Ernst and Young (EY), the court-appointed monitor in Quadriga’s Companies’ Creditor Arrangement Act (CCAA), has filed its third report in Nova Scotia Supreme Court.

The defunct crypto exchange was holding $250 million CAD ($190 million USD) in crypto and fiat at the time it went bust. EY has been trying to track down any recoverable funds—and it’s not finding much.

The majority of the recoverable money will likely come from Quadriga’s third-party payment processors. The monitor has written to 10 known payment processors requesting they hand over any funds they are holding on behalf of Quadriga. (Previously, EY identified nine payment processors. Now it has added one more, though it does not reveal the name.) Here is the grim news: since its last report filed on February 20, EY has only recovered an additional $5,000 CAD ($3,800 USD) from the payment processors.

This is in addition to the $30 million CAD ($23 million USD) EY has already recovered from the two payment processors Billerfy/Costodian and 1009926 B.C. Ltd.

More money is out there, but getting at it may be tough. As I wrote earlier, WB21 is sitting on $12 million CAD ($9 million USD), which it is refusing to relinquish. EY notes that “further relief from the court may be necessary to secure funds and records from certain of the third party processors.”

So negligent was Quadriga in its bookkeeping that it appears to have lost track of some of its money altogether. EY located a Quadriga bank account at the Canadian credit union containing $245,000 CAD ($184,000 USD). The account had been frozen since 2017.

EY also reached out to 14 other crypto exchanges looking for accounts that may have been opened by Quadriga or its dead CEO Gerald Cotten. EY did not name any of the exchanges, but four replied. One of them was holding a small amount of crypto on behalf of Quadriga, which it has handed over to EY.

I don’t know this for sure, but it is possible the exchange that returned the funds may have been Kraken.

We have thousands of wallet addresses known to belong to @QuadrigaCoinEx and are investigating the bizarre and, frankly, unbelievable story of the founder's death and lost keys. I'm not normally calling for subpoenas but if @rcmpgrcpolice are looking in to this, contact @krakenfx

[Update: I was wrong. Kraken CEO Jesse Powell says, “Nothing recovered from Kraken. So far, we have not discovered any accounts/funds believed to belong to Quadriga.”]

Two thirds of the customer funds ($180 million CAD or $136 million USD) that Quadriga held at the time of its collapse were said have been in the form of crypto located in cold, or offline, wallets that only the exchange’s dead CEO had access to. However, it is looking more and more like those funds may have never existed.

EY identified six cold wallet addresses that Quadriga used to store bitcoin in the past. Other than the sixth wallet, there have been no deposits into the identified bitcoin cold wallets since April 2018, except for the 104 bitcoin inadvertently transferred to one of them from Quadriga’s hot wallet on February 6, 2019.

Post April 2018, the sixth wallet appears to have been used to receive bitcoin from another crypto exchange account and subsequently transfer the bitcoin to the Quadriga hot wallet. The sixth wallet is currently empty. The last transaction from the sixth wallet was initiated on December 3, 2018, days before Cotten died.

The monitor also identified three other potential Quadriga cold wallet addresses used to store cryptocurrency, but provided no detail.

Quadriga apparently created 14 fake accounts on its own exchange for trading fake funds. Deposits into some of the accounts “may have been artificially created and subsequently used for trading” on the platform, the report said.

"The Monitor was further advised that deposits into certain of the Identified Accounts may have been artificially created and subsequently used for trading on the Quadriga platform."

A few other items in the monitor’s report caught my attention.

Quadriga’s platform data is stored in the cloud on Amazon Web Services (AWS). But because the account was in Cotten’s personal name and not the company’s, EY is seeking a court order to authorize access. Here is where that gets weird: EY notes that there is possibly another AWS account in the name of Jose Reyes, the principal of Billerfy. Why would a payment processor need access to Quadriga’s transaction data?

Also buried in the monitor’s report are signs EY may be getting frustrated in its dealings with Robertson and her stepfather Tom Beazley. They are the only two directors left at Quadriga. A third director, Jack Martel, resigned last month.

Recall that in her second affidavit, Robertson sought the appointment of a chief restructuring officer (CRO) for Quadriga. EY states that it “continues to see some benefit” of having someone independent of Robertson and Beazley making decisions at Quadriga.

The wording is careful, but the report goes on to say that in order for EY’s investigation “to proceed appropriately, without any conflict or appearance of any conflict,” EY needs to communicate with Quadriga “in an appropriate manner and at an appropriate time.”

Finally, less than one month in, the cost of Quadriga’s CCAA procedures now sits at $410,000 CAD ($309,000 USD).

A “bitcoin friendly” payment processor with a reputation for accepting bank wires and not actually processing them, is allegedly sitting on $12 million CAD ($9 million USD) of Quadriga funds.

WB21 is not showing any sign of wanting to hand over those funds either. That has some Quadriga creditors worried that more of their money has vaporized.

When Quadriga, the largest crypto exchange in Canada, went belly up earlier this year, it owed its customers $250 million CAD ($190 million USD). Two thirds of those funds are in the form of cryptocurrency stuck in cold wallets that only the company’s dead CEO Gerald Cotten held the keys to.

Meanwhile, Ernst & Young, the court-appointed monitor in Quadriga’s Companies’ Creditors Arrangement Act, is trying to round up any funds that remain. EY has contacted nine third-party payment processors that may be holding money on behalf of Quadriga. Two of them, Billerfy/Costodian and 1009926 BC LTD, are in the process of signing over $30 million CAD ($23 million USD) to EY.

But according to an affidavit filed by Cotten’s widow Jennifer Robertson on January 31, WB21 has another $9 million CAD and $2.4 million USD “but is refusing to to release the funds or respond to communications from Quadriga.”

After this story was published, Amish Patel, WB21’s global head of litigation, told me in an email that the balances stated by Robertson “are not confirmed,” and that the account is “under investigation.” Patel also accused me of defamation and threatened me with legal action if I did not make several updates to this story.

WB21 stands for “web bank 21st century.” Launched in Switzerland in late 2015, the company touts itself as a virtual bank that lets you “streamline” opening up a bank account from 180 countries. But it is really a payment processor with a shady past that Quadriga got involved with—another shady business partner, what are the odds?

In June 2016, WB21 announced that it was accepting bitcoin deposits. Send in your bitcoin, and WB21 will credit your account in fiat—though it relies on payment service BitPay to convert the bitcoin to fiat. “The funds are instantly available on the account and can be sent out by wire transfers or spent with a WB21 debit card,” WB21 says.

The startup went on to launch a PR campaign that consisted of mainly, well, making stuff up. After 10 months of doing business, WB21 claimed it had 1 million customers and that it had sent cross-border payments totaling more than $5.2 billion.

Those number don’t really add up, especially when you consider it took Transferwise, one of the biggest London-based fintech companies, four years to get a comparable $4.5 billion in transfer money. Also, as Gruenderszene points out, in September 2016, WB21’s official app had only 100 downloads on Google’s Play Store.

In defense, WB21 CEO Michael Gastauer told Gruenderszene that WB21 doesn’t rely on its mobile app. A few hours after the conversation, Gruenderszene noted that the app disappeared from the store.

Boasting a $2.2 billion valuation, WB21 also claimed that Gastauer sold Apax Group, a previous payments business, for $480 million, and that WB21 turned down a $50 million funding round after Gastauer invested $24 million of his own money. Kadhim Shubber at the Financial Times did some digging and found no evidence of Apax being sold.

Yet Forbes (wait, did Forbes pull that story? Try this link), The Huffington Post and Business Insider all wrote about WB21’s incredible success. Though to its credit, Business Insider later added it was “unable to independently verify these numbers.”

In late 2017, WB21 even got itself in the Wall Street Journal after announcing that it was moving its European head office from London to Berlin after the Brexit vote.

How did WB21, a company spewing so many questionable facts and figures, manage to get all this media coverage? Like another company that we’ve been hearing about lately, the payment processor leveraged the power of social media. WB21 has a Twitter account with 65,000, mostly fake, followers.

Gastauer, a man in his mid-40s who hails from Germany, also appears in an impressive Youtube video at a hitherto unheard of “Global Banking Award 2018” event in Frankfurt, where he apparently won the award. Dressed in a tux, with a fog machine in the background, he is seen in the video giving a speech on the future of banking. “How do you come up with an idea like this?,” he says in the video speaking of his business successes. “Do you wake up one morning thinking you want to revolutionize an 80 trillion dollar industry?”

But the truth has a way of catching up. In October 2018, the U.S. Securities and Exchange Commission revealed a civil lawsuit accusing Gastauer of aiding and abetting the fraudulent sale of $165 million USD worth of shares in microcap stocks.

