- By Amy Castor and David Gerard

- Be sure to subscribe to our Patreon accounts — Amy’s is here; David’s is here.

We often get asked by reporters: “Why are crypto markets crashing?” The short answer is because there’s no money left, and no more coming in. The long answer is more complicated.

Bitcoin peaked at $64,000 in April 2021 and again at $69,000 in November 2021. Many of the network effects that drove the price of bitcoin to those heights were put into place in 2020.

The same network effects are now working in reverse. Markets take the stairway up and the elevator down.

The 2017 bubble was fueled by the ICO boom and actual outside dollars entering the crypto economy. Bitcoin topped out just below $20,000 in December 2017.

The crash that followed over the next 12 months was like air being slowly let out of a balloon — much like the 2014 deflation after Bitcoin’s prior 2013 peak. ICO and enterprise blockchain promoters tried to keep going through 2018 like everything was fine, but the party was clearly over.

In contrast, the 2022 crash is like a wave of explosive dominoes all crashing down in rapid succession. How did we get here?

A long, cold crypto winter

Let’s start in early 2020. It was the crypto winter. Bitcoin’s price had spent two years bobbling up and down from infusions of tethers, and traders on BitMEX rigging the price to burn margin traders. (And, allegedly, BitMEX itself burning its margin traders.) [Medium, 2018]

But the dizzying price rises were peculiarly bloodless. There was little evidence of fresh outside dollars from retail investors — the ordinary people. The press would write how bitcoin had just hit $13,000 — but they’d also call people like us, and we’d tell them about Tether.

Throughout 2019 and into 2020, crypto pumpers were desperately trying scheme after scheme — initial coin offerings, initial exchange offerings, bitcoin futures, selling to pension funds — to lure in precious actual dollars and get the party re-started.

Then Corona-chan knocked on the door.

Act I, Scene I: Pandemic Panic

On March 13, 2020, the US government declared a pandemic emergency. The panic drove down stocks and crypto. Investors sold everything and flew to the safest, hardest form of money they could find: the US dollar! Bitcoin dropped from $7,250 to $3,858 over the course of that day.

It was an edge-of-the-cliff moment for bitcoin. Any further drop could force liquidations and create a ripple effect across dozens more crypto projects. For bitcoin miners, the price of bitcoin was now below the cost of mining.

Worse, only two months away was the bitcoin “halvening” — an every-four-year event when the number of bitcoins granted in each freshly-mined block halves. If bitcoin dropped too low in price, the miners wouldn’t be able to pay their enormous power bills. The crypto industry desperately needed to push bitcoin’s price back before May.

Tether spins up the printing press

Tether, launched in 2014, is an offshore crypto company that issues a dubiously backed stablecoin of the same name. Tether works like an I.O.U. — Tether supposedly takes in dollars and issues a tether for each dollar held in reserve. Since Tether has never had an audit, nobody knows for sure what’s backing tethers. The company has an extensive history of shenanigans — see Amy’s Tether timeline.

