unemployment, and $1.7 trillion to businesses, mostly as quickly-forgiven loans. [New York Times]

Bored day traders, stuck at home working their email jobs and unable to go out in the evening, got into trading stocks on Robinhood as the hot new mobile phone game. Car rental firm Hertz, a literally bankrupt company, whose stock was notionally worth zero, started going up just because Robinhood users thought it was a good deal. Instead of crypto becoming a more regular investment like stocks, the stonks* had turned into shitcoins.**

What isn’t clear is how much of this money found its way to the crypto market. At least some of it did. A study by the Federal Reserve Bank of Cleveland noted: “a significant increase in Bitcoin buy trades for the modal EIP amount of $1,200.” This increased BTC-USD trade volume by 3.8%! [Cleveland Fed]

But the trades only seemed to raise the price of bitcoin by 0.07%. And the dollars in question were only 0.02% of the money distributed in the EIP program.

* A cheap and nasty equity stock; the term comes from a meme image. [Know Your Meme] ** We are sorry to tell you that this is literally a technical term in crypto trading.

The final push over the line

A lot of channels into crypto were put into place in 2020. But the last step was to pump the price over the previous bubble peak of $20,000.

With that bitcoin number achieved, the press would cover the number going up — because “number go up” is the most interesting possible story in finance. That would lure in the precious retail dollars that hodlers needed to cash out.

The push started in late November, with deployments of tethers to the offshore exchanges. On December 18, 2020 — exactly three years after the previous high — bitcoin went over $20,000 again. And that’s when a year and a half of fun started.

Bitcoin broke below $20,000 last night. I got a message on Signal while I was sleeping.

On June 18, 2022, at 6:51 UTC, the price of bitcoin fell from $20,377 to $19,245 on Kraken and then slipped to as low as $18,728 before catching its breath. As I write, it is now $19,174.

Bitcoin has now fallen below the previous all-time high it set on December 17, 2017 — officially marking the end of the crypto bubble. The party is over.

Two years ago, as bitcoin embarked on its incredible journey to $69,000 — a number it reached on November 9, 2021 — it was $10,000. At the start of 2020, bitcoin was trading even lower, at around $7,000.

Those numbers give you a sense of how much further bitcoin can fall. As dramatic as the run-up was to $69,000 when every bitcoin bro imagined bitcoin would shoot to the moon, the fall can be equally so, and that is what we are seeing now.

Of course, everyone is asking, why did bitcoin plunge so quickly Saturday night? What pushed it below $20,000 so suddenly? Somebody is selling. Who needs to sell?

Miners have to sell to pay their power bills. They mine 900 newly minted bitcoin per day. The bitcoin network consumes a country’s worth of energy.

The miners have been borrowing money from their buddies, DCG and Galaxy, to cover business costs rather than selling since July 2021. But they can’t borrow any more dollars, so they’re dumping their coins. They also have to pay their credit bills when those loans come due.

Who else is selling? Any number of crypto lenders, yield farms, and other decentralized finance firms that are running desperately low on liquidity — and there are many of them.

Last month, Terra/Luna toppled over. This was DeFi’s Bear Stearns moment. Things seemed to settle down for a moment, but behind the scenes, a titanic shift had begun — the wrecking ball was in action. In the chain of reactions that followed, two other Ponzi schemes collapsed: Celsius and 3AC. Smaller outfits Finblox and Babel soon followed — and more are to come.

When investigators look back and piece together the causes of the crypto apocalypse of 2022, key factors will be huge VC money pouring into the space, the massive printing of Tethers — from 4 billion at the start of 2020 all the way to 83 billion earlier this year — and Grayscale’s Bitcoin Trust.

GBTC was an attempt to wrap Bitcoin in an institutionally compatible shell. As I wrote in “Welcome to Grayscale’s Hotel California,” GBTC’s arbitrage trade brought billions of dollars of real money into the crypto ecosystem.

It also caused explosive growth in crypto leverage. Many of the firms that are collapsing now, looked to GBTC as a way to deliver ridiculously high returns. They would exchange their cash or bitcoin for shares of GBTC and after a 6-12 month lockup, sell those shares on the secondary market for a premium to retail investors. That premium averaged around 18% in 2020.

It was a sure-fire way to make money until the premium dried up. GBTC has been trading below the price of bitcoin since February 2021.

All through 2020 and into 2021, there was a massive retail inflow of cash chasing a “reflexive Ponzi” in the form of a GBTC arb situation. And all Ponzi schemes end the same way — they crash stupendously.

If you like this post, consider subscribing to my Patreon account. You can support my writing for the cost of a cup of coffee per month — or more, if you are feeling generous!