“In reality, WB21 Group was not a registered bank, and Gastauer’s ‘solution’ was actually a circumvention of banking regulations designed to disguise his clients’ [ . . .] identities,” the SEC said.

As it turns out, this was not Gastauer’s first run in with authorities. Writing again for the Financial Times, Shubber notes:

“In 2010, [Gastauer] was given an 18-month suspended sentence by a court in Switzerland for commercial fraud and counterfeiting. Around the same time, a British gambling company sued him in London for allegedly taking millions of pounds from it. He had set up a payments processor, the company claimed, but kept the payments.”

Shubber goes on to comment:

“The story of Mr Gastauer is not just about alleged wrongdoing in the financial markets; it shows how an accused fraudster might sell himself and his fantastical story using the modern tools of the internet age.”

A Google search finds the Internet littered with WB21 customers claiming the company stole their money.

In August 2018, “bitcoinjack” wrote of WB21 on Reddit: “They will accept incoming funds and credit your account but you will never be able to get it out. They will lie about outgoing payments until you give up.”

Consumer review website Trustpilot has a long list of people complaining that WB21 has taken their money and gone silent.

Quadriga customers began having trouble with WB21 about a year ago. Several complained on Reddit that their bank wires were either not coming through or delayed. In response, Quadriga covered for WB21, blaming the delays on a bank in Poland that it was using:

“We used WB21 for about a week, but the vast majority of delays related to wires comes from the fact that the intermediary bank that handled CAD wires for the Polish bank cut them off due to the association with Bitcoin. We had to reissue all of these from other payment processors, all manually, which has caused delays.”

(This story was updated on March 5, 2019, to include a statement from WB21.)

The 104 bitcoin (worth $468,675 CAD) that Canadian crypto exchange QuadrigaCX “inadvertently” sent to its dead CEO’s cold wallets on February 6—a day after the company filed for creditor protection—was due to a “platform setting error.”

That and other news was included in Ernst & Young’s (EY’s) second report, released on February 20. EY is the court-appointed monitor in Quadriga’s Companies’ Creditors Arrangement Act (CCAA). At least now we know that the bitcoin wasn’t sent by somebody clumsily pushing a wrong button. Still, that single automation wiped out more than half of Quadriga’s hot wallet funds.

The rest of the hot wallet funds, worth $434,068 CAD, are now safe from Quadriga. On February 14, EY transferred the coins into cold wallets that it controls. The funds include 51 bitcoin, 33 bitcoin cash, 2,032 bitcoin gold, 822 litecoin, and 951 ether. But all of this is a mere drop in the bucket compared to the $250 million CAD owed to Quadriga’s 115,000 creditors—most of which is presumably lost forever.

Also in the report: Recall that Quadriga elected a new board following the death of its CEO Gerald Cotten on December 9. The new directors included Cotten’s widow Jennifer Robertson, her stepfather Thomas Beazley and a man named Jack Martel, who nobody knew too much about. Apparently, Martel stepped down on February 11.

And more money is needed to fund Quadriga’s CCAA process. EY and Quadriga’s law firm Stewart McKelvey have already burned through the nearly $300,000 CAD Robertson put up to initiate the process in January.

Additional money for the CCAA process—and ultimately for Quadriga’s creditors—will come from Quadriga’s payment processors, once they hand the money over to EY in the form of bank drafts. EY also has to get a bank to agree to accept the bank drafts, which is not an easy thing to do. Most banks want nothing to do with Quadriga’s money.

Costodian, a company created by payment processor Billerfy specifically to manage Quadriga’s funds, is holding $26 million CAD in bank drafts. After the Canadian Imperial Bank of Commerce froze those funds in January 2018, the Ontario Superior Court of Justice took control of that money, and in December, released the funds back to Costodian in the form of bank drafts issued by the Bank of Montreal (BOM).

According to EY, Costodian has so far handed over four BOM bank drafts totaling $20 million CAD. But it is waiting for a court order before releasing two more bank drafts.

One of those is for roughly $70,000 USD. These are personal funds belonging to Costodian’s principal Jose Reyes. EY has determined that those funds do indeed belong to Reyes, but he still needs to sign the check over to EY for disbursement.

The other BOM bank draft in question is for $5 million CAD. Of that amount, Custodian claims that $61,000 CAD also represent Reyes’ personal funds, and that $778,000 CAD is due to Custodian for unpaid processing fees.

Quadriga creditors don’t agree that Costodian should be paid these fees. To resolve the issue, EY notes that “a separate dispute resolution mechanism will be required during the course of these CCAA proceedings.”

In addition, Stewart McKelvey is holding 1,004 in bulk drafts totaling $6 million. These drafts were issued to 1009926 BC LTD, a payment processor run by a former Quadriga contractor. The problem is 1009926 BC LTD was dissolved in January 2018 for failure to file an annual report, so EY is looking to potentially restore the company.

EY is currently negotiating with the Royal Bank of Canada (RBC), where it hopes to deposit most of these checks. RBC is proceeding with caution, however.

According to EY, “a stranger to the CCAA proceedings, RBC has expressed hesitation to accept and disburse the BMO drafts, bulk drafts and future amounts, without direction and relief from the court.”

A hearing is scheduled for February 22 to give direction to the banks and to the third-party payment processors, so the funds can be freed up.

After that, another hearing to extend the stay of the CCAA proceedings is scheduled for March 5 in Halifax, where angry Quadriga creditors are looking to stage a protest. The protesters are urging the court to discontinue the CCAA proceedings and launch a criminal probe into Quadriga.

Update (February 21, 12:30 ET): I made some changes to clarify the amount of personal funds that Custodian principal Jose Reyes claims belong to him in two BOM bank drafts.

Nova Scotia Supreme Court Judge Michael Wood appointed law firms Miller Thomson and Cox & Palmer to represent the more than 115,000 Quadriga creditors, who are owed a total of $250 million CAD. Most of that money— $180.5 million CAD—is stuck in cold wallets after the company’s CEO died in India. He was the only one who held the keys.

To offer some background, a CCAA is a federal law in Canada that gives insolvent companies, such as Quadriga, time to restructure themselves and come up with a so-called plan of arrangement. It is not quite like a bankruptcy. A company can still operate and pay its employees during the proceedings.

When Quadriga was granted creditor protection on February 5, the judge issued a 30-day stay, to keep any lawsuits at bay. The court also appointed Ernst & Young as a monitor to oversee Quadriga’s business and help Quadriga put together its plan of arrangement.

If that plan is accepted by the court and the creditors, Quadriga users will likely be able to recoup some of their losses more expediently. If the plan is rejected, the stay will be lifted, and creditors can forge ahead with their lawsuits.

In the case of Quadriga, because there are so many creditors, the court felt it appropriate to find them legal representation. Three teams of lawyer vied for that position on February 12. Justice Wood reviewed their credentials and made his final decision today.

In his ruling, he explained that he chose Miller Thompson/Cox & Palmer because both firms have extensive insolvency experience. In the coming weeks, Cox and Palmer, which has an office in Halifax, will take the lead on the civil procedure and court appearances, while Miller Thompson, which is headquartered in Toronto, will handle “project management, communication and cryptocurrencies.”

The judge noted in his ruling that the firms’ proposal was “thought out carefully with a view to minimizing costs.” The team proposed an initial $250,000 cap on fees. They also said that they would communicate with creditors via social media, and that they would advocate for user privacy, something Quadriga users indicated was important to them.

Appointing a representative counsel and a stakeholder representative committee in complex CCAA proceedings is not unusual, the judge said. Such measures are usually undertaken when the group of stakeholders is large and without representation, many of them would struggle to effectively participate in the CCAA proceedings.

He also agreed with Quadriga’s lawyer Maurice Chiasson and others that assembling a committee of users to represent the broader group of creditors was something that needed to happen quickly.

“The anecdotal evidence at the hearing is that many people are extremely upset, angry and concerned about dishonest and fraudulent activity,” he wrote. “There are reports of death threats being made to people associated with the applicants. All parties agree that this user group needs representation as soon as possible.”

Quadriga’s stay of proceedings expires on March 7. A hearing is planned for March 5 to update the court on what progress Quadriga and its monitor Ernst & Young have made.

Update: According to an email Ernst & Young sent to creditors, Quadriga will, in fact, seek to extend the stay of proceedings. The monitor writes that “the stay of proceedings may be extended for any period that the Court deems appropriate. There is no standard timeframe for the completion of proceedings under the CCAA.”

Ernst & Young is posting updates to the CCAA proceedings on its website.

The news keeps getting worse for QuadrigaCX creditors. The Canadian crypto exchange has apparently jettisoned another $468,675 CAD worth of bitcoin into deep space.