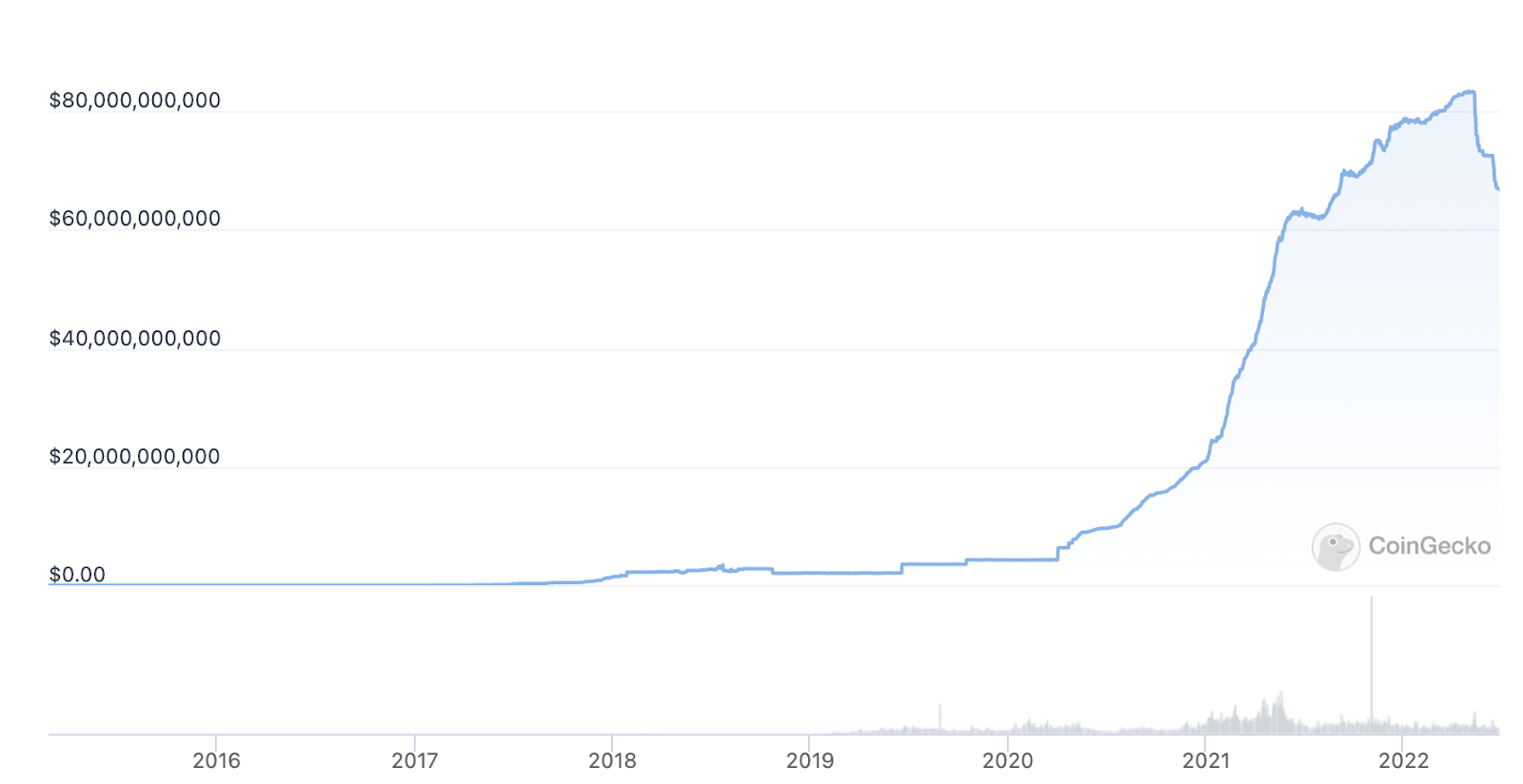

The issuance of tethers in March 2020, was 4.3 billion, but that’s when the Tether printer kicked into overdrive — minting tethers at a clip nobody had ever seen before.

Tether minted 4.4 billion tethers in April 2020 — crypto’s version of an economic stimulus package. By May, Bitcoin reached $10,000, just in time for the halvening.

Once the price of bitcoin goes up, though, there’s no way to turn off the Tether printing press. It has to keep printing. If the price of bitcoin goes down, people will sell, creating an exodus of real dollars from the system. So Tether kept printing, pushing the price of bitcoin ever skyward.

In May, June, and July 2020, Tether issued a combined total of 3 billion tethers. In August, when the price of bitcoin reached $12,000, Tether issued another 2.6 billion tethers. In September, when bitcoin slid below $10,000, Tether issued another 2.2 billion tethers.

By the end of 2020, Tether had reached a market cap of 21 billion. The printer kept going. In 2021, Tether pumped out 60 billion more tethers. By May 2022, Tether’s market cap had reached 83 billion. Bitcoin’s price peaks in April 2021 ($64,000) and November 2021 ($69,000) both coincided with an influx of tethers into the market.

You can’t just redeem tethers. Only Tether’s big customers — it has about ten of them — can redeem. You can try to sell your tethers on an exchange. But you can’t just go up to Tether to redeem them for dollars. There were no redemptions of tethers, ever, until May and June 2022 — the present crash.

Curiously, Tether’s reserve as declared to New York in April 2019 contained $2.1 billion of actual money — cash and US Treasuries. But Tether’s reserve attestation as of March 31, 2021, still contained just $2.1 billion of cash and treasuries!

This suggests that the rest of the reserve over that time was made up of whatever worthless nonsense Tether could claim was a reserve asset — loans of tethers, cryptocurrencies, and dubious commercial paper credited at face value rather than being marked to market.

Dan Davies, in his essential book Lying for Money, marks this as the key flaw in frauds of all sorts: they have to keep growing so that later fraud will keep covering for earlier fraud. This works until the fraud explodes.

GBTC’s ‘reflexive Ponzi’

Grayscale’s Bitcoin Trust (GBTC) played a huge role in keeping the price of bitcoin above water through 2020. It offered a lucrative arbitrage trade, an exploitable inefficiency in markets, that a lot of big players went all-in on.

GBTC was an attempt to wrap Bitcoin in an institutionally compatible shell. All through 2020 and into 2021, GBTC was trading at a premium to bitcoin on the secondary markets. Accredited investors would acquire GBTC at net asset value — some large proportion being in exchange for direct deposits of bitcoins, not purchases for cash, although all the accounting was stated in dollars. After a six-month lock-up, the accredited investors would sell the shares to the public at a 20 percent premium, sometimes more. Rinse, repeat, and that’s a 40 percent return in a year.

