In case you missed my tweet, I ended up sick at the end of June. I was chatting with a friend over Zoom when he noticed that I was tilting over in my chair. Was I drunk? No. Should he call an ambulance? I’m fine.

I ended up in the ER the next day on IV fluids and hooked to monitors. Turns out I had Anaplasmosis from a tick bite. Doxycycline did the trick, and I was on my feet again within 48 hours.

Apparently, this is the price you pay for walking blissfully unaware through grassy fields and woodsy trails.

I mentioned earlier I was writing a book on NFTs. While I did a lot of research on the subject, I’m putting the book on hold for now. My concern is, who would read it? NFTs seem to have been a fad, slipping out of fashion.

If you are interested in the topic, check out my recent notes on NFTs and money laundering. I also wrote for Business Insider on how Metakovan was pumping Beeple NFTs months before he bought Beeple’s $69.3 million NFT at Christie’s.

I think we can all admit that the art behind almost every NFT is absolute garbage, which the author of this blog post does a fine job of pointing out.

China’s crackdown on crypto

The People’s Bank of China has hated crypto since 2017, when it initially kicked the crypto exchanges out.

In recent months, the country has gone after crypto with a renewed vengeance, banning FIs from providing services to crypto firms and forcing bitcoin miners in the country to take their hardware offline.

Up until recently, most of the world’s bitcoin mining (~ 65% to 75%) took place in China. The country’s crackdown on mining caused more than 50% of the bitcoin hashrate to drop since May.

The hashrate dropped faster than bitcoin’s difficulty algorithm could keep up. Every 2,016 blocks, the difficulty adjusts to account for how many miners are on the network.

On July 3, bitcoin experienced a record 27.94% drop in mining difficulty, according to BTC.com, meaning now, bitcoin miners will have an easier time finding blocks. (CNBC)

Beijing even told companies they are no longer allowed to provide venues, commercial displays, or even ads for crypto-related businesses. On Tuesday, the PBoC said it had ordered the shutdown of Beijing Qudao Cultural Development, a company that makes software for crypto exchanges. (Reuters)

Why does China loathe crypto? Some people say the PBoC is trying to make way for China’s CBDC, but I doubt that has anything to do with it. The most likely reason is the country wants to stem capital outflows. According to a Chainalysis report last August, $50 billion in crypto assets moved from China to other regions in a 12-month period.

