There’s a lot of class action lawsuits in crypto. We mostly don’t note these — they so rarely go anywhere — but a consolidated class action against FTX’s various enablers has turned up some interesting allegations concerning everyone’s favorite stablecoin, Tether, and its remaining US dollar banker, Deltec Bank of the Bahamas.

Tether has banked with Deltec since 2018. Deltec was one of the few banks in the world that would have anything to do with Tether after their deal with Crypto Capital led to $850 million of the Tether reserve being frozen.

We already knew that FTX/Alameda, also based in the Bahamas, was in it up to their necks with Tether. Alameda was Tether’s largest customer between 2020 and 2022 that wasn’t a crypto exchange.

The new allegations, filed in a Florida federal court, are that Deltec was an active and enthusiastic part of the FTX and Alameda business schemes that lost billions of customer dollars and for which Sam Bankman-Fried is now in jail.

The amended complaint

The new amendment to the complaint, filed on February 16, is based on 7,000 pages of direct text messages that were offered up in discovery. The full amended complaint is 158 pages. The Deltec shenanigans are paragraphs 133 to 260. [Motion, PDF; Complaint, PDF; Case docket]

The complaint hammers on Deltec’s relationship with Tether, FTX, and Alameda. It states that Jean Chalopin, the head of Deltec, and Gregory Pepin, Deltec’s deputy CEO, played a key role in FTX’s money laundering.

FTX/Alameda: MONEY PARTY THE BEST PARTY

Bankman-Fried’s empire came crashing down in November 2022, when it was revealed the company had an $8 billion hole in its customer accounts. The complaint lists the various defendants in the case — Gary Wang, Nishad Singh, Caroline Ellison, Ryan Salame, and others.

Deltec provided banking for FTX Trading, FTX US, and Alameda. Pepin manually allocated incoming customer funds to FTX accounts and moved the funds to Alameda. Deltec also extended a “secret line of credit” to Alameda of $1.8 billion.

Deltec was a money launderette for FTX. They would happily let all those annoying compliance requirements slide for their very good friends at FTX.

Deltec would pass compliance questions from intermediary banks to FTX or just make up fake invoices to account for otherwise unexplained transactions. Here’s Pepin:

[Ibanera] are asking info about [the foregoing FTX customer] do you have the agreement linked to this deposit? so i can get [the wire] release asap?

Idea 🙂 Send me a PDF of the term and condition + Invoice and I’ll send

… Now if you send me a XLS sample or whatever of invoice I can populate invoice myself later can do?

Pepin would send ecstatic messages in the group chat when a batch of wires came in. The complaint has a whole page of Pepin posting like this:

MOOONNNEEEYYY TTTIIIIMMMMEEEE

I HEAR A MONEY TIME IS HAPPENING HERE I THINK I NEED TO BE A PART OF IT

doing my best to hold the wall but such money tsunami is hard to handle dude

MONEY PARTY THE BEST PARTY

it is MONEY TIME INDEEDE

Deltec Bank also moved FTX customer deposits directly to Alameda on request, in the billions. Deltec would even run out of cash to pay FTX customer withdrawals and have to ask Alameda to cover for them. Pepin: “Lena you send today the 300m? or later? As we won’t have liquidity”.

Moonstone Bank

Chalopin bought Farmington Bank in Washington in 2020 in a deal with FTX, turning a tiny local bank into a crypto service company — mostly for FTX and Alameda. The bank was then renamed Moonstone.

Moonstone joined the Federal Reserve without notifying the Fed of its change of business plan from a local farmers’ bank to a crypto money launderette. The Fed shut Moonstone down in August 2023.

North Dimension: Ipad 11 “ich Cell Phone

North Dimension was a fake electronics company that FTX/Alameda created so they could set up accounts at Silvergate Bank and Signature Bank in its name. FTX had customers wire money to North Dimension’s Silvergate and Signature accounts so that it would go directly to Alameda. This was part of the money laundering charge that Bankman-Fried was convicted on.

Pepin made sure that deposits from North Dimension came through to Deltec and were sent to FTX or Alameda as needed.

FTX put actual effort into the North Dimension bit of the fraud, if only the barest minimum. North Dimension even had a website!

The site didn’t actually work — all the product links went to the contact page. It was “rife with misspellings and bizarre product prices,” including “sale prices that were hundreds of dollars above a regular price” — such as the fabulously desirable “Ipad 11 “ich Cell Phone,” normally $410, but available at a sale price of just $899.

The North Dimension website is in the Internet Archive. The “About” page is a trip. The company logo comes from DesignEvo Free Logo Maker — it’s their “3D Orange Letter N” logo. You can see every penny of the twenty-five cents they spent on this. [North Dimension home page, archive; product page, archive; about page, archive; DesignEvo]

Tether and Deltec

When Tether became a Deltec customer in November 2018, it deposited about $1.8 billion — making up nearly half of Deltec’s total deposits at the time.

Alameda was the second-largest creator of tethers (USDT) — “about one-third of USDT minted at any time went to Alameda.”

The USDT was funded with FTX customer deposits which Deltec routed to Alameda. Remember that Alameda and FTX were claiming at this time to be completely separate operationally.

Alameda created and redeemed tethers directly via Alameda and Tether’s Deltec accounts. Alameda would first send a message to the Alameda/Tether/Deltec group chat. Transfers would often have to wait for Pepin to be awake.

Alameda pumping out new tethers seems to have been the engine for the billions of tethers printed in 2020, 100 million at a time: “In total, Alameda minted more than $40 billion USDT through this scheme, encompassing nearly half of USDT in circulation at the time.”