GBTC functioned like a “reflexive Ponzi.” When Grayscale bought more bitcoin for the trust, that drove up the price of bitcoin, which pushed up the GBTC premium, which resulted in investors wanting more GBTC and Grayscale issuing more shares.

Grayscale ran a national TV advertising campaign at the time, targeted at ordinary investors. The ads warned that disaster was imminent, inflation would eat your retirement, and bitcoin was better than gold — so you should buy bitcoin. Or, this shiny GBTC, which was implied to be just as good! [YouTube, 2019]

In a bull market, retail investors didn’t mind paying a premium — because the price of bitcoin kept going up. The market treated GBTC as if it was convertible back to bitcoins, even though it absolutely wasn’t. [Adventures in Capitalism]

Grayscale ultimately flooded the market with GBTC. When an actual bitcoin ETF became available in Canada, GBTC’s premium dried up. Since February 2021, GBTC has been trading below the price of bitcoin. As of March 2022, the trust holds 641,637 bitcoins. And they’re staying there indefinitely — leaving GBTC holders locked in on an underwater trade.

The rise of decentralized finance

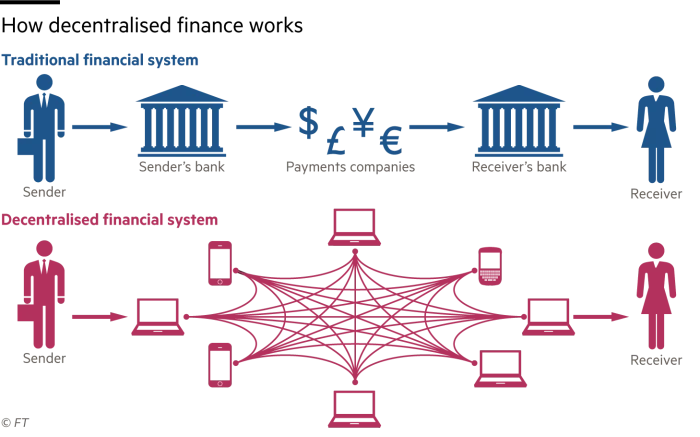

Decentralized finance, or DeFi, didn’t directly pump the price of bitcoin in 2020. But DeFi was one of the stars of the 2021 bubble itself, and eventually caused the bubble’s disastrous explosion. All of the structures to let that happen were set up through 2020.

DeFi is an attempt to put traditional financial system transactions — loans, deposits, margin trading — on the blockchain. Regulated institutions are replaced with unknown and unregulated intermediaries, and everything is facilitated with smart contracts — small computer programs running on the blockchain — and stablecoins.

All through 2019 and 2020, DeFi was heavily promoted as offering remarkable interest rates. At a time of low inflation, this got coverage in the mainstream financial press. Here’s the diagram the Financial Times ran, depicting DeFi as a laundromat for money: [FT, paywalled, archive]

The key to DeFi is decentralized exchanges, where you can trade any crypto asset that can be represented as an ERC-20 token — such as almost any ICO token — with any other ERC-20 token.

DeFi also lets you take illiquid tokens that nobody wants, do a trade, assign them a spurious price tag in dollars, then say they’re “worth” that much. This lets dead altcoins with no prospective buyers claim a price and a market cap, and attract attention they don’t warrant. If you put a dollar sign on things, then people take that price tag seriously — even when they shouldn’t.

You can also create a price for a token that you made up out of thin air yesterday and use DeFi to claim an instant millions-of-dollars market cap for it.

This was the entire basis for the valuation of Terraform Labs’ UST and luna tokens — and people believed those “$18 billion” in UST were trustworthily backed by anything.

You can also use those tokens you created out of thin air as collateral for loans to acquire yet more assets. An unconstrained supply of financial assets means more opportunities for bubbles to grow, and more illiquid assets that you can dump for liquid assets (BTC, ETH, USDC) when things go wonky.

By September 2020, five hundred new DeFi tokens had been created in the previous month. DeFi hadn’t hit the mainstream yet — but it was already the hottest market in crypto. [Bloomberg]

The problem was that in 2020, to use DeFi you had to know your way around using the actual blockchain. Retail investors, and even most institutional investors, haven’t got the time for that sort of dysfunctional nonsense.

Retail was more attracted to the “CeFi” (centralized DeFi) investment firms, such as Celsius and 3AC, offering impossible interest rates. These existed in 2020 but didn’t gain popularity until the following year when the bubble had started properly.

A new grift: NFTs

By late 2020, crypto promoters were searching for a new grift to lure in retail money, one that would have broader mainstream appeal. They soon found one.

NFTs as we know them got started in 2017, with CurioCards, CryptoPunks, and CryptoKitties. NFT marketing had continued through the crypto winter — in the desperate hope that ordinary people might put their dollars into crypto collectibles.