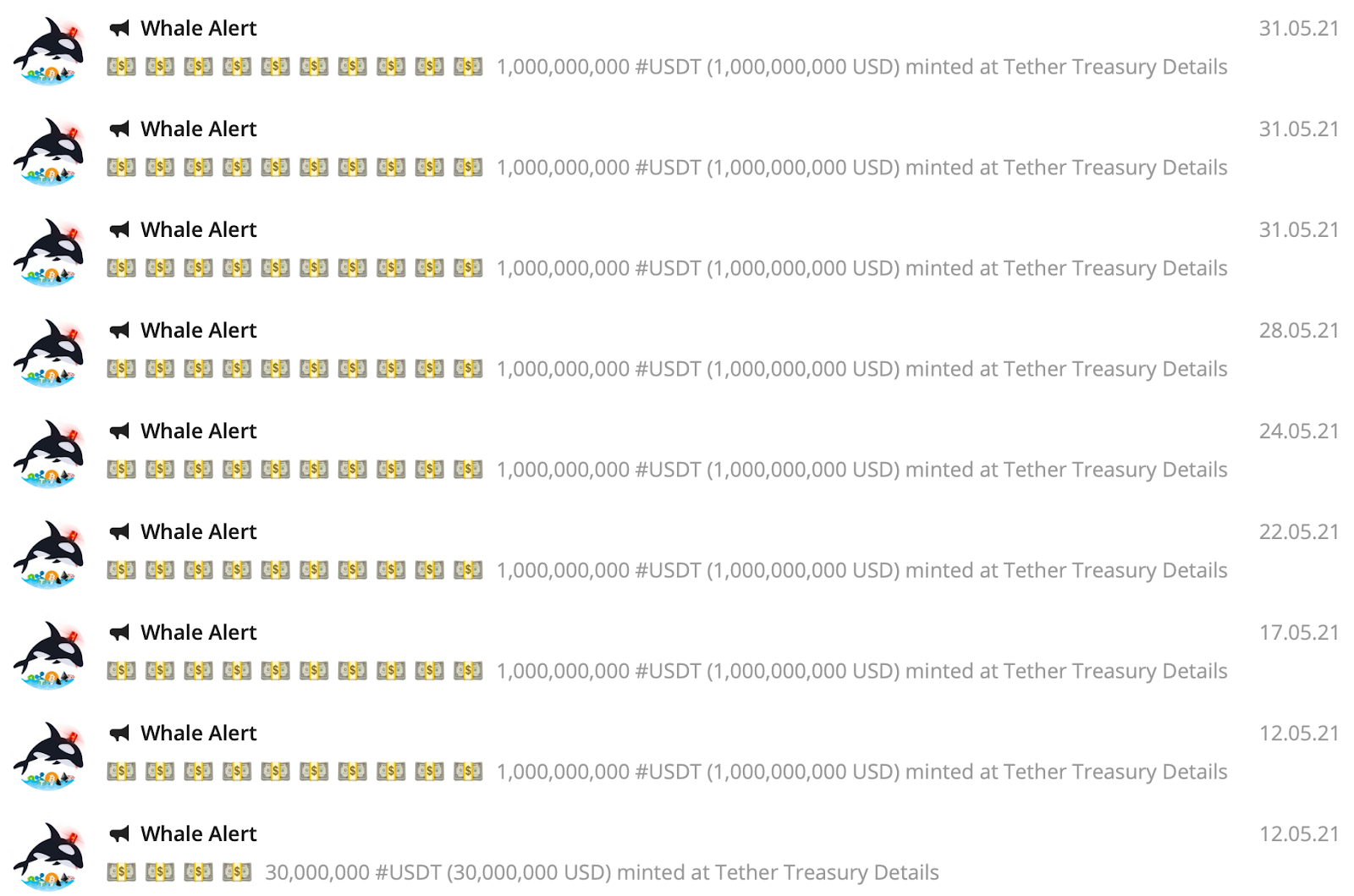

Why has Tether stopped printing?

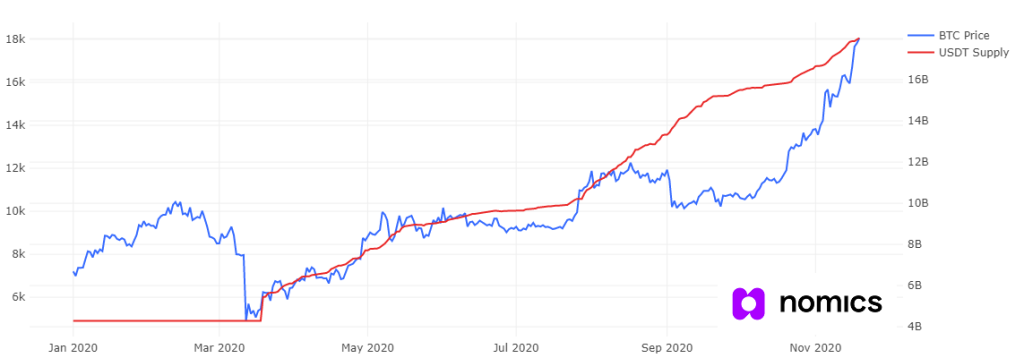

Tether is currently at 62.7 billion tethers, and it’s been stuck there for more than a month. Tether had several big prints at the end of May and now, crickets all through June and into July. The printer has totally stopped.

Nobody is really clear on why Tether has put its printing presses on hold, but the timing seems to correlate with China’s crackdown on crypto.

We have three theories for why Tether stopped printing

Theory #1 — Less demand

The China crackdown has created a reduced demand for tethers. When bitcoin’s hash rate dropped precipitously, so did the number of newly minted BTC per day — at one point it was down to 350 new BTC per day, as opposed to the 900 BTC per day the network should be producing.

Binance and OKex have mining pools, so bitcoin miners can mint bitcoin directly to their own exchange accounts. Since there is no way to cash out directly, miners convert BTC to tethers (USDT). And then convert USDT to RMB on unregulated over-the-counter platforms, such as Huobi and CoinCola.

With the exodus of miners from China, there was less demand for tethers.

Theory #2 — Chinese junk debt

Another theory floating around is that Tether may have been getting Chinese junk debt to issue tethers, and now that is no longer possible due to the risks.

Tether’s latest composition report showed that 50% of the assets backing USDT were unspecified commercial paper. In the US commercial paper market, that would place Tether among the likes of fund managers like Vanguard and BlackRock, which seems unlikely. (FT)

So maybe it’s holding Chinese paper?