Since November 2021, when Bitcoin hit its all-time high of $69,000, the original cryptocurrency has lost 70 percent of its face value. And when Bitcoin falters, it takes everything else in crypto down with it.

The entire crypto space has been a Jenga stack of interconnected time bombs for months now, getting ever more interdependent as the companies find new ways to prop each other up.

Which company blew out first was more a question of minor detail than the fact that a blow-out was obviously going to happen. The other blocks in the Jenga stack will have a hard time not following suit.

Here’s a quick handy guide to the crypto crash — the systemic risks in play as of June 2022. When Bitcoin slips below $20,000, we’ll officially call that the end of the 2021 bubble.

Recent disasters

TerraUSD collapse — Since stablecoins — substitutes for dollars — are unregulated, we don’t know what’s backing them. In the case of TerraUSD (UST), which was supposed to represent $18 billion … nothing was backing it. UST crashed, and it brought down a cascade of other stuff. [David Gerard; Foreign Policy; Chainalysis Report]

Celsius crumbles — Celsius was the largest crypto lender in the space, promising ridiculously high yields from implausible sources. It was only a matter of time before this Ponzi collapsed. We wrote up the inevitable implosion of Celsius yesterday. [David Gerard]

Exchange layoffs — Coinbase, Gemini, Crypto.com, and BlockFi have all announced staff layoffs. Crypto exchanges make money from trades. In a bear market, fewer people are trading, so profits go downhill. Coinbase in particular had been living high on the hog, as if there would never be a tomorrow. Reality is a tough pill. [Bloomberg; Gemini; The Verge]

Stock prices down — Coinbase $COIN, now trading at $50 a share, has lost 80% of its value since the firm went public in June 2021. The company was overhyped and overvalued.

US crypto mining stocks are all down — Bitfarms ($BITF), Hut 8 Mining ($HUT), Bit Digital ($BTBT), Canaan ($CAN), and Riot Blockchain ($RIOT). Miners have been borrowing cash as fast as possible and are finding the loans hard to pay back because Bitcoin has gone down.

UnTethering

Crypto trading needs a dollar substitute — hence the rise of UST, even as its claims of algorithmic backing literally didn’t make sense. What are the other options?

Tether — We’ve been watching Tether, the most popular and widely used stablecoin, closely since 2017. Problems at Tether could bring down the entire crypto market house of cards.

Tether went into 2020 with an issuance of 4 billion USDT, and now there are 72 billion USDT sloshing around in the crypto markets. As of May 11, Tether claimed its reserve held $83 billion, but this has dropped by several billion alleged “dollars” in the past month. There’s no evidence that $10.5 billion in actual dollars was sent anywhere, or even “$10.5 billion” of cryptos.

Tether is deeply entwined with the entire crypto casino. Tether invests in many other crypto ventures — the company was a Celsius investor, for example. Tether also helped Sam Bankman-Fried’s FTX exchange launch, and FTX is a major tether customer.

Tether’s big problem is the acerbic glare of regulators and possible legal action from the Department of Justice. We keep expecting Tether will face the same fate as Liberty Reserve did. But we were saying that in 2017. Nate Anderson of Hindenburg Research said he fully expects Tether execs to end the year in handcuffs.

Other stablecoins — Jeremy Allaire and Circle’s USDC (54 billion) claims to be backed by some actual dollars and US treasuries, and just a bit of mystery meat. Paxos’ USDP (1 billion) claims cash and treasuries. Paxos and Binance’s BUSD (18 billion) claims cash, treasuries, and money market funds.

None of these reserves have ever been audited — the companies publish snapshot attestations, but nobody looks into the provenance of the reserve. The holding companies try very hard to imply that the reserves have been audited in depth. Circle claims that Circle being audited counts as an audit of the USDC reserve. Of course, it doesn’t.

All of these stablecoins have a history of redemptions, which helps boost market confidence and gives the impression that these things are as good as dollars. They are not.

Runs on the reserves could still cause issues — and regulators are leaning toward full bank-like regulation.

Sentiment

There’s no fundamental reason for any crypto to trade at any particular price. Investor sentiment is everything. When the market’s spooked, new problems enter the picture, such as:

Loss of market confidence — Sentiment was visibly shaken by the Terra crash, and there’s no reason for it to return. It would take something remarkable to give the market fresh confidence that everything is going to work out just fine.

Regulation — The US Treasury and the Federal Reserve were keenly aware of the spectacular collapse of UST. Rumour has it that they’ve been calling around US banks, telling them to inspect anything touching crypto extra-closely. What keeps regulators awake at night is the fear of another 2008 financial crisis, and they’re absolutely not going to tolerate the crypto bozos causing such an event.

GBTC — Not enough has been said about Grayscale’s Bitcoin Trust, and how it has contributed to the rise and now the fall in the price of bitcoin. GBTC holds roughly 3.4 percent of the world’s bitcoin.