On Feb. 6, literally, one day after Quadriga applied for creditor protection, the exchange “inadvertently” sent 104 BTC to its dead CEO’s cold wallet, according to an initial report released by court-appointed monitor Ernst & Young.

When Quadriga CEO Gerald Cotten died in India on Dec. 9, he carried into the afterlife with him the keys to the exchange’s cold wallets, where $180 million CAD—now $180.5 million CAD—worth of crypto is stored. Unless Cotten springs from the grave, any crypto in those wallets is as good as gone.

You have to scratch your head till it bleeds on that one. Why was anyone at Quadriga allowed to touch those coins after the company applied for creditor protection? EY is now moving to safeguard the remaining crypto, a stash now down to 51 bitcoin, 33 bitcoin cash, 2,032 bitcoin gold, 822 litecoin, and 951 ether, worth a current value of $434,068 CAD. Basically, more than half the money in the hot wallets is now gone.

EY is also working to retrieve about $30 million worth of cash from nine Quadriga payment processors. So far, EY has yet to collect a dime, and one of the processors is stubbornly insisting that “it has the right to continue to hold funds in its possession pursuant to the terms of its agreement with the Applicants.”

Which payment processor would that be then? How about WB21? According to Robertson’s affidavit filed on Jan. 31, WB21 is holding roughly $9 million CAD and $2.4 million USD of the exchange’s money. Even before EY took over, WB21 was “refusing to release the funds or respond to communications from Quadriga.”

A quick Google search reveals that WB21 has long been plagued by accusations that it is a scam. A year ago, Quadriga customers were complaining on Reddit that they were having trouble getting their wires from WB21. And it also turns out, the U.S. Securities and Exchange Commission is suing WB21’s CEO for fraud. (You can find the full SEC complaint here.)

Creditors need their own lawyer

Quadriga’s 115,000 creditors need proper representation. On Feb. 14, three legal teams appeared in court to vie for the position of representative counsel. Nova Scotia Supreme Court Judge Michael Wood said he plans to have a final decision next week.

All this legal stuff is getting expensive. So far, Robertson has put up $250,000 CAD of the $300,000 CAD she promised in her affidavit to fund the CCAA process. And the funds are being gobbled up quick. Quadriga’s lawyer Maurice Chiasson said the money will run out in two weeks, if not sooner.

Chiasson: Jennifer Robertson has put in 250-thousand of the 300-thousand she’s promised to fund this process so far. But that money will run out in the next 2 weeks if not sooner.

After that, where will the money come from? Likely, out of whatever funds EY pulls from those nine payment processors.

Meanwhile, more funny business is starting to surface. In her sworn affidavit, Cotten’s widow stated that she had no dealings with Quadriga prior to Cotten’s death. Yet, three Quadriga creditors (archive) claim they received wires from Robertson’s real estate company, Robertson Nova Property Inc.

The wire transactions occurred in 2016 and 2017. This is interesting, given Jennifer only changed her name to Robertson in April 2017.

Cash delivered to your door

Did you know that if you wanted to cash out of Quadriga, you could opt to have actual boxes of cash dropped off at your door? That was an actual service Quadriga offered its customers. A few have suggested that the money may have come from bitcoin ATM machines that Quadriga operated.

I've been hearing more and more about @QuadrigaCoinEx users receiving significant withdrawals in the form of cash in nondescript packages by Canada Post. AFAIK, cash deposits were not an option. Why did Quadriga have so much cash on hand? @Bitfinexed#QuadrigaCX#seaglasstrust

Remember, Quadriga had no corporate banking. That is why, when you sold bitcoin for cash on the exchange or wired in money via one of Quadriga’s payment processors, your online wallet was credited with QuadrigaCX Bucks—not real bucks.

But who knew? I’ve been speaking to Quadriga creditors and some of them had no clue that the “CAD” they saw in their online wallets was basically Quad Bucks.

“Everyone knows CAD equals Quad bucks now, but I didn’t know that until after the implosion,” one creditor who preferred to remain anonymous told me. “I guess it was in the terms [and conditions], but it wasn’t marked Quad bucks.”

Some traders also told me that bitcoin sold for a premium on Quadriga. That meant, you could buy bitcoin on another exchange, such as Kraken, and then sell it for a profit on Quadriga. As an added incentive to move your crypto onto the exchange, Quadriga also offered free cash withdrawals, as long as you did not mind waiting two weeks or so for the money to hit your bank account. You had to pay a fee for express withdrawals.

Gerry Bot was pushing the price up on quad for YEARS! It was a giant carrot luring in new ignorant money into depositing BTC!

Finally, the Globe and Mail sent its investigative reporters to India, where Cotten and his wife celebrated their honeymoon just before Cotten died. People are still wondering if his death was staged. “That Mr. Cotten did indeed die is a certainty among police and medical professionals in India, and The Globe reviewed hotel, hospital and embalming records that give no suggestion of anything abnormal,” the Globe writes.

But why was Cotten’s body taken from the hospital where he died back to the hotel where he had been staying? (According to Cotten’s death certificate, Fortis Escorts Hospital was the place of death.) Partly because of this, Simmi Mehra, who works at Mahatma Gandhi Medical College & Hospital, refused to embalm the body.

She told The Globe: “That guy [a representative from the hotel] told me the body will come from the hotel. I said: ‘Why the hotel? I’m not taking any body from the hotel, it should come from Fortis.”

The Globe and Mail report also reveals tragic details of the oft-overlooked Angel House orphanage that Cotten and Robertson sponsored. Apparently, the money they donated only paid for building materials. Several doors are still missing from the structure, including one to the toilet. And the operator of the orphanage is sinking into debt.

The orphanage appears to be yet another example of the wake of destruction that Cotten, who otherwise lived as though money were no object, carelessly left in his passing.

QuadrigaCX customers’ worst fears have come to pass. The Canadian exchange is officially insolvent, and all the crypto is gone—well, most of it anyway.

On January 31, after filing for creditor protection, Jennifer Robertson, the widow of the exchange’s now-deceased CEO Gerald Cotten, filed an affidavit with the Supreme Court of Nova Scotia. As it turns out, Cotten was the only person who held the keys to the exchange’s cold wallets—encrypted wallets where cryptocurrency is kept offline. When he died in December, all that crypto became inaccessible.

According to the affidavit, QuadrigaCX owes 115,000 customers some $250 million CAD ($190 million USD) in both crypto and fiat. Roughly $192 million CAD ($147 million USD) were in crypto assets, most of it in the cold wallets.

So let me get this straight:

No one knows the cold wallet addresses for Quadriga or if they even exist?

In addition to the lost crypto, $30 million CAD is currently held by payment processor Billerfy. Three other third-party payment processors are holding a combined $565,000 CAD. And another $9.2 million USD is stuck inside WB21—a money transfer service that, surprise, surprise, is being sued by the U.S. Securities and Exchange Commission (SEC) for fraud.

But here is where things get strange. Two weeks before he died, Cotten signed a will leaving $100,000 CAD for his two dogs, according to the Globe and Mail (archive.)

I’m not insinuating any foul play here, but let’s go over what we have: Cotten and Robertson supposedly got married two months before his death. Cotten writes up a will to make sure his dogs are taken care of and Robertson takes ownership of 43% of the shares of Quadriga Fintech Solutions, the parent company of QuadrigaCX, should anything awful happen to him. Once that’s all said and done, something awful happens. Cotten goes off to India to help needy children (so nice of him) and dies.

A month later, Robertson posts an announcement on the exchange’s website telling everyone the company’s CEO is dead. He was a kind, honest, upstanding, guy…after all, he sponsored an orphanage. And then later: Oh, and by the way, all the money is gone, because only Gerald knows where he put it.

[Update: A new twist to this plot may be developing. One Reddit user claims to have found the QuadrigaCX litecoin cold wallet addresses—and the funds appear to be on the move.]

Elsewhere in the news, Canadian social media startup Kik plans to fight an expected SEC enforcement action over an initial coin offering (ICO). (Read my coverage here.) Kik raised $100 million in 2017 by selling its kin token. In a response to a Wells notice from the SEC, Kik argues that its token is a currency, therefore, it cannot be a security, and besides, the company never marketed kin as an investment anyway.

You could almost go along with that, as long as you completely ignored this 2017 Youtube video of Kik’s CEO Ted Livingston telling everyone how rich they could become if they owned kin. “We’re gonna put [kin] inside Kik and it will become super valuable on day one, we think.” Oops! (Read the full coverage in The Block.)

Two “professional hacking groups” are behind the majority of publicly reported hacks of crypto exchanges and other cryptocurrency organizations, according to a crypto crime report published by blockchain data analytics firm Chainalysis. The two nefarious groups so far have raked in $1 billion of hacking revenues for themselves. Of course, even thieves don’t keep their holdings in bitcoin. They converted everything to fiat.