“If Tether is holding Chinese commercial paper, the issuer can default on those debts with impunity. What is Tether going to do? Sue in Chinese courts?,” Tether whistleblower Bitfinexed said in a tweet.

He revealed in a DM that the info comes from a “reliable source.”

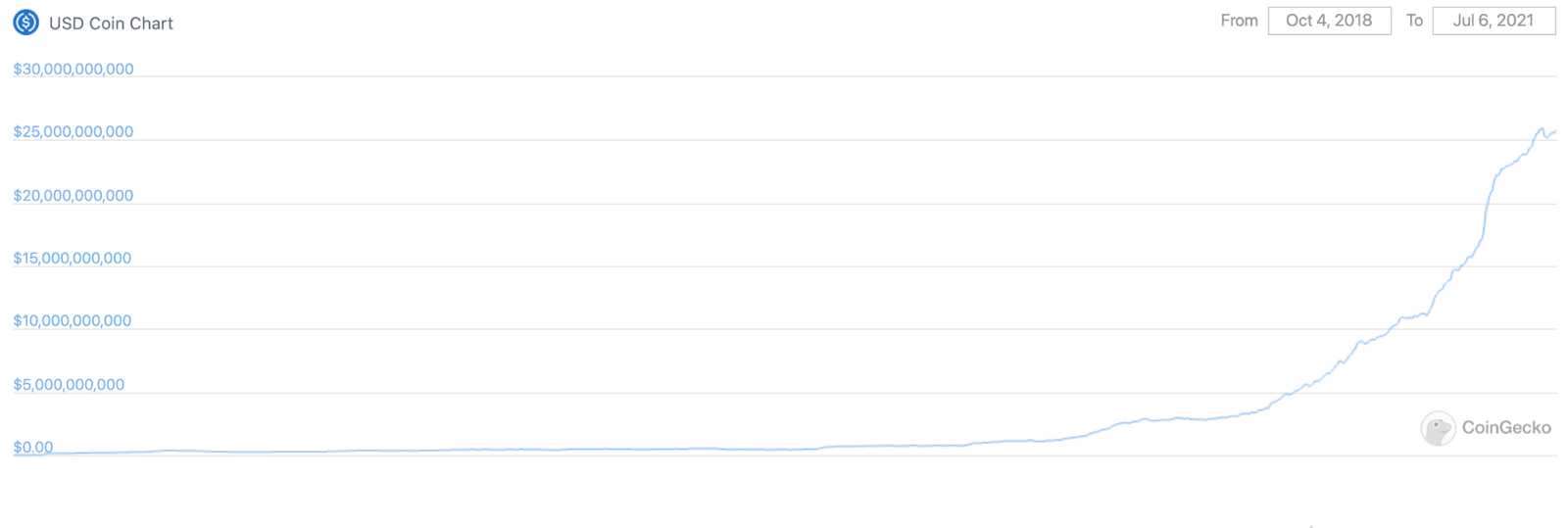

Theory #3 — USDC is picking up the slack

While the tether printer stopped, the USDC printer appears to have picked up speed, issuing 10 million USDC since May 8.

As of July 5, there are 25.5 billion USDC stablecoins in circulation, so maybe USDC is stepping into Tether’s shoes?

In other news, Tether is working hard to shine up its tarnished image. The company is hiring a Reputation Manager, to “advocate for the company in social media spaces, engaging in dialogues and answering questions where appropriate.”

If you want to fight the FUD spread by salty nocoiners like myself, this job could be for you. (Teether, archive)

Binance vs the world

The UK, Singapore, Japan, Germany, Canada and now the Cayman Islands are all moving against Binance, the world’s largest crypto exchange. I wrote a blog post detailing Binance’s pariah status.

The bad news keeps getting worse. Following the FCA banning Binance in the UK on June 26, Barclays says it is blocking customers from using their debit and credit cards to make payments to Binance. (They will let you take money out, but they won’t let you put money in.)

Binance “talks a big game on anti-money laundering and know-your-customer” rules, but was “resistant to throwing human resources at compliance issues,” an executive at a payments company that helped connect Binance to the broader financial market before cutting ties with the group, told the (FT)

And worse still — on Tuesday, Binance told its customers that it will temporarily disable deposits via SEPA bank transfers. Binance said the move was due to “events beyond our control.” (FT)

Binance founder CZ says it’s all FUD.