All through 2020 and into 2021, shares in GBTC traded at a premium to bitcoin on secondary markets. This facilitated an arbitrage that drew billions of dollars worth of bitcoin into the trust. GBTC is now trading below NAV, and that arbitrage is gone. What pushed bitcoin up in price is now working in reverse.

Grayscale wants to convert GBTC into a bitcoin ETF. GBTC holders and all of crypto, really, are holding out hope for the SEC to approve a bitcoin ETF, which would bring desperately needed fresh cash into the crypto space. But the chances of this happening are slim to none.

The bitcoins are stuck in GBTC unless the fund is dissolved. Grayscale wouldn’t like to do this — but they might end up being pressured into it. [Amy Castor]

Whales breaking ranks — Monday’s price collapse looks very like one crypto whale decided to get out while there was any chance of getting some of the ever-dwindling actual dollars out from the cryptosystem. Expect the knives to be out. Who’s jumping next?

Crypto hedge funds and DeFi

Celsius operated as if it was a crypto hedge fund that was heavily into DeFi. The company had insinuated itself into everything — so its collapse caused major waves in crypto. What other companies are time bombs?

Three Arrows Capital — There’s some weird stuff happening at 3AC from blockchain evidence, and the company’s principals have stopped communicating on social media. 3AC is quite a large crypto holder, but it’s not clear how systemically intertwined they are with the rest of crypto. Perhaps they’ll be back tomorrow and it’ll all be fine. [Update: things aren’t looking good. 3AC fails to meet lender margin calls.] [Defiant; Coindesk; FT]

BlockFi — Another crypto lender promising hilariously high returns.

Nexo — And another. Nexo offered to buy out Celsius’ loan book. But Nexo offers Ponzi-like interest rates with FOMO marketing as well, and no transparency as to how their interest rates are supposed to work out.

Swissborg — This crypto “wealth management company” has assets under management in the hundreds of millions of dollars (or “dollars”), according to Dirty Bubble Media. [Twitter thread]

Large holdings ready for release

Crypto holders have no chill whatsoever. When they need to dump their holding, they dump.

MicroStrategy — Michael Saylor’s software company has bet the farm on Bitcoin — and that bet is coming due. “Bitcoin needs to cut in half for around $21,000 before we’d have a margin call,” Phong Le, MicroStrategy’s president, said in early May. MicroStrategy’s Bitcoin stash is now worth $2.9 billion, translating to an unrealized loss of more than $1 billion. [Bloomberg]

Silvergate Bank — MicroStrategy has a $205 million loan with Silvergate Bank, collateralized with Bitcoin. Silvergate is the banker to the US crypto industry — nobody else will touch crypto. Silvergate is heavily invested in propping up the game of musical chairs. If Silvergate ever has to pull the plug, almost all of US crypto is screwed. [David Gerard]

Bitcoin miners — Electricity costs more, and Bitcoin is worth less. As the price of Bitcoin drops, miners find it harder to pay business expenses. Miners have been holding on to their coins because the market is too thin to sell the coins, and borrowing from their fellow crypto bros to pay the bills since July 2021. But some miners started selling in February 2022, and more are following. [Wired]

Mt. Gox — at some point, likely in 2022, the 140,000 bitcoins that remained in the Mt. Gox crypto exchange when it failed in 2014 are going to be distributed to creditors. Those bitcoins are going to hit the market immediately, bringing down the price of bitcoin even further.

Feature image by James Meickle, with apologies to XKCD and Karl Marx.

Don’t forget to subscribe to our Patreon accounts. Amy’s is here and David’s is here. We need your supportfor stories like this!

The Securities and Exchange Commission is being inundated by thousands of comments solicited by Grayscale to support the conversion of their Grayscale Bitcoin Trust (GBTC) into a spot bitcoin ETF. [Comments on NYSE Arca Rulemaking]

As part of the filing, the SEC provides a comment period of 240 days. NYSE Arca filed the application on October 19, 2021, so the last day for comments is June 16.

Bitcoin skeptics refer to GBTC as the Bitcoin Roach Motel or Hotel California, a place you can check in but never leave because once bitcoin goes into the trust, it has no obvious way of getting out. I covered the details of how the trust works in an earlier blog post. [Amy Castor]

GBTC is currently trading at 25% below the price of bitcoin. Grayscale argues that converting it to a spot bitcoin ETF will allow GBTC to trade in line with its underlying asset.

In truth, Grayscale can redeem shares and return investors their money, but it stands to make hundreds of millions of dollars more with an ETF, so you should definitely spam the SEC instead!

Grayscale has encouraged spamming the commission through a massive ad campaign at Amtrak stations. Grayscale CEO Michael Sonnenshein is going around giving press interviews, pointing out how mean and evil the SEC is for never having approved a spot bitcoin ETF in the past.