If you thought SingularDTV was a dreadful name, the blockchain entertainment company has come up with something even more bad. SingularDTV has changed its name to Breaker. The company has a new logo, too—a circle comprised of small lines swirling inward meant to represent the “the hive mind,” a type of groupthink that decentralized projects like to associate themselves with.

Breaker owns Breaker Magazine, which changed its name to BreakerMag to avoid confusion. To go along with the new branding, Breaker (we’re talking about SinglarDTV now) also released a cringe-worthy video that starts with a man gyrating his hips and saying, “It’s like this,” and then devolves into a woman ripping a pink beauty mask off her face. As if the name change wasn’t awkward enough.

Nicholas Weaver, a researcher at International Computer Science Institute, gave a talk at Enigma, a USENIX conference, called “Cryptocurrency: Burn it with Fire!,” where he argued the entire cryptocurrency and blockchain space is effectively one big fraud. Here are the slides to the presentation. The video is not up yet, but Weaver gave a similar talk in April 2018. (It’s funny, watch it.)

For a brief period, tether (USDT), the stablecoin associated with the crypto exchange Bitfinex, rose to become the fourth largest crypto by market cap at $2 billion. It has dropped back down to sixth place now, but who knows, maybe it will rise up again. (Read my tether timeline to learn why tether is so important to crypto markets.)

Banking giant JP Morgan says bitcoin is now worth less than the cost to mine it. “The drop in Bitcoin prices from around $6,500 throughout much of October to below $4,000 now has increasingly pushed margins further and further negative for just about every region except low-cost Chinese miners,” the bank’s analysts said. (Bloomberg)

Despite all the hype, decentralized exchanges (DEX) are not attracting much interest. According to a report in Diar, DEX volume is at an all-time low—something that’s unlikely to change, mainly due to poor usability issues. Another reason to avoid DEXs: anyone can list any token they like—even if it’s not a legitimate one.

the things u cld do with a fake ERC-20 token: – show as "collateral" or proof of reserves – sell on DEX to redeem for real $ETH – trade on your own exchange to pump your volume #'s (harder than 1, 2)

Binance has come up with yet another harebrained business scheme. The Malta-based crypto exchange now allows customers to buy crypto using their credit cards. I can’t see this working out too well. Banks generally distance themselves from all things crypto, and many won’t allow you to put crypto on credit cards. And even if they do, weird things happen. US-based crypto exchange Coinbase no longer accepts credit cards, but when it did, Visa actually overcharged buyers—though, it did eventually issue refunds.

An Italian bankruptcy court found Francisco Firano (aka “Francisco the Bomber”) personally liable for $170 million in losses related to the BitGrail hack in April 2018. (Last year, I wrote a story about the hack for Bitcoin Magazine.) The BitGrail Victims Group posted scans of the court documents along with an explanation of the court’s decision on Medium.

In a big win for nocoiners, David Gerard, author of “Attack of the 50-foot Blockchain,” wrote a op-ed for The Block titled “The Buttcoin Standard: the problem with Bitcoin,” where he basically takes apart bitcoin and criticizes the horrendous energy waste of proof of work. Gerard’s article was solid. But just as you might expect, bitcoiners objected en masse, and even attackedThe Block cofounder Mike Dudas.

seriously – weirdest response so far from bitcoiners has been "but he didn't touch on the *serious* issues" … and a glaring failure to list these serious criticisms.

Apple cofounder Steve Wozniak, who used to go around comparing bitcoin to digital gold, admits he sold all his bitcoin at its peak. “When it shot up high, I said I don’t want to be one of those people who watches and watches it and cares about the number. I don’t want that kind of care in my life,” he said at the Nordic Business Forum. “Part of my happiness is not to have worries, so I sold it all and just got rid of it.” (Satoshi Times)

And finally, the police department in Lawrence, Kansas has been getting reports of bad actors calling people up at random to demand bitcoin.

Someone is calling people and pretending to be one of our sergeants and demanding bitcoin. First of all, no, second of all, just call him whatever names and profanities you want, then hang up. It’s not from us, pinky promise.

I originally wrote this article in January 2019. It is based off an earlier story that I wrote for Bitcoin Magazine in February 2018.

This timeline only goes up until May 2021; however, it documents all of the early shenanigans of Bitfinex and Tether.

Stablecoins—virtual currencies pegged to another asset, usually, the U.S. dollar—bring liquidity to crypto exchanges, especially those that lack ties to traditional banking. Putting it simply, if you are a crypto exchange and you don’t have access to real dollars, stablecoins are the next best thing.

Today, there are several stablecoins to choose from. But by far the most popular and widely traded is tether (USDT), issued by a company of the same name. Of the three or four main stablecoin models, Tether follows the I.O.U. model, where virtual coins are supposed to represent actual money and be redeemable at any time. It all sounds well and good, but for one thing: There is no evidence to suggest Tether is fully backed.

Currently, there are 1.9 billion tethers in circulation.* That means, there should be a corresponding $1.9 billion tucked away in one or more bank accounts somewhere. Bitfinex, the crypto exchange closely linked to Tether, claims the money exists, but has yet to provide an official audit to support those claims. (We have seen snapshots of bank account balances at certain points in time, but these are not full audits.)

*As of May 2025, there are 149 billion tethers in circulation, according to Tether’s Transparency page.

More troubling, the issuance of tethers correlates with the rapid run up in price of bitcoin from April to December 2017 when bitcoin peaked at nearly $20,000. If authorities were to step in and freeze the bank accounts underlying tether, it is hard to guess what impact that could have on crypto markets at large.

A timeline of events reveals a full picture of the controversy surrounding Tether and Bitfinex.

Timeline

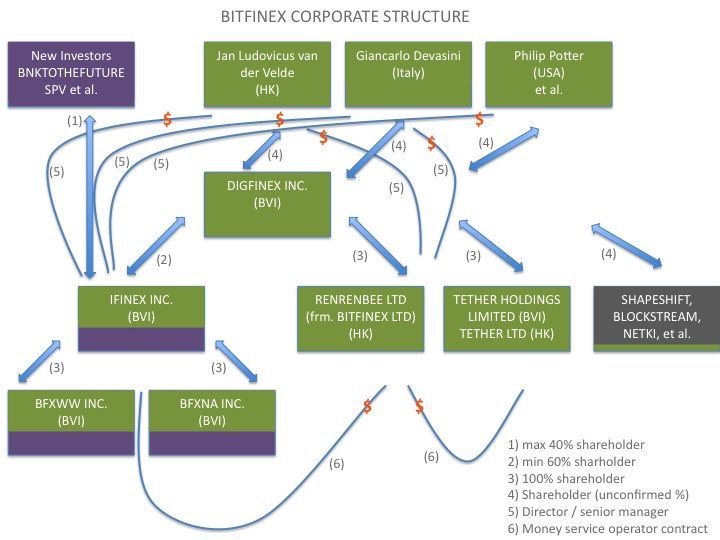

2012 — iFinex Inc., the company that is to become the parent company of Bitfinex and Tether, is founded in Hong Kong. (Like its parent company DigFinex, iFinex is registered in the British Virgin Islands. An org chart from NY AG court filings is here.)

2013 — Bitfinex incorporates in Hong Kong. The cryptocurrency exchange is run by the triad: Chief Strategy Officer Phil Potter, CEO Jan Ludovicus van der Velde and CFO Giancarlo Devasini.

July 9, 2014— Brock Pierce, Bitcoin Foundation director and former Disney child actor, launches Realcoin, a dollar-backed stablecoin. Realcoin is built on a Bitcoin second-layer protocol called Mastercoin, now Omni. Pierce was one of the founding members of the Mastercoin Foundation before resigning in July 2014. He founded Realcoin along with Mastercoin CTO Craig Sellars and ad-industry entrepreneur Reeve Collins. (Wall Street Journal)

September 5, 2014—Appleby, an offshore law firm, assists Bitfinex operators Potter and Devasini in setting up Tether Holdings Limited in the British Virgin Islands, according to the Paradise Papers. (Offshore Leaks Database)

September 8, 2014 — Tether Limited registers in Hong Kong.

October 6, 2014 — The very first tethers are minted, according to the Omni block explorer.

November 20, 2014 — Realcoin rebrands as “Tether” and officially launches in private beta. The company hides its full relationship with Bitfinex. A press release lists Bitfinex as a “partner.” In explaining the name change, project co-founder Reeve Collins tells CoinDesk the firm wanted to avoid association with altcoins.

January 15, 2015 — Bitfinex enables trading of tether on their platform.* (Bitfinex blog.Archive.)