How solidly backed was USDT by the account at Deltec? About as solidly as it was in 2017 when Tether didn’t have a bank account at all for months at a time:

… in November 2018, Deltec Bank provided an assurance letter stating that USDTs were fully back by cash, one U.S. dollar for every USDT. However, the next day, Tether began to transfer hundreds of millions in funds out of its Deltec Bank account, such that within 24 hours, Deltec Bank’s assurance letter was no longer true.

FTX’s alleged Tether scam

The complaint postulates that Alameda was furiously printing tethers so that Alameda could make less than a tenth of a percent from arbitraging the price of USDT:

Upon information and belief, Alameda and Tether profited from the scheme as follows. Alameda would create USDT in amounts and at times that would inflate the market price of the stablecoin. Alameda would promptly sell the USDT in the market, at several basis points above the purchase price. Tether, in turn, would receive U.S. dollars for stablecoins it minted from nothing.

This sounds unlikely to us — there just isn’t the volume on any existing USD-USDT trading pair. To turn USDT into dollars in any quantity, you need to buy crypto then sell that at an actual-dollar exchange.

Deltec allowed Alameda a three-day grace period to pay for its freshly created USDT — that $1.8 billion line of credit. We think Alameda’s scam would have been to do some market-moving trades to make enough dollars to pay for the tethers they’d just bought.

Attachments to the complaint

Also attached to the complaint is a declaration from Caroline Ellison, former head of Alameda. Ellison apparently settled with this class action’s plaintiffs in January 2024 and offered to assist them. This declaration asserts the accuracy of the claims in the complaint as far as Ellison directly knows.

FTX former counsel Dan Friedberg adds a declaration. Friedberg has also settled with the plaintiffs of this class action. He only confirms the plaintiffs’ claim that Avinash Dabir managed FTX’s celebrity sponsorships out of FTX’s Miami office.

The last attachment on the amended complaint is a transcript of a podcast with Dabir talking to Joe Pompliano on the Joe Pomp Show about FTX’s celebrity sponsorships.

Harborne corrects the record by lawsuit

Christopher Harborne, shareholder of 12% of the Tether empire under his Thai name, Chakrit Sakunkrit, is suing the Wall Street Journal for an article it wrote in March 2023. The story was about Tether’s efforts to get banking after they were cut off by correspondent bank Wells Fargo in 2017. [Complaint, PDF, archive]

The WSJ story said that Harborne aided Tether’s efforts to skirt the traditional banking system by using his company AML Global to set up an account at Signature Bank: “The Sakunkrit name had earlier been added to a list of names the bank felt were trying to evade anti-money-laundering controls when the companies’ earlier accounts were closed, but Mr. Harborne’s hadn’t.”

Harborne states that “AML’s Signature Bank account was never used for Tether or Bitfinex whatsoever.” WSJ told him that the story didn’t imply that he had committed crimes, but he is suing over a claimed inference that he had.

WSJ edited the story on February 21 to remove the bits about Harborne. [WSJ; archive of March 3, 2023]

Harborne’s lawyers also reached out to Mike Burgersburg, a.k.a. Dirty Bubble Media, asking him to take down his article on Harborne. Mike kept the story up but made edits. [Dirty Bubble,archive of November 30, 2023]

Originally Mike had noted that the account Harborne set up at Signature was a back door for Bitfinex to access the US banking system. His source was the WSJ. “This was edited because WSJ removed those comments from their story. I am not making this claim, and there is no evidence at present for this assertion,” Mike said.

Tether is run by a handful of people, some known and many unknown. Former CTO Paolo Ardoino is the named CEO and he acts like a social media intern. This reeks of Ardoino being the fall guy for whoever actually is running Tether.

Harborne doesn’t want to be thought to be that person. He says he “is not now and never has been in any management or executive role at Bitfinex or Tether; he is merely a minority shareholder.” A large chunk of his net worth is apparently in ether. His son, Will Harborne, has worked for various iFinex entities over the years.

Squeal!

Pig butchering scams, a.k.a. romance scams, have taken $75 billion from victims, according to a study by University of Texas finance professor John Griffin and his student Kevin Mei.

Once scammers collect the funds, they most often convert them to tethers: “Funds exit the crypto network in large quantities, mostly in Tether, through less transparent but large exchanges—Binance, Huobi, and OKX.” [SSRN]

Zeke Faux researched Tether’s pig butchering use case in depth for his book Number Go Up. That chapter of the book was put up by Bloomberg as a teaser. [Bloomberg, 2023, archive]

Griffin has been following Tether for some years. He was behind another paper on Tether money flows, 2018’s “Is Bitcoin Really Un-Tethered.” That study showed how Tether was used to prop up the price of bitcoin for most of the 2017 crypto bubble.

Tether shills on Twitter have been frantically congratulating Tether on its “deal” with the Department of Justice to combat romance scams. No such deal has been announced. [Twitter, archive]

Just in case

USDT tokens are currently available on 15 different blockchains. Most of the issuance is on Ethereum and Tron.

Tether has proudly announced a recovery tool in case any of these blockchains have problems and your USDT becomes inaccessible. [Tether, archive]

We doubt Tether would make an announcement like this without a gun to their heads. So this reads to us like Tether reassuring the crypto whales that their tethers will be protected if Tron goes down.