On its website, Grayscale offers a link that opens up directly to a ready-made email, making it mindlessly easy to spam the SEC in a few simple clicks.

Jorge Stolfi, a computer scientist in Brazil, has been reading through the SEC comments one by one and posting his thoughts on Twitter.

Nearly 4,000 comments have been submitted so far, and 98% of them are positive in that they support converting GBTC to a bitcoin ETF. Some of the names look suspiciously made up.

Thousands of the comments are copies of the same Grayscale spam message, and many don’t even bother to edit the “[YOUR NAME HERE]” placeholders.

Thanks to the torrent of spam letters to the SEC re making GBTC into an ETF, I learned two more financial terms: "contango" and "backwardation".

I feel embarrassed for having to learn them from guys who cannot even edit "***[YOUR NAME HERE]***" placeholders in spam messages.

Many of the comments parrot Sonnenshein’s remarks to the press about how the SEC has approved a bitcoin futures ETF; therefore, it should also approve a spot. (This is nonsense. The former is an actual bet on dollars. Nobody touches BTC at any point in the process.)

Hopefully, the SEC will read the spam comments and understand them for what they are: clear evidence that thousands of GBTC investors do not understand the nature of bitcoin, and that GBTC should not be converted to an ETF for the sake of those same investors.

In reading through the comments something else becomes alarmingly clear — many retail investors are stuck with GBTC in their retirement accounts. Thanks to a television ad campaign that Grayscale ran in 2020, many falsely believed that bitcoin was a hedge against inflation, rather than an incredible risky and volatile asset.

Amongst the positive comments, Coinbase submitted a ridiculously long (27 pages) letter trying to demonstrate that the bitcoin market cannot be manipulated. They somehow forgot to mention the 83 billion tethers currently sloshing around in the crypto markets. [SEC Comment]

Last year, Coinbase settled charges with the CFTC that one of its own employees was wash trading the vast majority of a certain coin’s volume on their own exchange, and they apparently weren’t aware of it until much later. I’m sure they have a lot of credibility on this subject!

Voices against the GBTC conversion

There are a few powerful letters to the SEC against the conversion. These are definitely worth a read for anyone who wants to get a better understanding of how GBTC works.

Writing on behalf of a client, Ropes & Gray Attorney David Hennes does a fantastic job underscoring how Grayscale is royally screwing over GBTC holders. [SEC Comment]

As Hennes points out, Grayscale bought $700 million worth of its own GBTC shares at a discount and is authorized to buy back $1.2 billion.

If GBTC converts to an ETF, Grayscale would then be authorized to sell the corresponding bitcoins at the market price, thus making some $200 million to $350 million in profit at the expense of those who sold them the shares at discount.

Since Grayscale is no longer issuing shares of GBTC, it can redeem GBTC at net asset value without running afoul of Regulation M, as it had in the past. However, it chooses not to because it is collecting a 2% management fee on $25 billion in BTC assets held in the trust.

“The SEC should thus deny the conversion of GBTC into an ETF unless and until Grayscale first (a) initiates a redemption program for GBTC that complies with Regulation M; and (b) agrees to distribute to GBTC’s other shareholders on a pro-rata basis any and all gains resulting from any Grayscale purchases of GBTC shares at a discount and corresponding sales of GBTC shares on an undiscounted basis,” wrote Hennes.

Computer scientist David Rosenthal, who gave a popular lecture at Stanford warning about the hazards of crypto, says all of the reasons the SEC had for rejecting previous bitcoin spot ETFs — and there have been close to a dozen of them — are still valid.

“The constant pressure to approve a spot Bitcoin ETF exists because Bitcoin is a negative-sum game. Bitcoin whales need to increase the flow of dollars in so as to have dollars to withdraw. The SEC should not pander to them.” [SEC Comment]

Rosenthal also comments on my Grayscale story in his blog. [DSHR blog]

Along that same vein, David Golumbia, author of “The Politics of Bitcoin,” warns “manipulators in the crypto space need a constant inflow of real dollars to prop up their manipulation so that they can continue to dump their tokens into the hands of ever more unsuspecting consumers. That they are obviously engaged in selling their own tokens for a profit while bullying others into buying at the same time is only one of many tactics they use that are illegal in well-ordered markets.” [SEC Comment]

In his own submission, Stolfi states that bitcoin is a tool of crime. It allows dark markets to exist and flourish. It has taken the place of the now-defunct criminal bank Liberty Reserve. And it functions as a natural Ponzi. [SEC comment]

“Bitcoin does not provide any benefits for society; on the contrary, it has caused enormous damage; and this balance cannot ever improve, because the technology is inherently wasteful, impractical, illegal, and insecure.”