May 18, 2015 — Tether issues 200,000 tethers, bringing the total supply to 450,000.

May 22, 2015— Bitfinex is hit with its first hack. The exchange claims it lost 1,500 bitcoin (worth $400,000 at the time) when its hot wallets were breached. The amount represents 0.05 percent of the company’s total holdings. Bitfinex says it will absorb the losses.

December 1, 2015 — Tether issues 500,000 USDT, bringing the total supply to 950,000. (The price of bitcoin has remained stable throughout most of 2015, but climbs from $250 in October to about $460 in December.)

June 2, 2016— The U.S. Commodity Futures Trading Commission fines Bitfinex $75,000 for offering illegal off-exchange financed retail commodity transactions in bitcoin and other cryptocurrencies and for failing to register as a futures commission merchant as required by the Commodity Exchange Act. In response, Bitfinex moves its crypto funds from an omnibus account to multisignature wallets protected by BitGo.

August 2, 2016 —Bitfinex claims it has been hacked again when 119,756 BTC, worth $72 million at the time, vanish. This is one of the largest hacks in bitcoin’s history, second only to Mt. Gox, a Tokyo exchange that lost 650,000 BTC in 2014. Bitfinex never reveals the full details of the breach. (Chapter 8 of David Gerard’s book “Attack of the 50-Foot Blockchain” offers an in-depth explanation of the hack.)

August 6, 2016— Bitfinex is unable to absorb the losses of the hack. The exchange announces a 36% haircut across the board for its customers. It even takes funds from those who were not holding any bitcoin at the time of the hack. In return, customers receive an I.O.U. in the form of BFX tokens, valued at $1 each.

One large U.S. customer reportedly didn’t get the full haircut. “Coinbase, got a better deal after threatening to sue, multiple sources told me,” said NYT’s Nathaniel Popper.

One point that didn't fit in the story: After getting hacked in 2016, Bitfinex said it gave every customer a 36% haircut to cover losses. But at least one customer, Coinbase, got a better deal after threatening to sue, multiple sources told me.

August 10, 2016 — After having been shut down for a week after the heist, Bitfinex resumes trading and withdrawals on its platform. Meanwhile, Zane Tacket, the exchange’s community director, announces on Reddit (archive) that Bitfinex is offering a bounty of 5% (worth up to $3.6 million) for any information leading to the recovery of the stolen funds.

August 17, 2016— Bitfinex announces it is engaging Ledger Labs, a blockchain forensic firm founded by Ethereum creator Vitalik Buterin, to investigate its recent breach. Bitfinex hires Ledger to do a computer security audit, but leads customers into believing that Ledger is also going to perform a financial audit. A financial audit is key to knowing whether Bitfinex was even solvent at the time of the hack.

“We are also in the process of engaging Ledger Labs to perform an audit of our complete balance sheet for both cryptocurrency and fiat assets and liabilities,” Bitfinex says in a blog post (archive).

A footnote added to the blog post on April 5, 2017, makes a correction: “Ledger Labs has not been engaged to perform a financial audit of Bitfinex. When in initial discussions with Ledger Labs in August 2016, we had initially understood that they could offer this service to us.” The exchange goes on to say that it is in the process of engaging a third-party accounting firm to audit its balance sheet.

This audit, as we are to learn, never happens.

October 12, 2016 — Bitfinex tries to reach out to the hacker. In a blog post (archive), titled “Message to the individual responsible for the Bitfinex security incident of August 2, 2016,” the firm writes: “We would like to have the opportunity to securely communicate with you. It might be possible to reach a mutually agreeable arrangement in exchange for an enormous bug bounty.”

October 13, 2016 — Bitfinex announces (archive) that its largest BFX token holders have agreed to exchange over 20 million BFX tokens for equity shares of iFinex, the exchange’s parent company. Many Bitfinex customers accept the offer, having already watched BFX tokens drop far below $1. One Redditor even reported the price dropping to $0.30.

As a way to incentivize BFX holders to convert, Bitfinex creates yet another new token: a tradable Recovery Rights Token (RRT). According to the exchange, if any of the stolen bitcoins are recovered, any excess of funds after all BFX tokens have been redeemed will be distributed to RRT token holders.

If you convert your BFX to iFinex shares before October 7, you get one RRT for each BFX token converted. If you convert between Oct. 8 and Nov. 1, you get half an RRT for each BFX token converted. After that, you get 1/4 of an RRT per BFX token converted. No further RTTs are given after November 30.

December 31, 2016 — In 2016, Tether issued 6 million USDT, six times what it issued the prior year.

March 31, 2017— Correspondent bank Wells Fargo cuts off services to Bitfinex and Tether, according to court documents in a lawsuit that Bitfinex later files. Bitfinex is not a direct customer of Wells Fargo, but rather a customer of four Taiwan-based banks that use Wells Fargo as an intermediate to facilitate wire transfers.

April 3, 2017 — In a blog post(archive), Bitfinex announces plans to redeem any outstanding BFX tokens. “After these redemptions, no BFX tokens will remain outstanding; they will all be destroyed.”

Meanwhile, Potter reveals in an audio that all of the remaining BFX tokens have been converted to tethers. In a nutshell, this means that none of the victims of the August 2016 Bitfinex hack got back any of their original funds—they were all compensated with BFX tokens, RRT tokens and USDT.

April 5, 2017 — Two days after announcing that it had “paid off” all its debt to customers, Bitfinex, via law firm Steptoe & Johnson, files a lawsuit against Wells Fargo for interrupting its wire transfers. Tether Limited is listed as a plaintiff. In addition to an injunction order, Bitfinex seeks more than $75,000 in damages. (See here for a complete list of documents associated with the lawsuit.)

April 10, 2017— A pseudonymous character known as “Bitfinex’ed” debuts online. In a relentless series of tweets, he accuses Bitfinex of minting tethers out of thin air to pay off debts. At this point, the number of USDT in circulation is 55 million, and BTC’s price has begun a steep ascent that will continue to the end of the year.

April 11, 2017 — Bitfinex withdraws its lawsuit against Wells Fargo. In an audio, Potter admits the lawsuit was frivolous, stating the company was only hoping to “buy time.”

April 17, 2017 — Following a notice about wire delays, Bitfinex announces (archive) it has been shut off by its four main Taiwanese banks: Hwatai Commercial Bank, KGI Bank, First Commercial Bank, and Taishin Bank. Bitfinex is now left to shuffle money between a series of banks in other countries without telling its customers where it is keeping its reserves.

In an audio, Bitfinex CSO Phil Potter tries to calm customers by telling them that Bitfinex effectively deals with this sort of thing by setting up shell accounts and tricking banks.

“We’ve had banking hiccups in the past, we’ve just always been able to route around it or deal with it, open up new accounts, or what have you…shift to a new corporate entity, lots of cat and mouse tricks.”

Around this time, Bitfinex begins to rely increasingly upon Crypto Capital Corp, a Panamanian shadow bank, to shuffle funds around the globe—but it does not make this clear to customers. Also, Bitfinex never engages in a formal contract with Crypto Capital, according to later court documents.

April 24, 2017 — Amidst reports that Bitfinex has lost its banking, USDT temporarily dips to $0.91.

May 5, 2017— After finally clarifying (archive) to customers that it only engaged Ledger Labs for a security audit—not a financial audit—Bitfinex hires accounting firm Friedman LLP to complete a comprehensive balance sheet audit. “A third-party audit is important to all Bitfinex stakeholders, and we’re thrilled that Friedman will be helping us achieve this goal,” Bitfinex writes in a blog post (archive).

June 21, 2017 —The Omni foundation and Charlie Lee announce that tether will soon be issued on the Omni layer of Litecoin, but apparently it never panned out, according to Lee. (Omni Blog, archive)

"Tether will be issuing USDT on Omni on Litecoin 😀"

Launching tether (or anything) on Litecoin requires no approval or corporation from me. I was informed of their decision and I supported it. But I didn't do any work on it. Ultimately, it didn't pan out. I don't have inside info on tether.

August 5, 2017 — Bitfinex’ed publishes his first blog post titled: “Meet ‘Spoofy.’ How a Single Entity Dominates the Price of Bitcoin.” The post explains how an illegal form of market manipulation known as spoofing works. The post includes a video showing a Bitfinex trader putting up a large order of BTC just long enough to push up the price of bitcoin, before canceling the order.

(This is not the first time a crypto exchange has manipulated the price of bitcoin. Mt. Gox, a Tokyo exchange that handled 70% of all global bitcoin transactions before its 2014 collapse, also manipulated its markets. Former Mt. Gox CEO Mark Karpeles admitted in court to operating a “Willy Bot.” An academic paper titled “The Willy Report” shows how the bots were responsible for much of bitcoin’s 2013 price rise.)