Heading for the trillion

Tether crossed 100 billion USDT in circulation on March 5. This is completely in line with Dan Davies’ theory from Lying for Money that frauds snowball over time:

The reason for this is that unlike a genuine business, a fraud does not generate enough real returns to support itself, particularly as money is extracted by the criminal. Because of this, at every date when repayment is expected, the fraudster has to make the choice between whether to shut the fraud down and try to make an escape, or to increase its size; more and more money has to be defrauded in order to keep the scheme going as time progresses.

The news about crossing 100 billion made it into Reuters, which noted Tether’s remarkably non-transparent reserves and the risks Tether poses to crypto and the broader financial system. [Reuters; Reuters]

Tether needs to be shut down. We’ve been saying this since 2017. It’s a risk to anyone who holds crypto. It’s also helped to accelerate other scams, so they’ve grown to a whole new level.

As we write this, Tether has just printed 2 billion USDT — its biggest issuance yet. Tether has printed 5 billion new USDT in just the past week. Gotta keep number going up. MOOONNNEEEYYY TTTIIIIMMMMEEEE!

Image: Gregory Pepin photographed on the ipad 11 “ich sell phone.

(Updated March 12 at 5PM ET to add a quote from Mike Burgersburg and clarify why he edited his story on Tether.)

_______________________________________________

And now, a word from our sponsors

We write this newsletter for money. Please send us some! Here’s Amy’s Patreon and here’s David’s. For casual tips, here’s Amy’s Ko-Fi and here’s David’s.

If you like our work, become a patron! Here’s Amy’s Patreon, and here’s David’s. Sign up today!

Arizona businessman and sports investor Reggie Fowler spent decades talking himself out of sticky situations. But in a Manhattan courtroom on June 5, reality finally caught up to him.

US District Judge Andrew Carter sentenced Fowler, who is 64 years old, to 6 years and 3 months in prison for his role in hiding cryptocurrency transactions on behalf of shadow banking operation Crypto Capital and the disappearance of hundreds of millions of dollars. Fowler will surrender in Phoenix at 10 a.m. on June 30, giving him three weeks to get his affairs in order and rehome his dog.

Fowler’s crypto frauds were the beginning of the more recent frauds in the crypto space, and the failures of the Silvergate and Signature banks, prosecutors said in court.

“I have harmed the people of the AAF and my family,” sobbed Fowler. “I am embarrassed and ashamed.” Poor fellow.

Just a little off the top

Crypto Capital was a Panama-incorporated money transmitter that served as a shadow bank for many US and Canadian crypto exchanges, including Bitfinex and the failed QuadrigaCX — because they had enormous trouble getting proper banks to talk to them.

Throughout 2018, Fowler was Crypto Capital’s US contact. He set up a network of bank accounts in the US and abroad so that Crypto Capital could process payments for its customers without worrying about all those tedious anti-money-laundering laws.

Fowler lied to the banks, telling them that the accounts were for his real estate business. His scheme ran internationally and received over $740 million just in 2018. Most of this was Bitfinex customer money. A “Master US Workbook” listed more than 60 bank accounts around the world, which totaled over $345 million by January 2019. [Decrypt]

Fowler didn’t worry too much about separating Crypto Capital or Bitfinex money from his own funds. He and his co-conspirators set up a “10% Fund,” skimming from client deposits for themselves.

In the original indictment, and again at today’s sentencing, prosecutors detailed “additional criminal conduct” Fowler seemed to be involved in — though he wasn’t charged on these.

Fowler allegedly tried many times to get bank loans using fraudulent bond certificates, valued in the billions, as collateral. He tried to use funds from the Crypto Capital scheme as collateral for loans. He was caught with $14,000 in sheets of counterfeit $100 notes right there in his office.

Fowler was arrested in Chandler, Arizona, on April 19, 2019.

Prosecutors piled on more charges in a superseding indictment in February 2020 after they discovered Fowler had been using Crypto Capital money to fund the AAF. That funding fell through after the Department of Justice seized $68 million from Fowler’s bank accounts at HSBC in late 2018.

Fowler, who had fumbled an opportunity for a plea deal in January 2020, pleaded guilty to all five counts against him in April 2022, throwing himself at the mercy of the court. He has remained out of jail since his initial arrest on $5 million bail.

A respectable businessman of flawless repute

Fowler’s lawyer Ed Sapone wrote a letter to the judge on April 10 asking for clemency for his client — that is, no jail time at all.

Sapone argued that Fowler had lived a hard life, growing up in the South without parental support, and had never broken the law before. At least not in any way that landed him behind bars. [Doc 124, PDF]

Never mind that Fowler was a fully-grown 59-year-old man at the time of his crimes with a long career as a (cough) sharp businessman behind him.

In a sentencing submission, prosecutors said that they didn’t appreciate that Fowler had blown $200,000 gambling in casinos since his guilty plea, rather than using those funds to pay back his victims. [Doc 125, PDF]

Prosecutors also noted that in December 2016, Fowler was stopped at the Canadian border with items associated with a “black money scam” — a scheme where a con artist claims to have stacks of US bills dyed black to avoid detection. The bills will come clean if you just purchase this expensive “special chemical.”

Hard work and perseverance

Fowler’s story reads like an episode of American Greed — where money seduces and power corrupts.

Before his path crossed that of Crypto Capital, Fowler’s main business was Spiral Inc. — a holding company for about a hundred different businesses, including ice rinks, car washes, and a foam food tray manufacturer company. Most of the businesses were located between Arizona and Colorado.

Fowler was also a pilot and owned two jets — a Cessna Citation CJ2 and a CJ3, which he flew for business and loaned out.