Binance’s organizational structure

Binance has a lot secrets. The company refuses to say where its headquarters is located. And it’s tight-lipped about its organizational structure, too.

On May 1, Brian Brooks, former Coinbase chief legal officer and former acting head of the Comptroller of the Currency, took over as CEO of Binance.US, replacing Catherine Coley. (WSJ)

In a Coindesk interview in April, he said he reports to the board of directors, yet he wouldn’t name who was on the board.

Coindesk: “Brian, what is the reporting structure with Binance US. Who do you report to?”

Brooks: “I have a board of directors, which I will be a member of, and I will report to that board.”

Coindesk: “Who else is on the board?”

Brooks: “The board is obviously the founder of the company and another person. It’s a private company, so we don’t necessarily go into the governance structure…”

Later when Coindesk asks him where Binance.com is located, Brooks dances around that question as well. He did say, however, that Binance keeps its US customer data separate from Binance.com.

Binance.US also just brought onboard Manuel Alvarez, a former commissioner at the California Department of Financial Protection and Innovation, as its new chief administrative officer. (Coindesk)

FATF releases 12-month review

The Financial Action Task Force, a Paris-based global anti-money laundering watchdog, published its second 12-month review of its revised standards for virtual assets and virtual asset service providers, or VASPs

VASPs include crypto exchanges, bitcoin ATM operators, wallet custodians, and hedge funds.

When the FATF published its guidance in 2019, it recommended full AML data collection by VASPs — and Rule 16, also known as the “travel rule.”

The travel rule requires VASPs to disclose certain customer data and include that data with a funds transfer, so that the info “travels” down the funds transfer chain.

Of FATF’s 128 reporting jurisdictions, 58 have implemented the revised FATF standards. The other 70 have not. And the majority of jurisdictions have yet to implement the travel rule.

“These gaps in implementation mean that there is not yet a global regime to prevent the misuse of virtual assets and VASPs for money laundering or terrorist financing,” the FATF said.

The FAFT plans to publish its revised guidance by November 2021 with a focus on accelerating the implementation of the travel rule as a priority. (Forkfast)

Kaseya ransomware

The REvil ransomware operation is behind a massive attack centering on Kaseya, a company that develops software for managed service providers. MSPs provide outsourced IT services to small and medium-sized businesses that can’t afford their own IT department.

Between 800 and 1,500 businesses have been compromised by the global ransomware attack, including schools in New Zealand and supermarkets in Sweden.

The REvil gang has offered to decrypt all victims for $70 million in Monero (XMR), a cryptocurrency that is harder to track than bitcoin. The immediate ransom demand is $45,000 worth of XMR, rising to $90,000 after a week.

Nicholas Weaver, a researcher at the International Computer Science Institute in Berkeley, wrote a story for Lawfare breaking down the Kaseya ransomware attack.

He also wrote an earlier story for Lawfare titled “The Ransomware Problem Is a Bitcoin Problem,” where he explains why getting rid of crypto is a great idea. “The ransomware gangs can’t use normal banking. Even the most blatantly corrupt bank would consider processing ransomware payments as an existential risk.”

El Salvador, bitcoin and Bitcoin Beach

Who is the San Diego surfer who brought bitcoin to El Zonte? A white evangelist named Michael Peterson. I wrote about him and his Bitcoin Beach project at length in a recent blog post.

Peterson read my story. He says it’s full of “glaring inaccuracies” and “plagiarized pieces of other bad reporting.” When asked to substantiate his defamatory accusations, he never replied back.

Does he use these same bully tactics to get people in El Zonte to use bitcoin?

David Gerard wrote up a detailed blog post explaining the latest developments on bitcoin and El Salvador.

Here are some notes, if you want to catch up quick:

- Nayib Bukele, El Salvador’s president, has announced a government wallet — the Chivo wallet — that will be available for download in September. (Youtube)

- The Chivo (slang for “cool”) wallet will hold both USD and bitcoin balances.

- Salvadorans who sign up for the mobile app will get $30 in bitcoin, but they have to spend it. They can’t sell their BTC for cash — which makes you wonder if Bukele is simply planning to issue new dollars under the guise of bitcoin. (I also recommend you read Gerard’s piece in Foreign Policy on this topic)

- The technical details of the Chivo wallet are totally unclear. Is Jack Mallers, the CEO of Zap and the remittance app Strike, going to develop the wallet? We don’t know.