September 11, 2017 — Tether announces they will begin making ERC-20 tokens for US dollars and euros on the Ethereum blockchain. (Ethfinex blog,archive)

September 15, 2017 —In the summer of 2017, rumors were afoot that tethers were not fully backed. To quash those rumors, Tether and Bitfinex arrange for accounting firm Friedman LLP to perform an attestation on September 15, 2017.

In the morning, Tether opens an account at Noble Bank. And Bitfinex transfers $382 million from Bitfinex’s account at Noble Bank into Tether’s account at Noble Bank. Friedman conducts its verification of Tether’s assets that evening.

“No one reviewing Tether’s representations would have reasonably understood that the $382,064,782 listed as cash reserves for tethers had only been placed in Tether’s account as of the very morning that Friedman verified the bank balance,” the NY attorney general wrote in its later findings.

The attestation included $61 million held at the Bank of Montreal in an a trust account controlled by Tether and Bitfinex’s general counsel Stuart Hoegner.

September 28, 2017 — Friedman LLP issues a report alleging that Tether’s U.S. dollar balances ($443 million) match the amount of tethers in circulation at the time. Falling far short of a full audit, the report does not disclose the names or locations of banks.

According to the report: “FLLP did not evaluate the terms of the above bank accounts and makes no representations about the Client’s ability to access funds from the accounts or whether the funds are committed for purposes other than Tether token redemptions.”

August 7, 2017 — In a blog post (archive), Bitfinex announces that over the next 90 days, it will gradually discontinue services to its U.S. customers. Effective almost immediately, U.S. citizens are no longer able to trade Ethereum-based ERC20 tokens, commonly associated with initial coin offerings.

The news follows regulatory crackdowns in the U.S. (The previous month, the U.S. Securities and Exchange Commission issued an investigative report that deemed that tokens issued by the DAO—an investor-directed fund built on top of Ethereum that crashed spectacularly in June 2016—were securities.)

November 7, 2017—Leaked documents dubbed “The Paradise Papers” reveal Bitfinex and Tether are run by the same individuals. Up until now, Tether and Bitfinex insisted the two operations were separate, though they were widely suspected to be the same.

November 19, 2017—Tether is hacked when 31 million USDT are moved from the Tether treasury wallet into an unauthorized Bitcoin address. Tether initiates a hard fork to prevent those funds from being spent.

After this hack, Tether notes on its website (archive) that redemption of USDT for real dollars is no longer possible via the Tether website. (It is worth noting that there is no public record of anyone having redeemed their USDT for dollars at any point before this either.)

“Until we are able to migrate to the new platform, the purchase or sale of Tether will not be possible directly through tether.to. For the time being, though, we invite you to use the services of any one of a dozen global exchanges to acquire or dispose of Tethers for either USD or other cryptocurrencies. Such exchanges and other qualified corporate customers can contact Tether directly to arrange for creation and redemption. Sadly, however, we cannot create or redeem tether for any U.S.-based customers at this time.”

From now until December 2018, tether purchases and redemptions can be made only from Bitfinex. (After December 2018, they switch back to tether.io.)

November 30, 2017 — Bitfinex hires 5W, a scrappy New-York public relations firm led by Ronn Torossian. 5W promptly issues a press release stating that an “audit” from Friedman LLP is forthcoming. The agency also tells journalists they can view Bitfinex’s bank accounts if they sign a non-disclosure agreement first. No journalist takes the bait. “We plan to release regular financial statements and are working with journalists who can review our finances as wel[l],” Torossian says in a tweet.

We plan to release regular financial statements and are working with journalists who can review our finances as wel

December 4, 2017— Bitfinex threatens legal action against its critics, according to Bitcoin Magazine. The exchange does not specify who those critics are but the obvious target is Bitfinex’ed, the cynical blogger who continues to accuse Bitfinex of manipulating markets and printing more tether than it can redeem. Bitfinex never actually sues Bitfinex’ed, though Bitfinex’ed collects donations and hires a lawyer just in case.

December 6, 2017— The CFTC subpoenas Bitfinex and Tether, Bloomberg reports. The actual documents are not made public.

December 16, 2017 — The price of bitcoin reaches an all-time high of nearly $20,000, marking the end of a spectacular run-up and bitcoin’s biggest bubble to date. A year before, BTC was only $780.

December 21, 2017 — Without any formal announcement, Bitfinex appears to suddenly close all new account registrations. Those trying to register for a new account are asked for a mysterious referral code but no referral code seems to exist.

December 31, 2017 — Tether has issued roughly $1.4 billion USDT to date.

January 3, 2018— A change to Tether’s legal terms of service (archive) states: “Beginning on January 1, 2018, Tether Tokens will no longer be issued to U.S. Persons.”

January 12, 2018 — After a month of being closed to new registrations, Bitfinex announces it is reopening its doors, but now requires new customers to deposit $10,000 in fiat or crypto before they can trade. Bitfinex does not officially say this, but customers also can no longer make fiat withdrawals of less than $10,000 either.

January 27, 2018 — Tether parts ways with accounting firm Friedman LLP. There is no official announcement; Friedman simply deletes all mention of Bitfinex from its website, including past press releases.

A Tether spokesperson tells CoinDesk: “Given the excruciatingly detailed procedures Friedman was undertaking for the relatively simple balance sheet of Tether, it became clear that an audit would be unattainable in a reasonable time frame.”

January 31, 2018 — The 2017 bitcoin bubble has burst. As the price of BTC plummets, tether issuance takes on a rapid, frenzied pace. In January, Tether issues 850 million USDT, more than any single month prior. Of this, roughly 250 million were created during a mid-month bitcoin price crash.

February 2018 — an ex-NFL owner named Reginald Fowler registers a company called Global Trading Solutions LLC. He goes on to set up bank accounts under the company’s name at HSBC.

February 20, 2018 — Bitfinex posts a fiat transactions delays notice, specifically noting delays between Jan. 10 through Feb 5.

February 20, 2018 — Dutch bank ING confirms Bitfinex has an account there. Two members of parliament in the Netherlands lodge questions for the finance minister after Dutch news site Follow The Money first disclosed the relationship on Feb. 14.

March 28, 2018 — Bitfinex weighs a move to Switzerland. Bitfinex CEO J.L. van der Velde tells Swiss news outlet Handelszeitung: “We are looking for a new home for Bitfinex and the parent company iFinex, where we want to merge the operations previously spread over several locations.” They end up moving their servers to Switzerland.

May 23, 2018 — Phil Potter steps down from his role as Bitfinex chief strategy officer. “As Bitfinex pivots away from the U.S., I felt that, as a U.S. person, it was time for me to rethink my position as a member of the executive team,” he says in a statement.

May 24, 2018 — Bloomberg confirms previous speculations that Bitfinex has been banking at Puerto Rico’s Noble Bank since 2017. Real Coin/Tether creator Brock Pierce is a cofounder of Noble Bank, along with John Betts, a former Wall Street executive.

These individuals had past dealings. In 2014, Betts led a group called Sunlot Holdings to try and acquire the failed Mt. Gox exchange. Pierce, along with former FBI director Louis Freeh were also involved in that effort. (Freeh has his own Twitter whistleblower, by the way.)

May 24, 2018 — The U.S. Justice Department launches a criminal probe into bitcoin markets. The focus is on illegal practices like spoofing, the process of putting up a large sell or buy and then cancelling, and wash trading, where a trader simultaneously buys and sells assets to increase trading volume. The criminal probe will bring in other agencies, including the CFTC.

June 1, 2018 — Looking to reassure its customers, Bitfinex hires Freeh Sporkin & Sullivan, a law firm co-founded by Freeh (the same Freeh who held an advisory role at Sunlot Holdings) to confirm that Tether has $2.55 billion in its banks, enough to cover the USDT in circulation at the time.

FSS is not an accounting firm. Further, there appears to be a conflict of interest. FSS Senior Partner Eugene Sullivan is also an advisor to Noble Bank, where Bitfinex and Tether hold accounts.

“The bottom line is an audit cannot be obtained,” Stuart Hoegner, Bitfinex and Tether’s general counsel, tells Bloomberg. “The big four firms are anathema to that level of risk…. We’ve gone for what we think is the next best thing.”

June 25, 2018 — Bolstering suspicions that tether is being used to prop up the price of bitcoin, researchers John Griffin and Amin Shams at the University of Austin, Texas, release a paper titled “Is Bitcoin Really Un-Tethered?” The two write:

“Using algorithms to analyze the blockchain data, we find that purchases with tether are timed following market downturns and result in sizable increases in bitcoin prices.”