He touched many lives including friends in the sports world and those who depended on him for their livelihood. Because Amy wrote about Fowler regularly, people who knew him contacted her. Sources described Fowler as well-read, charming, and a “fantastic salesperson, overbearing and confident.” He was not a gambler, at least not before his indictment, said a source. He never drank and worked out at the gym religiously.

What Fowler was not good at, however, was shedding businesses that were dogs — like his “Shammy Man” carwashes in Arizona, which he co-owned with a partner who served time in federal prison — or putting money into the ones that were doing well.

His firm Styro-Tech in Denver was making money hand over fist, but Fowler couldn’t seem to invest in better equipment and he was always hiring illegal immigrants cheap. “He could never pay anybody what they were worth,” said one source. “I don’t know how many times he got caught hiring illegals.”

Football obsessed

Fowler was a football player in his youth and remained an obsessive fan. His obsession with the game played no small part in his downfall.

He kept a Cincinnati Bengals helmet in his office and gave people the impression that he had played professionally for the Bengals — though he had only attended training camp.

In 2005, Fowler tried to purchase the Minnesota Vikings from Red McCombs in a $600 million deal. “He was 100 percent committed to getting it done,” McCombs said. “He was very straightforward. He said, ‘I am going to buy your football team.’” Fowler would have been the NFL’s first Black owner. [LA Times, 2005]

But the deal led to financial scrutiny, and the Star Tribune uncovered several outright lies in Fowler’s resume, so Fowler pursued a limited partnership instead. The cash he put up for the 3% ownership in the Vikings got him into financial trouble. [Minnesota Public Radio, 2005]

Things went from bad to worse, and Fowler went deeper into debt. He refinanced Spiral in 2006, landing him $65 million in debt. The credit crisis followed in 2008, and Spiral never recovered. By 2013, the company was in receivership, and Fowler lost control of all his businesses. By October 2014, Fowler no longer had a stake in the Vikings. [Resolute, 2022; Star Tribune, 2014]

At some point over the following years, a debt-saddled Fowler crossed paths with the people at Crypto Capital — Oz Yosef and his sister Ravid. The Yosefs were both later indicted for their part in Fowler’s fraud, but remain at large.

Crypto had an interesting year in 2017. Bitfinex, the largest crypto exchange at the time, lost its ties to the traditional banking system when its Taiwanese banks were cut off from correspondent banking by Wells Fargo. Short of real dollars, and trying to recover from a $72 million hack in 2016, Bitfinex and its sister company, stablecoin issuer Tether, began pumping out tethers at a pace unlike anything before — frequently with no dollars backing them at all. (Just like the salty nocoiners told you at the time.)

Fueled by these unbacked fake dollars pouring into the crypto markets, the price of bitcoin climbed to new highs. A year later, Fowler found himself in control of bank accounts with hundreds of millions of dollars flowing through them. And then football called to him again.

AAF: the Fyre Festival of football

Alternative football leagues have a long history of dismal failure. In 2017, TV producer Charles Ebersol came up with an idea for a springtime football league that would be a feeder for the National Football League.

Somehow “millions” of fans would have an interest in watching football after the Super Bowl. The Alliance of American Football would even come with a killer app that promised to change sports gambling as we know it.

Ebersol and AAF co-founder Bill Polian, an NFL executive, attracted some seed capital. In June 2018, Willie Lanier, a former Super Bowl champion, introduced Ebersol to Fowler. Fowler offered to be a lead investor, committing $170 million — a $50 million line of equity and a $120 million line of credit. Prosecutors wrote in their letter to the court:

During a June 2018 meeting with AAF executives, including AAF co-founder Charlie Ebersol, Fowler showed the AAF corporate team printouts of bank account information purporting to show that Fowler had hundreds of millions of dollars in foreign bank accounts. Fowler would not let anyone take the printouts after the meeting. Fowler told Ebersol that Fowler’s wealth, which he said was largely in cash, came from real estate holdings and an aviation business that built drones in Germany for U.S. Government contracts. During an October 2018 meeting, one of Ebersol’s associates took a picture of a bank account printout that Fowler presented. That printout showed roughly $60 million in an HSBC account.

That HSBC account would be one of the accounts that was frozen by the Department of Justice in that very month.

Ebersol claims in an affidavit that he did his due diligence on Fowler — though clearly he did not. All Eberson would have had to do was look up all the multiple lawsuits against Fowler. Peter Thiel also invested in AAF through his Founders Fund.

The league kicked off in February 2019 — with eight teams and more than 400 players — but after eight weeks of play, the dream unraveled when Fowler missed a $28 million payment because all his money had been frozen. [Affidavit, PDF; CNBC, 2018]

The AAF disintegrated into the football version of the Fyre Festival. They missed payroll in the first week one, blaming it on a computer glitch. Players had been booted out of their hotels and had to pay cash for their flights back home.

Another investor, Tom Dundon, took over the league, but he soon gave up throwing money into the pit as well. The AAF declared bankruptcy on April 17, 2019 — and multiple lawsuits against its founders ensued. [Twitter, archive; Twitter, archive; Sports Illustrated]

End of the linebacker

What can we learn from Reggie Fowler? Mostly that pigs get fat, but hogs get slaughtered.

Fowler spent decades doing sharp business that didn’t quite get him in trouble with the law. Then he got in a bind and let his hubris do the thinking for him. Like so many in crypto, he found out that this works until it doesn’t.

By the time he gets out of jail, Fowler will be 70. In the four years between his arrest and today’s sentencing, he spent his time just going to work every day. We predict he’ll get out of jail and just get back into running businesses until the day he drops. Hopefully less flagrantly illegal ones.