Someone going by “Concerned Citizen of the Word” noted that “It’s just a matter of time before the Bitcoin bubble pops due to any of many reasons, and a lot of people, especially Americans, are going to lose massively.” [SEC comment]

If you are similarly disturbed by Grayscale’s campaign of misinformation, I encourage you to write to the SEC and make your own voice heard — with original commentary, which I’m sure they would appreciate. You can submit your comments here.

If you like my work, consider supporting my writing by subscribing to my Patreon account for $5 or $20 a month. Every little bit helps.

The DOJ found 119,754 bitcoins stolen from crypto exchange Bitfinex in a hack in 2016. Federal officials were able to seize 94,643.29 BTC ($3.6 billion). The rest is still out there. (Washington Post)

On Jan. 31, those funds were spotted moving out of the hacker’s wallet, but nobody realized at the time it was the feds moving the funds. Most people assumed it was the hackers themselves!

Heather Morgan, 31, and Ilya Lichtenstein, 34, were charged with trying to launder the bitcoins. They were arrested in NYC, where they live. (DoJ press release, Complaint, Statement of facts)

Lichtenstein is Russian-American. Morgan is a U.S. citizen, who grew up in California. We don’t know if the pair were behind the actual theft, but they probably were given the majority of the coins were in the same wallet as when they left Bitfinex.

David Gerard describes the 2016 hack in Chapter 8 of his book “Attack of the 50-foot Blockchain,” as told to him by Phil Potter. He summarized it on Twitter.

Morgan is a rapper with loads of embarrassing videos online. (Vice)

She had an active TikTok account featuring her rap moves.

Morgan was also a prolific Forbes contributor, which should surprise nobody. (Forbes)

And she gave a talk at NYC Salon on how to social engineer your way into anything. (Youtube)

The couple sat on those coins from August 2016 to January 2017, before trying to launder some of them. Almost all of the BTC they moved went through AlphaBay, which they used as a mixer. The feds were able to spot this because they seized AlphaBay in July 2017.

One overlooked detail in the Razzlekahn arrest. Almost all the money went through AlphaBay, using it as a mixer. The feds were able to see through this because they seized AlphaBay. Its amazing how, even years after, darknet market seizures pay dividends to the feds.

This arrest underscores how difficult it is to actually launder bitcoin. All of the transactions are traceable. Even when you are sitting on piles of BTC, as these two allegedly were, it is really difficult to cash out.

A judge ruled the pair could be released on bonds — $5 million for Lichtenstein; $3 million for Morgan. But the government, which originally asked for a $100 million bond, ordered a review of the detention order, saying the couple have the means to flee — $330 million in BTC have yet to be found. Also, Russia has no extradition treaty with the U.S. (Stay of release)

It’s not clear what will happen to the recovered funds at this point, but likely they will be held up by the U.S. government for a long time to come. (Decrypt)

Bitfinex is absolutely convinced it will receive the recovered funds. It wants to use 80% of them to “burn” one of its shitcoins — LEO. (Bitfinex blog)

Naturally, LEO saw a surge in value after the announcement. (Defiant)

Bitfinex is the sister company of Tether. The 2016 hack set off a string of calamities for the two firms. Rather than claim insolvency, Bitfinex gave its customers a 36% haircut, repaid them in BFX tokens, and then lost its banking. Thus began a prolific printing of tethers, telling lies and other nonsense that has continued to this day. Also, it was Bitfinex’s reliance on third-party payment processors after it lost its banking that led to all the problems with Crypto Capital, some missing $850 million in funds, and the NYAG telling Tether to take its business out of New York. I detail most of this in my timeline.

Bitfinex never really paid its customers back for the 36% haircut. Ultimately, all of those customers were paid back in tethers, so why should Bitfinex get that money?

BlockFi to pay $100M

Crypto lender BlockFi is paying $50 million to the SEC and $50 million to various state regulators to settle claims that it illegally offered high-yielding crypto lending products, say sources. (Bloomberg)

It’s clear as mud how BlockFi is able to offer the rates it does. “Executives at BlockFi have said they are able to pay such high yields to customers because institutional investors will pay them even more to borrow the deposits. But the companies don’t provide a detailed accounting of how the funds are used or in what circumstances investors could lose their cryptocurrency,” writes Bloomberg.

Crypto lending programs are obviously securities subject to SEC regulation. BlockFi was funding its crypto lending operations and proprietary trading through the sale of unregistered securities. The SEC similarly warned Coinbase against launching “Lend.” And the regulator is currently looking into Celsius, Voyager Digital, and Gemini Trust regarding crypto yield products.

I didn’t realize this earlier, but apparently BlockFi is one of the largest holders of GBTC, buying it for the premium. GBTC is now trading at -24% of NAV, according to Ycharts.