June 27, 2018 — Several Bitfinex customers report delayed and rejected wire deposits. A representative of Bitfinex named “Garbis” takes to Reddit (archive) to explain that the situation was caused by a change in banking relations.

October 1, 2018 — Reports circulate that Noble Bank is up for sale, as a result of having lost several of its big customers, including Bitfinex and Tether. (I don’t know this for sure, but my guess is that Noble’s custodial bank, Bank of New York Mellon, likely told Noble to end its relationship with Bitfinex.)

October 6, 2018 — According to a report in The Block, Bitfinex appears to be banking at HSBC—a bank previously fined $1.9 billion in 2012 for money laundering—under the shell account “Global Trading Solutions.” (We find out later that the shell was registered by Arizona businessman Reginald Fowler.)

October 10, 2018 — Four days after reports comes out that Bitfinex is banking at HSBC, Bitfinex temporarily suspends all cash deposits, suggesting that the exchange is once again on the hunt for a new reserve bank. (As it turns out, the DoJ froze these accounts, so the money became inaccessible.)

October 14, 2018 — Amid concerns over Tether’s solvency and the company’s ability to establish banking relationships, tether’s peg slips again, this time to $0.92, according to CoinMarketCap, which aggregates prices from major exchanges. On a single crypto exchange Kraken, tether momentarily slips to $0.85.

October 16, 2018 — Tether appears to be holding reserves at Deltec Bank in the Bahamas. According to earlier rumors, the bank account was set up by Daniel Kelman, a crypto lawyer who was actively involved in trying to free the remaining Mt. Gox funds.

Further, Bitfinex appears to be banking through the Bank of Communications under “Prosperity Revenue Merchandising,” a shell company created in June 5, 2018. The Hong Kong bank is owned in part by HSBC and uses Citibank as an intermediate to send deposits to Deltec in the Bahamas.

October 24, 2018 — In a blog post (archive), Tether announces it has “redeemed a significant amount of USDT” and will now burn 500 million USDT, representing those redemptions. The remaining 446 million USDT in its treasury will be used as a “preparatory measures for future USDT issuances.”

November 1, 2018 — Tether officially announces (archive) that it is banking with Deltec and provides an attestation letter from the Bahamian bank that the account holds $1.8 billion, enough to cover the amount of tether in circulation at the time. The attestation has a mysterious squiggly signature at the bottom with no name attached to it.

We are pleased to be able to confirm that Tether has an account with Deltec Bank & Trust Limited https://t.co/LSn64soUsC . Balance confirmation at 2018-10-31 attached.

November 30, 2018 — Recall that in May 2017, the U.S. Department of Justice together with the CFTC began looking into illegal manipulation of bitcoin prices. And then in December 2017, the CFTC subpoenaed both Tether and Bitfinex. Now federal prosecutors have supposedly “homed in on suspicions that a tangled web involving Bitcoin, Tether and crypto exchange Bitfinex might have been used to illegally move prices,” according to Bloomberg.

November 27, 2018 — In a blog post (archive), Tether says its customers can once again redeem tether for actual dollars via tether.io. “Today marks an important step in Tether’s journey, as we launch a redesigned platform allowing for the verification of new customers and direct redemption of Tether to fiat.” All accounts require a minimal issuance and redemption of $100,000 USD or 100,000 USDT.

December, 18, 2018 — A Bloomberg reporter says that he has seen Tether bank statements from accounts at Puerto Rico’s Noble Bank and the Bank of Montreal taken over four separate months. The article suggests Tether holds sufficient dollars to back the tether tokens on the market. But again, these are attestations, not the full audit Tether has been promising for months. Notably from the report: $61 million Canadian dollars in the Bank of Montreal is listed under Stuart Hoegner, Bitfinex’s general counsel.

December 19, 2018 — Crypto Capital shares a letter with its customers. The letter is from Global Trade Solutions AG, the parent company of Crypto Capital Corp—not to be confused with Global Trading Solutions LLC, which is a shell set up by Reginald Fowler. The letter states that GTS AG is being denied banking services in the U.S., Europe, and elsewhere “as a result of certain AML and financial crimes investigations” by the FBI and cooperative international law enforcements and/or regulatory agencies.”

December 31, 2018 — By the end of 2018, roughly 1.9 billion tethers are in circulation.

January 16, 2019 — Bitfinex opens a data center in Switzerland, according to Handelszeitung. Previously, Bitfinex was relying on Amazon cloud servers. An earlier Bitfinex blog post confirms the move.

February 25, 2019 — In a blog post (archive), Bitfinex claims the U.S. government has located 27.7 BTC (worth about $100,000 at this time) taken from Bitfinex in the August 2016 hack and returned the funds to Bitfinex. The exchange says it has converted those bitcoin into USD and distributed the money to its RRT token holders. What is odd here is that the U.S. Department of Justice hasn’t issued any statement about recovered bitcoin. And Bitfinex doesn’t share a transaction record to show it actually received the recovered funds.

February 26, 2019 — Tether admits, for the first time that it is operating a fractional reserve and that tethers are no longer backed by cash alone. An update on the company’s website reads:

“Every tether is always 100% backed by our reserves, which include traditional currency and cash equivalents and, from time to time, may include other assets and receivables from loans made by Tether to third parties, which may include affiliated entities (collectively, “reserves”). Every tether is also 1-to-1 pegged to the dollar, so 1 USD₮ is always valued by Tether at 1 USD.”

“Every tether is always backed 1-to-1, by traditional currency held in our reserves. So 1 USD₮ is always equivalent to 1 USD.”

The change is also updated in Tether’s legal section.

April 9, 2019 — Bitfinex lifts its $10,000 minimum equity requirement to start trading. “We simply could not ignore the increasing level of requests for access to trade on Bitfinex from a wider cohort than our traditional customer base,” J.L. van der Velde says in a blog post (archive). Meanwhile, customers continue to complain that they are unable to get cash off of the exchange. And now some are saying they are having trouble getting their crypto off the exchange as well.

April 11, 2019 — Reginald Fowler, an ex NFL minority owner, and Ravid Yosef, who lives in Los Angeles and Tel Aviv, are indicted in the U.S. for charges related to bank fraud. The two were allegedly part of a scheme that involved setting up bank accounts under false pretenses to move money on behalf of series of cryptocurrency exchanges. (CoinDesk)

Also on this day, Bitfinex enables margin trading on tether. Margin pairs include BTC/USDT and ETH/USDT.

April 17, 2019 — Tether goes live on the Tron network as a TRC-20 token, a standard used by the Tron blockchain for implementing tokens, similar to and compatible with Ethereum’s ERC-20 standard. You can view the issuance on Tronscan.

April 24, 2019 — The New York Attorney General has been investigating Tether and Bitfinex for Martin Act violation. Allegedly, Bitfinex has been dipping into Tether’s reserves when it lost access to $850 million in the hands of its payment processor, Crypto Capital Corp. The investigation become public for the first time when the NY AG office sues iFinex, the parent company of Bitfinex and Tether, saying that the company has been commingling client and corporate funds to cover up $850 million in missing funds.

From 2014 to 2018, Bitfinex placed over $1 billion with Crypto Capital because it was unable to find a reputable bank to work with it. Crypto Capital then either lost, stole, or absconded with $850 million.

In order to fill the gap, Bitfinex dipped into Tether’s reserves for hundreds of millions of dollars. According to the NY AG, “Despite the sheer amount of money it handed over, Bitfinex never signed a contract or other agreement with Crypto Capital.”

Bitfinex: we are totes legit

Also Bitfinex: we privately gave $850m of commingled client deposits to a company we didn't sign a contract with, they took the money and ran, so we privately pilfered from our own "stablecoin" fund and demonized anyone who questioned the math pic.twitter.com/cJivO80tNa

April 26, 2019 — In a response to to the NY Attorney General’s allegations, Bitfinex says the $850 million has not been lost, but rather “seized and safeguarded.” Meanwhile, according to CoinDesk, Zhao Dong, a Bitfinex shareholder, claims that Bitfinex CFO Giancarlo Devasini told him that the exchange just needs a few weeks to unfreeze the funds.

April 30, 2019 — In response to the NYAG’s ex-parte order, Bitfinex general counsel Stuart Hoegner files an affidavit accompanied by a motion to vacate from outside counsel Zoe Phillips of Morgan Lewis.

In the affidavit, Hoegner admits that $2.8 billion worth of tethers are only 74% backed. And in its motion to vacate, Morgan Lewis argues that the NYAG has no jurisdiction over Tether or Bitfinex’s actions.

On this same day, Reginald Fowler is arrested. A grand jury has accused him of setting up a network of bank accounts to move money for cryptocurrency firms. He is linked to Crypto Capital’s $850 million in missing funds. (DoJ press release and indictment.)