The foundations of the early 2021 burst of art NFTs were laid in late 2020, when Vignesh Sundaresan, a.k.a. Metakovan, first started looking into promoting digital artists, such as Beeple — whose $69 million JPEG made international headlines for NFTs in March 2021, and officially kicked off the NFT boom.

Late 2020 also saw the launch of NBA Top Shot, the only crypto collectible that ever got any interest from buyers other than crypto speculators. Top Shot traders were disappointed at how incredibly slow Dapper Labs was at letting them withdraw the money they’d made in trading — and became some of the first investors in the Bored Apes.

Coiner CEOs

By late 2020, several big company CEOs started promoting the concept of bitcoin on the company dime. These included Jack Dorsey at Twitter, Dan Schulman at PayPal, and Michael Saylor at business software company MicroStrategy.

In October 2020, Saylor revealed his company had bought 17,732 bitcoins for an average of $10,000 per coin. Over the next 18 months, Microstrategy would plow through its cash reserves and take on debt to funnel more money into bitcoin, spending $4 billion in the process. Buying MSTR shares become the newest way for retail investors to bet on bitcoin. Saylor also put himself forward as bitcoin’s latest prophet and crazy god.

PayPal set up bitcoin trading in 2020, though only as a walled garden, where you couldn’t move coins in or out. Still, it made gambling on crypto more accessible to retail investors.

Bitcoin miners start ‘hodling‘

By late 2020, we suspect there was very little actual cash in crypto. But bitcoin needed to continue its upward ascent.

The biggest tip-off that the fresh outside dollars had stopped flowing was when bitcoin miners stopped selling their coins. Bitcoin miners mint 900 new bitcoins per day. They typically sell these to pay their energy costs — power companies don’t accept tether — and buy new mining equipment, which becomes obsolete every 18 months. At $20,000 per bitcoin, that would equate to $18 million, in actual dollars, getting pulled out of the bitcoin ecosystem every day.

In October 2020, Marathon Digital (MARA), one of the largest publicly traded miners, stopped selling its bitcoins. They took out loans, which allowed them to buy their equipment and hold their bitcoins. Marathon even bought additional bitcoins!

Borrowing against mined bitcoins, and not selling them, reduced selling pressure on bitcoin’s price in dollars. US-based miners used this model heavily from July 2021 onward — taking low-interest loans from their crypto buddies, Galaxy Digital, DCG, and Silvergate Bank. Although, in 2022, the loans started running out and they had to start selling bitcoins.

This also set Marathon up for potential implosion when energy prices went up and the price of bitcoin dropped in 2022. Marathon is presently losing $10,000 on every bitcoin they mine.

Easy money?

2020 was a weird year of market panics, bored day traders, and easy money — for some.

The Federal Reserve dealt with the pandemic panic by showering the markets with stimulus money. At the retail end, $817 billion was distributed in stimulus checks (Economic Impact Payments), $678 billion in extended unemployment, and $1.7 trillion to businesses, mostly as quickly-forgiven loans. [New York Times]

Bored day traders, stuck at home working their email jobs and unable to go out in the evening, got into trading stocks on Robinhood as the hot new mobile phone game. Car rental firm Hertz, a literally bankrupt company, whose stock was notionally worth zero, started going up just because Robinhood users thought it was a good deal. Instead of crypto becoming a more regular investment like stocks, the stonks* had turned into shitcoins.**

What isn’t clear is how much of this money found its way to the crypto market. At least some of it did. A study by the Federal Reserve Bank of Cleveland noted: “a significant increase in Bitcoin buy trades for the modal EIP amount of $1,200.” This increased BTC-USD trade volume by 3.8%! [Cleveland Fed]

But the trades only seemed to raise the price of bitcoin by 0.07%. And the dollars in question were only 0.02% of the money distributed in the EIP program.

* A cheap and nasty equity stock; the term comes from a meme image. [Know Your Meme]

** We are sorry to tell you that this is literally a technical term in crypto trading.

The final push over the line

A lot of channels into crypto were put into place in 2020. But the last step was to pump the price over the previous bubble peak of $20,000.

With that bitcoin number achieved, the press would cover the number going up — because “number go up” is the most interesting possible story in finance. That would lure in the precious retail dollars that hodlers needed to cash out.

The push started in late November, with deployments of tethers to the offshore exchanges. On December 18, 2020 — exactly three years after the previous high — bitcoin went over $20,000 again. And that’s when a year and a half of fun started.

The federal reserve did not issue the stimulus.

The Federal Reserve’s stimulus program. Your stimulus checks were issued by the IRS.

What a great recent history lesson. Your recent Twitter Spaces dismantling of Carol was pretty awesome btw, thanks for putting in so much great work!