Update: On June 21, 2022, Forbes announced the termination of the SPAC transaction. The transaction never closed due to the termination of the deal. [Forbes] __________

Forbes, the publication that featured alleged bitcoin money launderer Heather Morgan as a contributor, is now taking $200 million from Binance, the crypto exchange that has been thus far kicked out of every corner of the world for blatantly ignoring laws and regulations. (CNBC)

The funds will help Forbes follow through on its plan to merge with a special purpose acquisition company (SPAC) in the first quarter. Forbes is owned mainly by Chinese Firm Integrated Whale Media, which bought a controlling stake from the Forbes family in 2014.

This will make Binance one of the biggest owners of Forbes after its listing. Binance will also have two director positions on Forbes’ board of executives. Binance tried to sue Forbes in 2020 for defamation, but the suit was quietly dropped.

If you are looking for an unbiased crypto news source in the future, you probably want to look elsewhere.

“Does she have regrets? I kept waiting to hear them and she comes closest in the final few pages (after chapters of what does seem like a Kafkaesque nightmare in both legal and emotional terms). ‘I regret every moment of every day of the terrible year that followed Gerry’s death,’ is what she confesses. A weaselly mea culpa that reminded me of when people, often on reality shows, apologize by saying, ‘I am sorry you feel that way.’”

The Sun also has a review of the book. It’s mostly just… a review of the book. Nice photos of Jen and Gerry though.

On Feb. 5, a loophole in the Meter Passport smart contract allowed an attacker to siphon 1,391 ETH ($4.2 million) and 2.74 wrapped Bitcoin ($83,000) from the Meter Passport blockchain bridge.

Blockchain bridges allow you to conveniently spend crypto from one blockchain — such as ETH or, in this case, BTC — on another blockchain.

@ishwinder explains the hack in layman’s terms. (Twitter)

This is one of three recent hacks on blockchain bridges lately! On Feb. 3, we had the Wormhole exploit, with $320 million in funds stolen. And on Jan. 17, Qubit was hacked for $80 million in crypto.

What does this tell you about blockchain bridges?

Meter urged its users not to trade any meterBNB, which are currently unbacked, and said that they were “working on compensating funds to all affected users.” (Twitter)

Community, unfortunately Meter Passport was hacked a few hours ago. Please do not trade the unbacked meterBNB that is circulating on Moonriver.

We have identified the issue: Passport has a feature to automatically wrap and unwrap gas tokens like ETH and BNB for user convenience.

The U.S. Department of Treasury released a report: “Study of the Facilitation of Money Laundering and Terror Finance Through the Trade in Works of Art.” The report was mandated by Congress in the AML Act of 2020. It specifically mentions NFTs. (Press release, Study, Blockchain Law Center)

According to the report, NFTs are vulnerable to money laundering because “NFT platforms range in structure, ownership, and operation, and no single platform operates the same way or has the same standards or due diligence protocols.”

The report specified that NFTs used for payment or investment may fall under the virtual asset definition, and some NFT platforms may qualify as virtual asset service providers (VASPs), depending on the characteristics of the NFTs that they offer.

The report makes it clear that the Treasury department is carefully monitoring digital art assets, including NFTs, and the online marketplaces where they are traded. (JDSupra)

Grayscale wants to turn its Grayscale Bitcoin Trust (GBTC) into an exchange-traded fund. The SEC is seeking advice from the public about whether ETFs tied to Bitcoin’s spot price could be a vehicle for fraud. The SEC has denied six similar applications since November, including those from VanEck, WisdomTree and SkyBridge Capital. (SEC notice, Coindesk)

Only licensed banks should be allowed to issue stablecoins, according to Jean Nellie Liang, the under secretary for domestic finance at the Department of the Treasury. She appeared before the House of Representatives Committee on Financial Services to reaffirm the PWG’s November report on stablecoins. (Liang’s written testimony, Bloomberg)

Time is running out for crypto firms to be approved for the UK’s anti-money laundering register before the end of March. Ninety-six applicants are still waiting for a decision on their application. Without approval before a March 31 deadline, the future of these crypto firms’ UK operations — including exchanges, wallets and other businesses — hangs on a limb. (The Block)

Crypto shilling at the Super Bowl, and other NFT news

It’s Super Bowl weekend. Expect to see a massive amount of marketing dollars go toward shilling crypto and NFTs. Crypto.com, FTX, and Binance are among the major advertisers. (Hollywood Reporter) (NYT)

Bored Apes are also rumored to appear at the Super Bowl, in some shape or form. (Bloomberg)

Twitter accounts that have been speaking out against NFTs are being reported by bots, their accounts suspended and/or locked. This happened to @NFTEthics and @interlunations. (Twitter)