May 2, 2019 — The U.S. Government wants Fowler held without bail due to flight risk.

May 3, 2019 — The NYAG files an opposition to Bitfinex’s motion to vacate. Bitfinex follows two days later with a response to the opposition. In the memo, Bitfinex argues that “nothing in the Attorney General’s opposition papers justifies the ex parte order having been issued in the first place.”

May 8, 2019 — iFinex has a new plan to raise $1 billion: a token sale. The company releases a white paper for a new LEO token. One LEO is worth 1 USDT, a flashback to when Bitfinex offered BFX tokens to cover the $70 million lost in a hack.

Meanwhile, Fowler is out on $5 million bail. He is required to give up his passport. Bail is posted in the Southern District of New York, where he is to appear for arraignment on May 15. His travel is restricted to parts of New York and Arizona.

May 6, 2019 — New York Supreme Court District Judge Joel M. Cohen rules that the NY AG’s ex parte order should remain in effect, at least in part. However, he thinks the injunction is “amorphous and endless.” He gives the two parties a week to work out a compromise and submit new proposals for what the scope of the injunction should be.

May 13, 2019 — Attorneys for the NYAG and iFinex failed to come to a consensus on what Tether should be allowed to do with its holdings. They submit separate proposals. iFinex is asking for a 45-day limit on the injunction and wants Tether employees to get paid using Tether’s reserves. The NYAG is not opposed to employees being paid, but it wants Tether to to pay them using transaction fees—not reserves.

May 16, 2019 — Judge Cohen grants Bitfinex’s motion to modify a preliminary injunction. The preliminary injunction is limited to 90 days, and Tether is allowed to use its reserves to pay its employees. The judge holds that the Martin Act “does not provide a roving mandate to regulate commercial activity.” Bitfinex and Tether still have to handover documents that the NYAG requested in its November 2018 investigative subpoena.

May 21, 2019 — Bitfinex files a motion to dismiss the proceeding brought by the NYAG on the grounds that Bitfinex/Tether do not do business in NY, the Martin Act does not apply to its business, and the Martin Act cannot be used to compel a foreign corporation to produce documents stored overseas. Bitfinex and Tether also seek an immediate stay of the NYAG’s document demands.

May 22, 2019 — Judge Joel M. Cohen of the New York Supreme Court grants Bitfinex’s motion for an immediate stay of the document demands. He issues an order requiring the companies produce only documents relevant to the limited issue of whether there is personal jurisdiction over the companies in New York but staying the document order in all other respects. The NYAG has until July 8 to file a response. And the judge schedules a hearing on the motion to dismiss for July 29.

July 22, 2019 — iFinex files court docs arguing once again that Bitfinex/Tether are not doing any business in New York and tether is not a security. (Here is Bitfinex counsel Stuart Hoegner’s affidavit and an accompanying memorandum of law submitted by the company’s outside counsel).

October 24, 2019 — Crypto Capital President Molina Lee is arrested by Polish authorities in connection with laundering money for Columbian drug cartels via Bitfinex, according to several Polish news sites.

March 30, 2021 — Tether releases another attestation, essentially saying that Tether has $35 billion in assets backing 35 billion tethers at a blink in time on Feb. 26, 2021. The report was done by Moore Cayman, an accounting firm in the Cayman Islands. It means nothing, as it is not a full audit and doesn’t say what sort of assets tethers are backed by. (David Gerard’s blog,Tether press release)

April 23, 2021 — Coinbase announces that it is listing USDT. (My blog)

May 13, 2021 — Tether publishes a breakdown of the assets behind tethers. It’s a one-pager consisting of two silly pie charts. A critical look reveals there’s only a tiny bit of cash left. (My blog)

# # #

*Update Feb. 20, 2021 — an earlier version of this article said Bitfinex listed tether in Feb. 25, 2015. It was Jan. 15, 2015.)

If you are an investigator or a reporter who has benefited from this work—or just another obsessed Bitfinex follower—please consider making a donation via Patreon.

Ethereum Classic was hit by a 51% attack. A private pool got hold of more than half of the network’s computing power and used that to rewrite history and double spend nearly $1.1 million ETC, the platform’s native currency. Coinbase noted the attack on January 5, and followed with a detailed analysis of what happened.

Here is the irony: Ethereum Classic was founded on the principle of immutability, meaning good or bad, legal or illegal, whatever transactions happen on the network, happen, and you have to live with it. The project took over the pre-fork chain after Ethereum forked to reverse transactions in the DAO hack. If Ethereum Classic wants to stand on that hill, it may have to suffer the consequences, which so far, have not been terrible. ETC was $5 at the time of the attack and is now at $4.66.

How is Ethereum Classic still worth anything right now

Bitcoin saw its 10-year anniversary on January 9. CoinDesk threw a whopping party in New York City, which, judging by photos, was well attended by a lot of white men. For bitcoiners, 10 years is a mark of resilience. But it is worth noting, for the most part, you still cannot buy groceries or pay rent with bitcoin. And if you bought bitcoin a year ago ($14,000) and sold today ($3,700), you would have lost two-thirds of your investment — so much for store of value.

KodakOne announced it generated $1 million in “post-licensing claims” on a beta of its platform. Breaker’s David Z. Morris did a softball interview with KodakOne’s Cam Shell, omitting tough questions like, “How in god’s name did you manage to come out with a beta version of the platform while stiffing all your developers?” I followed up with a story of my own as did Decrypt Media’s Ben Munster and David Gerard, explaining that the $1 million is completely hypothetical money.

Justin Sun, the CEO of blockchain platform Tron, has been unveiled as technically incompetent. Tron recently bought file-sharing client BitTorrent, Now it wants to launch a BitTorrent token. But, in a Breaker interview (another story by Z. Morris, but this one, really good), former BitTorrent executive Simon Morris said there is no way Tron can handle the transaction volume. Simon also said Sun has no technical know-how and Tron is basically little more than a marketing machine.

Rumors swirled a week ago that the co-CEOs of Chinese crypto miner maker Bitmain, Wu Jihan and Zhan Ketuan were going to step down. Turns out, the rumors are true, and Wang Haichao, Bitmain’s director of product engineering, has stepped in to replace them as CEO. In December, CoinDesk reported that Bitmain may be letting go of half of its 3,100 workforce. None of this bodes well for the company’s upcoming IPO.

If you want to trade bitcoin in India, you better keep that information well hidden from your bank. The country’s banks are sending out notices warning customers that they will close accounts without notice, if customers are found dealing in cryptocurrency.

Indian Banks now forcefully taking permission from us to 'reserve right to close our account without further intimation' if we deal in #cryptocurrency transactions

The Texas Department of Banking released a supervisory memorandum on January 2 in regard to treatment of virtual currencies under the Texas Money Services Act. According to the memo, Texas considers pegged stablecoins, like tether, money, which means that anyone dealing with them may need to apply for a Texas money transmitter license.

Ernst and Young (EY), the court-appointed monitor in Quadriga’s Companies’ Creditor Arrangement Act (CCAA), has filed its third report in Nova Scotia Supreme Court.

Ernst and Young (EY), the court-appointed monitor in Quadriga’s Companies’ Creditor Arrangement Act (CCAA), has filed its third report in Nova Scotia Supreme Court.

Gastauer, a man in his mid-40s who hails from Germany, also appears in an impressive Youtube

Gastauer, a man in his mid-40s who hails from Germany, also appears in an impressive Youtube  The 104 bitcoin (worth $468,675 CAD) that Canadian crypto exchange QuadrigaCX “inadvertently” sent to its dead CEO’s cold wallets on February 6—a day after the company filed for creditor protection—was due to a “platform setting error.”

The 104 bitcoin (worth $468,675 CAD) that Canadian crypto exchange QuadrigaCX “inadvertently” sent to its dead CEO’s cold wallets on February 6—a day after the company filed for creditor protection—was due to a “platform setting error.” QuadrigaCX creditors now have a legal team to represent them in the crypto exchange’s

QuadrigaCX creditors now have a legal team to represent them in the crypto exchange’s  Did you know that if you wanted to cash out of Quadriga, you could opt to hav

Did you know that if you wanted to cash out of Quadriga, you could opt to hav

Ethereum Classic was hit by a 51% attack. A private pool got hold of more than half of the network’s computing power and used that to rewrite history and double spend nearly $1.1 million ETC, the platform’s native currency. Coinbase noted the attack on January 5, and

Ethereum Classic was hit by a 51% attack. A private pool got hold of more than half of the network’s computing power and used that to rewrite history and double spend nearly $1.1 million ETC, the platform’s native currency. Coinbase noted the attack on January 5, and

{kind=link}