- Originally, Mallers said Strike was using tether for remittances. (My blog post.) Now, he says Strike is no longer using tethers, and the folks in El Salvador receiving remittances on his app will receive actual dollars. (What Bitcoin Did)

- How will this happen? Mallers said in his What Bitcoin Did interview that his company has local banking relationships in ES, but we don’t know what banks, where.

- Here is a direct quote from the transcript of the interview: “So, I was like, ‘Well, fuck, I don’t know then how I’m going to pull this off!’ So, what I did is, we built Tether into Strike, which was the equivalent of the Chase bank account in America, and it at least gave us some MBP basic functionality, where I can go and just observe and listen and see how people used it and see if it was helpful. But now, we’re already integrating with the top five banks in the country.”

- Mallers tends to be long on plans and short on details. When the media reaches out to him with questions — like Decrypt did when they learned Zap is not licensed to operate in most US states — he generally just ignores them.

- Despite what Mallers keeps claiming, sending remittances via Western Union from the US to El Salvador isn’t really that costly, to begin with. Steve Hanke, Nicholas Hanlon, and Mihir Chakravarthi point this out in their paper: “Bukele’s bitcoin blunder.”

- Jack Maller’s company Zap (the parent company of Strike) got $14.9 million in fresh funding in March from “Venture Series – unknown,” on top of a $3.5 million seed round a year prior. Nobody seems to know who is behind the funding. (Crunchbase)

- Athena, the company that Bukele ordered 1,000 new bitcoin ATMs from, installed a new bitcoin ATM machine — the country’s third installed machine! — in La Gran Vía shopping center. They had a ribbon-cutting ceremony and everything.

- Unfortunately, the machine was located in front of an upscale department store owned by the Simán family, Bukele’s arch enemy. Worried that the ATM would draw foot traffic to his rival’s business, Bukele had the machine relocated next to the toilets, where it sits unplugged. (Twitter)

- The US State Department named 14 El Salvadorans, many associated with the Bukele regime, as corrupt or undemocratic actors. (US State report)

Robinhood’s planned listing

Robinhood had plans to go public in June, but the SEC has some questions about its cryptocurrency business, according to Bloomberg.

The company also agreed to pay FINRA $70 million to settle allegations that the brokerage caused customers “widespread and significant” harm on multiple different fronts over the past few years.

Specifically, FINRA’s investigation found that millions of customers received false or misleading information from Robinhood on a variety of issues, including how much money customers had in their accounts, whether they could place trades on margin and more.

In its SEC S-1 filing, which dropped on July 1, Robinhood notes that a “substantial portion of the recent growth in our net revenues earned from cryptocurrency transactions is attributable to transactions in Dogecoin. If demand for transactions in Dogecoin declines and is not replaced by new demand for other cryptocurrencies available for trading on our platform, our business, financial condition and results of operations could be adversely affected.”

Robinhood currently supports seven different cryptos. When you trade crypto on Robinhood, you don’t ever hold the keys to your own crypto. Robinhood itself buys the actual crypto and maintains custody, so you can’t move your coins onto or off the platform. You’re stuck in there.

Bitcoin mining turns NY lake into a hot tub

The Greenidge Generation Bitcoin mining plant, owned by private equity firm Atlas Holdings, sits on the shores of beautiful Seneca Lake in New York.

The tagline on its website reads, “Green Power for Generations to Come.”

The firm uses lake water to cool its 8,000 computers used to mine bitcoin within the gas-fired plant. Greenidge’s current permit allows it to take in 139 million gallons of water and discharge 135 million gallons daily, at temperatures as high as 108 degrees Fahrenheit in the summer and 86 degrees in winter.

Locals want the mining facility gone. They have been staging protests. They claim the plant is polluting the air and heating the lake, thanks to its use of fossil fuels.

“The lake is so warm you feel like you’re in a hot tub,” said one nearby resident. (NBC) (Arstechnica)

RSA Conference’s blockchain moment

Over the weekend, the RSA Conference gave infosec and computer science Twitter a bit of a shock when it suggested replacing the entire internet with — a blockchain.

The tweet quickly disappeared, but not before being archived. The blockchain is immutable! I wrote about the event in a blog post.

(Updated on July 8 to note that Brian Brooks replaced Catherine Coley as CEO of Binance.US.)

If you like my work, please subscribe to my Patreon account for as little as $5 a month.