It looks like Reginald Fowler, the man tied to hundreds of millions of dollars of missing Tether and Bitfinex money, has ditched plans for renegotiating a plea deal. Instead, he is planning to head to trial.

In aletter filed with the New York Southern District Court on July 7 on behalf of both parties, the government stated: “The parties are not currently engaged in plea negotiations and do not anticipate resuming negotiations.”

Prosecutors are requesting a trial date in early February with pretrial motions beginning in October. The trial is expected to last two weeks.

[Update Aug. 4: Fowler’s trial is set for Feb. 14, 2022. Here is the order.]

Fowler was indicted in April 2019, along with Israeli woman Ravid Yosef, who is still at large. The pair allegedly lied to banks, telling them they were in the real estate business so they could illegally open up accounts to store funds for cryptocurrency exchanges on behalf of Crypto Capital, a shadow banking operation.

At the time, Judge Andrew Carter gave Sapone three months to get up to speed on the case and warned: “You are going into this with your eyes wide open.”

Preparing for trial means a lot more work for Sapone, so it is a surprise he wasn’t able to work out something with prosecutors.

Fowler came very close to a plea deal on January 17, 2020.

On that day, the former football player stood before the judge in a Manhattan courtroom ready to plead guilty to count four of his indictment — charges of operating an unlicensed money transmitter business — pursuant to negotiating with the government.

Had he accepted the deal, Fowler would have likely spent five years in prison with three years of supervised release, and paid a fine of up to $250,000.

But the deal, which required Fowler to forfeit $371 million held insome 50-odd bank accounts, fell apart at the last minute. Why? Because nobody was sure of the exact amount in the bank accounts and Fowler would have been on the hook for the difference.

James McGovern, Fowler’s defense attorney at the time, told the judge:

“The issue with respect to the forfeiture that became an issue for us today stems from the fact that none of the parties seem to have an idea of how much money is at play here in the forfeiture order because these accounts that have all been frozen by one entity or another have an amount of money that nobody seems to know how much is in there. So our issue is how much actual exposure under the forfeiture order after the accounts are liquidated is Mr. Fowler looking at. That’s kind of the heart of the issue.”

On Feb. 20, 2020, the government filed a superseding indictment against Fowler, adding wire fraud to existing charges of bank fraud, illegal money transfer, and conspiracy. Wire fraud alone is punishable with up to 20 years in prison, so Fowler, 61, could be looking at spending the rest of his life behind bars.

There was speculation that Fowler’s defense team would try again to work out something with the government. He could still negotiate a deal, but by the tone of the prosecutor’s letter today, it sounds unlikely.

Reginald Fowler’s lawyers confirmed that money is indeed at the center of a conflict between them and their client — and the main reason why they want to withdraw from the case.

The news was revealed Friday in a telephone status call attended by Assistant US Attorneys Jessica Greenwood, Sheb Swett and Sam Rothschild; Fowler’s defense team, James McGovern, Michael Hefter, and Sam Rackear of Hogan Lovells, and Scott Rosenblum of Rosenblum Schwartz & Fry; and Fowler himself.

Fowler, a former NFL investor — who resides in Chandler, Arizona, and is free on bail — is accused of setting up a shadow banking service that has been linked to Crypto Capital, a Panamanian firm at the center of the New York Attorney General’s investigation into crypto firms Bitfinex and Tether.

As I wrote earlier, Fowler’s defense counsel have been careful about disclosing details on why they want to ditch their client, who they have been working with since Fowler was indicted in April 2019.

District Judge Andrew Carter began the call: “Defense, can you give me a little further elucidation regarding the grounds for your seeking to be relieved without getting into any privileged or confidential materials?”

Fowler’s attorney McGovern said the matter involved privileged and confidential information but added: “I think it is fair to say that it is of the nature that the government assumes in their filing, of a fee-based nature.”

Judge Carter cut straight to the heart of the matter: “So it is fair to say, without getting into the details, this is about lawyers not getting paid?”

“Yes,” McGovern answered, but added it was “a little bit more than that.” He then suggested that his team file an ex-parte submission setting out the nature and specifics of the request to withdraw. “That way, we’ll provide the court with a substantial amount of information that will provide color for the entire discussion,” he said.

Fowler is represented by two legal firms. Carter asked if the nature of the conflict was the same for both firms. “Yes,” responded Rosenblum, Fowler’s attorney at the second law firm.

Federal prosecutors have argued that Fowler’s defense can’t simply withdraw from the case without giving some type of explanation.

US Assistant Attorney Greenwood reiterated that argument, telling the judge that “there are significant portions of a fee arrangement that are not potentially privileged.” She suggested Fowler’s attorneys provide details in an ex-parte and then allow the government to access the non-privileged portions “so we can appropriately respond to the motion to withdraw.”

Judge Carter agreed to allow Fowler’s defense team to file a submission under seal. “Once I receive those materials,” he said, “I will make a determination as to whether or not the document will remain under seal or whether or not there are portions that can, in fact, and should, in fact, be redacted and other portions that should be made public.”

The defense counsel said they would submit the document on Nov. 18.

So where is Fowler’s money?

Fowler has been having money problems for a while—problems that extend back to when the US Department of Justice froze his bank accounts in late 2018, leading to the collapse of the Alliance of American Football, a new football league that he cofounded and was a major investor in.

From there, things seem to have gotten worse.

Recall that in January 2020, Fowler rejected a plea deal that would have required him to forfeit $371 million. It was the forfeiture requirements that blew up the deal. Prosecutors hit back with a superseding indictment that added a new count: wire fraud.