We are back. Twitter’s suspension of our account, based on the fact that we were supposedly impersonating someone else (LOL) could not have been a bigger justification for the existence of Web3. And for that we kindly thank all the scammers and their bot armies that reported us❤️

Sotheby’s is planning to auction off a set of 104 CryptoPunks on Feb. 23. The set is expected to bring $20 million to $30 million in crypto. The original buyer was 0x650d, who scooped them all up in July 2021. Here is the Etherscan confirming his purchase. (Artnet News)

He bought them for $7 million because he “chose wealth.” (Twitter)

Why did I spend $7MM on 104 floor punks? Easy: because I choose wealth. 🧵/1

Following the news of the Sotheby’s auction, the celebrity shilling begins. German-American model Heidi Klum just announced on Twitter she owns a Punk. (Tweet)

Who paid for her Punk? That’s not exactly clear. Mike Burgersburg (not his real name, obviously) has tracked down links between Bitclout investor Reade Seiff and Klum’s Punk. (Dirty Bubble)

Burgersburg also says whoever is funding Reese Witherspoon’s NFT purchases probably has a financial interest in promoting the WOW project. (Dirty Bubble)

In addition to proper FTC disclosure requirements, fans and retail buyers deserve more transparency about how these deals are made and who’s providing the money to pump up these assets.

John Reed Stark was chief of the SEC office of internet enforcement for 11 years. He has a few things to say about NFTs: Market manipulation of NFTs appears not only rampant and tolerated, but also encouraged. Fraud not only rewarded, but also taught. (Linkedin)

The counterfeit NFT problem is getting worse. Bots are scraping artists’ online galleries, or even keyword searches on Google Images, and then creating collections with auto-generated texts. Those listings have proliferated on OpenSea. (Verge)

Sotheby’s made headlines last year when it sold Kevin McCoy’s Quantum NFT (2014) for $1.47 million. Now, that sale is in the headlines once more, this time for a lawsuit being filed against McCoy and the auction house by a holdings company whose owner claims he owns Quantum. (Artnews)

Indie game platform itch.io has come out strongly against NFTs: “NFTs are a scam. If you think they are legitimately useful for anything other than the exploitation of creators, financial scams, and the destruction of the planet the we ask that [you] please reevaluate your life choices.”(Twitter, PC Gamer)

A few have asked about our stance on NFTs:

NFTs are a scam. If you think they are legitimately useful for anything other than the exploitation of creators, financial scams, and the destruction of the planet the we ask that please reevaluate your life choices.

YouTube is launching new creator tools to expand monetization, including allowing creators to sell content as NFTs so fans can “own” videos. (NBC News)

The Alfa Romeo Tonale SUV is the “first car on the market” to come with an NFT digital certificate that the automaker says will increase the car’s residual value. How? Technical details are thin. (Verge)

A group supporting WikiLeaks founder Julian Assange raised $50 million in ETH by selling an NFT of a clock to a DAO (called AssangeDAO) set up to support his legal bills. The NFT, titled “Clock,” is a joint creation by Assange and digital artist Pak. AssangeDAO contributors receive $JUSTICE. (Wired)

someone is going to have a hundred million dollar business cleaning up the mess that DAO dipshittery is already causing

David Rosenthal’s talk at Stanford is a summary of everything that is wrong with crypto and blockchain technology. This is a great read. (DSHR blog)

Vice interviewed Dan Olsen, whose Youtube video on NFTs went viral. “I’ve been keeping my thumb on what’s going on in crypto. By and large, it’s been the story of the evolution of fraud.” (Vice)

The BBC published and then took unpublished a story about a “self-made crypto millionaire giving back” without mentioning his scam coin. (archive)(missing story)

“City Coins — free, magical money for your city! Maybe” (David Gerard)

Fais Khan’s part II of his work explaining how VCs cash out on tokens: “The Unstoppable Grift: How Coinbase and Binance Helped Turned Web3 into Venture3.” (Fais Khan)

The U.S. government’s system for spotting money laundering has received a surge of suspicious activity reports from a set of San Francisco financial companies that includes some of the world’s leading crypto exchanges. (FT, Dynamics Securities Analytics report)

Mark Zuckerberg is lying about the Metaverse. The CEO of one of the most valuable companies in the world is shoving $10 billion into a concept he cannot describe. (Ed Zitron)

The Russian government will treat bitcoin and digital assets as currency. The proposal includes subjecting crypto transactions (not just within exchanges) to AML/KYC rules, which, being technically impossible to execute, should be equivalent to a ban…(Blockworks)

If you like my work, please consider supporting my writing by subscribing to my Patreon account for $5 or $20 (or even more!) a month. Every little bit helps.