On October 15, Law360, reported that Fowler’s legal team might be open to exploring for a second time potential options to resolve the charges, even though the new wire fraud charge complicated things.

And then, on October 23, Fowler’s defense team went to the court seeking to modify conditions of his bond so that he could pay for his defense. (Here is the original May 2019 bond conditions; here is their request for a change.)

Specifically, they wanted to change the bond conditions to enable Fowler to take credit out on properties he had acquired prior to February 2018 “when the alleged conspiracy began” without approval from pretrial services. And to remove the five properties posted as security for the $5 million bond.

Those properties, based on a rough estimate of looking at them on Zillow, are probably only worth around $1.5 million total.

Whatever happened after that — it clearly wasn’t enough to satisfy his attorneys.

Updated Nov. 14 to add the bit about Fowler’s accounts getting frozen in 2018 and the AAF.

Reginald Fowler, the Arizona, businessman allegedly linked to hundreds of million of dollars in missing Crypto Capital funds, is about to lose his defense team. Did he neglect to pay them?

And knowing who their client was, did his lawyers ask for a large enough retainer in the event that something unexpected like, say, a superseding indictment might extend their work?

Crypto Capital is the payment processor that Tether and Bitfinex—and several other cryptocurrency firms—used to shuttle money around the globe as a workaround to the traditional banking system. Fowler allegedly helped out by opening up a network of bank accounts for them.

We can only guess the real reason Fowler’s lawyers are keen to drop their client at the moment, but court docs may offer clues. Here is the backstory:

Earlier this week, Fowler’s attorneys—James McGovern and Michael Hefter of Hogan Lovells US LLP—asked a New York judge for permission to withdraw from the case. (Here is their motion to withdraw filed on Nov. 9.)

(Fowler is also represented by Scott Rosenblum of Rosenblum Schwartz & Fry PC, though Rosenblum’s name is not on the motion.)

The lawyers claim they initially told Fowler their reasons for wanting to quit on February 26—coincidentally, just five days after the government added a fifth charge against Fowler in its superseding indictment and a month after Fowler forfeited on a reasonable sounding plea bargain.

In the months follower, the legal team informed Fowler both “orally and in writing on multiple occasions” of their grounds for wanting to withdraw. Now, after much back and forth, they have had enough: they are asking the court for permission to drop him.

McGovern and Hefter don’t offer a specific reason for wanting to quit in their motion, citing attorney-client privileged. But they argue the case has had “limited pertinent discovery,” Fowler has had ample time to find new counsel, and essentially, the case should go on just fine without them.

Federal prosecutors are not convinced. In a letter addressed to Andrew Carter, the Southern District of New York judge overseeing the case, they argue the defense counsel has’t presented enough facts for the court to decide on the motion. (Here is their response filed on Nov. 12.)

Specifically, they dispute the “limited pertinent discovery” claim, saying the government has so far produced over 370,000 pages of discovery, much of which they have already discussed in detail with the defense counsel.

Further, they argue that if this is about a “fee dispute,” the court needs to weigh other factors, such as “nonprivileged facts” about the fee arrangement, including whether a “more careful or prudent approach to the retainer agreement might have avoided the current problem”—i.e., McGovern and Hefter should have insisted on more money up front.

Finally, they claim that if Fowler’s lawyers’ leaving further delays the trial, the court should not allow it. After two postponements, the trial is currently scheduled for April 12, 2021. (It was originally slated to begin on April 28, 2020, and then got moved to January 11, 2021, before the current trial date.)

“Now, approximately five months before the current trial date, defense counsel seeks to withdraw from this matter based on facts they claim were discussed with the defendant as early as February 26, 2020—nearly nine months ago and before both prior adjournments in this case,” federal prosecutors said. “The current motions should be denied if allowing counsel to withdraw at this late stage would further delay trial.”

The search for what happened to QuadrigaCX’s missing money is a never-ending one.

In the latest twist, Ernst & Young, the trustee in the Canadian crypto exchange’s bankruptcy case, hired an analytics firm to probe the blockchain for additional clues on where it all went.

Miller Thomson, the law firm representing Quadriga’s former users, sent out a letter to Quadriga creditors on Friday, letting them know that on August 17, EY retained Kroll Associates “to conduct further analysis on a subset of transaction data.”

The decision was guided in part by the “official committee,” a subset of Quadriga users who represent the exchange’s former users as a whole. The group has been working with EY since February collecting and reviewing proposals from third-party cryptocurrency asset tracing firms, Miller Thomson said.

Kroll, a division of New York-based financial consultancy firm Duff & Phelps, will not be tackling the project alone, however. It is joining forces with Coinfirm, a London-based blockchain analytics firm.

Kroll will receive up to $50,000 USD for their efforts. And EY has provided a contractual indemnity of up to $150,000 USD—three times the professional fees—to protect Kroll from any lawsuits or negligence claims.

Crypto Capital

In its letter, Miller Thomson also noted that it appears Crypto Capital is not holding any of Quadriga’s money.

Recall that back in January, Miller Thomson reached out to creditors asking for help in identifying if Quadriga had used the Panamanian third-party processor to funnel cash in and out of the exchange.

Crypto Capital is of interest because it is tied to crypto exchange Bitfinex, which is allegedly missing some $850 million. (I guess the hope was that some additional Quadriga money might have been tied up in all of that mess—and there would be more to reclaim.)

Disbursement of funds

So far, EY has located $35 million (CA$46 million ) to pay out to creditors. The amount represents a fraction of the total $190 million (CA$246 million) that went missing when the exchange went belly up early last year.

As of May, EY has received 16,959 claims from the 76,000 or so users who held funds on the exchange when it collapsed.

Two things have to happen before those claims can be filled. The first is that EY has to review each claim individually, and that takes time and money.

But the bigger holdup by far is that the Canada Revenue Agency needs to complete its audit of Quadriga’s tax liabilities, said Miller Thomson.

In March, the CRA collected a vast trove of documents from EY, and there’s no telling how long that will take to dig through, especially given current circumstances.

“The CRA did not confirm a timeline of when the CRA Audit will be completed given the COVID19 pandemic,” the law firm said.

Reginald Fowler stood before a New York judge Thursday and pleaded not guilty to wire fraud. The new charge brought the total counts against him to five. An irked-looking judge agreed to move the trial date, originally set for next month, to Jan. 11. (Court doc.)

The wire fraud charge was added in a superseding indictment on Feb. 21. The Arizona businessman and ex-NFL owner had already pleaded not guilty to the four prior counts, which had to do with bank fraud and illegal money transmitting. He was looking at a trial date of April 28.

However, with the new charge piled on, Fowler’s lawyer James McGovern wanted more time to prepare. Matthew Lee of Inner City Press, live-tweeted Fowler’s arraignment in court today.

“The trial is scheduled. Mr. Fowler did not plead guilty. Now he wants an adjournment of the trial,” said U.S. Attorney Jessica Fender, according to Lee’s account.

Judge Carter granted the adjournment and offered Oct. 28 as a new date for the trial. But Fender turned it down saying her colleague was unavailable at that time.

“Really? A prosecutor not being available is not grounds under the Speedy Trial Act,” said Judge Carter.

Finally, a new date of early next year was settled upon — and the judge appeared irritated with the government, Lee told me.

The law moves slow

Nothing is happening fast in this case. But the right to a speedy trial isn’t for the benefit of the public — it’s for the benefit of the defendant, who can waive it. And since Fowler is free on $5 million bail while he awaits trial, he can afford to do that. After all, he could find himself behind bars for many years after the trial.

Fowler was originally indicted on April 30, 2019, along with Israeli woman Ravid Yosef, who remains at large. The pair allegedly ran a shadow banking service on behalf of Crypto Capital Corp, a Panamanian payment processor that counted Bitfinex and the failed QuadrigaCX cryptocurrency exchanges as customers.

A plea deal would have seen three out of four charges against Fowler dropped. The deal was conditioned upon him forfeiting $371 million* allegedly tied up in some 50 bank accounts, but he wouldn’t—or couldn’t—agree to that.

After Fowler turned down the plea deal, federal prosecutors heaped on the newest charge of wire fraud. The fifth count was no surprise. In a court transcript filed in October 2019, Assistant U.S. Attorney Sebastian Swett told Judge Carter:

“We have told defense counsel that, notwithstanding the plea negotiations, we are still investigating this matter, and, should we not reach a resolution, we will likely supersede with additional charges.”

Fowler, who resides in Chandler, Ariz., will likely go about his daily life until next year when his trial begins. Is he rattled by any of this? Who knows. This is a man who has plenty of experience dealing with lawyers and judges. In 2005, ESPN reported that he had been sued 36 times.

Updated (3/7/20) to add names of attorneys.

*Updated (3/5/20 at 11:30 p.m ET) to note that Fowler’s proposed plea deal was based on him forfeiting $371 million, not $371,000 as previously stated.

A superseding indictment filed with the SDNY court Thursday includes a new charge of wire fraud for ex-Minnesota Viking co-owner Reginald Fowler.

Fowler, who is living in Chandler, Ariz., while free on $5 million in bail, currently faces four other charges related to bank fraud and operating an illegal money transmitting business, so this makes for count number five.

According to federal prosecutors, from June 2018 to February 2019, Fowler obtained money through “false and fraudulent pretenses” to fund a professional sports league in connection with his ownership stake in the league.

What sports league would that be? The indictment does not tell us. But Fowler invested $25 million in the Alliance of American Football — an attempt to form a new football league — right before its inaugural season and shortly before his arrest on April 30, 2019.

The league ran into problems after withdrawals from Fowler’s domestic and foreign accounts were “held up around Christmas,” freezing a principal source of the league’s funding.