Bitcoin is sitting at around $54,000, and Tether has hit a new milestone: 50 billion tethers in circulation, something it’s quite proud of. “Will we reach $100B before 2022?”

🎉 Tether has just surpassed $50B market cap! 🚀Tether’s market cap is growing fast, with a monthly increase of $10B. Will we reach $100B before 2022?

So far, in April, Tether has issued 9 billion tethers—and the month isn’t even over yet. Tether has been minting 2 billion tethers at a time—the largest single batches we’ve seen to date.

Per the NY AG settlement agreement, Tether is supposed to provide a breakdown of its reserves in May. And they are already whining about how unfair and unjust this is.

Stuart Hoegner, Tether’s general counsel, complained on Twitter: “The second-biggest stablecoin issuer [USDC] doesn’t give a breakdown of their reserves, either. Observers should ask why our detractors are pushing one rule for them and another for us.”

(USDC—a stablecoin bootstrapped by Coinbase and Circle—has issued 13.5 billion USDC to date, not quite the level of Tether, but it’s working its way up there.)

Coinbase debuts on Wall Street, then lists USDT

Coinbase, the largest crypto exchange in the U.S., debuted on Wall Street on April 14. Trading opened at $381 a share—a 52% increase over a $250 reference price set by Nasdaq. COIN swung as high as $429 that first day. (Though, now it is at $291.)

It was the moment Coinbase execs and its VC backers had all been waiting for. They didn’t waste any time dumping their shares on retailers, according to data from Capital Market Laboratories.

Insiders sold off $4.6 billion in COIN on the first day of trading, and Coinbase CEO Brian Armstrong sold shares worth $292 million. (SEC filing)(Cointelegraph)

Less than two weeks later, Coinbase—being the respected operation that it is—dropped the bomb that it is listing tether on Coinbase Pro.

Ecstatic bitcoiners claim the move legitimizes Tether. Actually, the move delegitimizes Coinbase.

Listing tether makes Coinbase look shady, like they’ll do anything to boost profits and keep share prices up so insiders can continue their sell-off. (My blog post)

Tether is a wildcat bank, operating with no oversight. It has been largely responsible for boosting the price of bitcoin because it allows unregulated crypto exchanges to thrive and funnels them a steady stream of dubiously backed tethers.

How, HOW do the laser noodles have the audacity to complain about “fiat money printing”? Totally baffles me. They can’t seriously believe that anyone has just put $200m into the crypto economy.

Thanks to Tether, Coinbase had a hugely profitable Q1. And thanks to Tether, Brian Armstrong is a wealthy man indeed.

Was it a coincidence that BTC tapped a new all-time high of $63,275 the day before Coinbase went public? Or was that simply irrational exuberance?

When Tether gets taken down, liquidity will evaporate and crypto markets will crash. Those who get hurt will be naive retailers, who didn’t understand the system was rigged from the get-go.

Bernie—gone but not forgotten

Bernie Madoff died in jail on the same day that Coinbase went public. He ran the biggest Ponzi scheme in history, and it went on for 25 years. Paper losses totaled $64.8 billion. Madoff took billions from investors and simply stole the money instead of investing.

Why didn’t the SEC catch Madoff sooner? Why didn’t they step in and do something to protect investors? They were tipped off eight years before, and yet they failed to act.

Here we are watching a similar drama unfold with Tether. All the red flags are waving. And no regulator or authority has stepped in to take strong action.

You know what would be nice, if financial regulators actually did their job rather than having the tech industry regulate itself internally.

I guess I can blame the federal government for effectively being run by a clown mafia for the last four years. 😒

If you are wondering how fraudsters live with themselves—they rationalize and minimize.

David Sheehan, a trustee who worked to recover money stolen from investors, met with Madoff a dozen times. He told WSJ: “[Madoff] didn’t think he was harming anybody. He actually thought his scheme would work, that it just got out of hand and he couldn’t control it.”

$2 billion crypto scam in Turkey?

When Thodex, one of the largest crypto exchanges in Turkey, suspended trading on April 18 for five days of “maintenance,” users began to complain they couldn’t access their funds.

Now a manhunt is underway for the exchange’s 27-year-old founder, Faruk Fatih Özer, who has reportedly fled to the capital of Albania with $2 billion in investors’ money.

Turk authorities have detained 62 people and issued detention warrants for 16 more.

Meanwhile, Özer is claiming that Thodex is the target of a “smear campaign.” He says he was on a jaunt to meet with foreign investors, nothing more.

We’ve seen this film before. It’s called “Crypto exchange operates as a Ponzi scheme.” Last time, the protagonist was Gerald Cotten, the founder of Canada’s QuadrigaCX. And instead of going to meet with “foreign investors,” he went to India and died under suspicious circumstances.