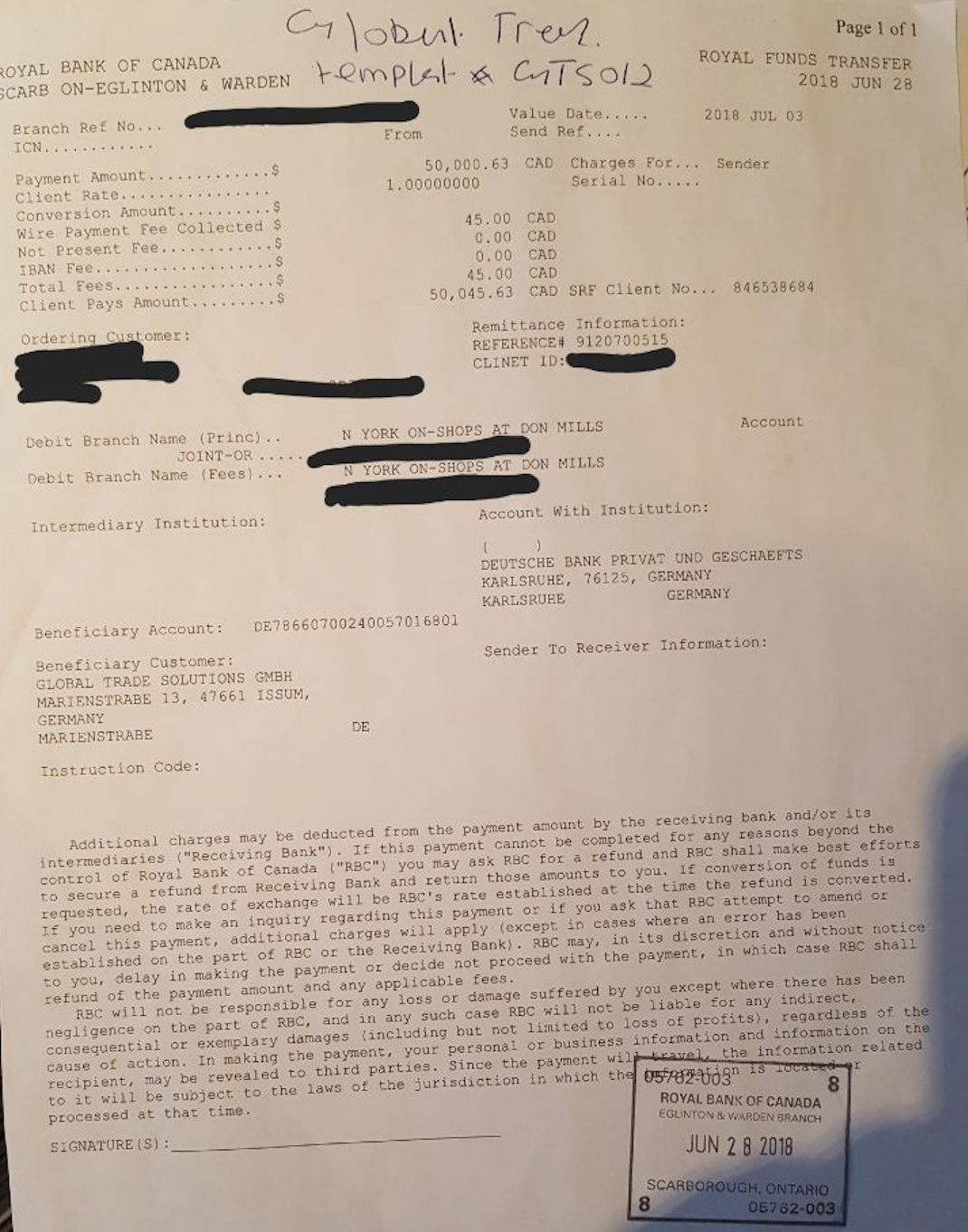

Global Trading Solutions LLC has been directly linked to Crypto Capital Corp., a Panamanian shadow bank used by Bitfinex and the failed Canadian crypto exchange QuadrigaCX.

Due to money problems, the AAF collapsed on April 2, 2019, and filed for Chapter 7 bankruptcy two weeks later. The league claimed assets of $11.3 million and liabilities of $48.3 million and held just $536,160.68 in cash.

After forgoing a plea deal last month, Fowler is set to go trial on all five counts on April 28.

Did you enjoy this story? Support me and my writing by becoming a patron.

Last month, Miller Thomson, the law firm representing Quadriga’s former users, asked creditors for help in identifying if the failed Canadian exchange had used Crypto Capital Corp, a payment processor that is allegedly missing some $850 million.

In a letter posted on its website on Jan. 22, the law firm said that it had received information that Quadriga had used a “Panamanian shadow bank” in the final quarter of its operation—presumably, that means September thru December 2018, since the exchange went belly up in January 2019.

Specifically, the law firm asked creditors to forward any emails or financial statements with names of people or companies linked to Crypto Capital. It offered a lengthy list that included Global Trading Solutions LLC and Global Trade Solutions AG.

The former was a shell company in Chandler, Ariz., set up on Feb. 14, 2018, by Reggie Fowler, one of the individuals alleged to have connections to Crypto Capital. The latter was the Swiss parent company of Crypto Capital. (The firm was cited as a parent company on Crypto Capital’s website.)

Also, in a December 2018 letter published on this blog, Crypto Capital boss Ivan Molina wrote that “Global Trade Solutions AG and related entities” were being denied banking in the U.S., Europe and elsewhere as a result of financial crimes investigations. Molina was arrested for money laundering last year.

What about GTS Germany?

Global Trade Solutions Gmbh is not on Miller Thomson’s list. I can’t find it on any legal or court docs either, but someone posted on Reddit a year ago that they had received their Crypto Capital withdrawals from the company.

Spiral Inc. is a holding company Fowler set up in 1989. At one time it held more than 100 businesses. He also owns Spiral Volleyball.

Links to Quadriga

Two documents recently shared by individuals on Telegram claiming to be Quadriga creditors show funds sent to Global Trade Solutions Gmbh.

On June 28, 2018, one creditor wired $50,000 CAD from the Royal Bank of Canada in Toronto to an account at Deutsche Bank in Germany belonging to Global Trade Solutions Gmbh.

“I should have followed my gut feelings when I was at the bank making this wire transfer,” the user told me. “I just had a very shady feeling.”

Another creditor shared the following document on Telegram. Similarly, it shows funds being sent to a Global Trade Solutions Gmbh account at Deutsche Bank. The transfer appears to be going out from a bank in Toronto, but there is no date on it.

Other evidence

There is other evidence to support Quadriga using Crypto Capital. At one time, the payment processor listed Quadriga on its website as a client. Gerald Cotten, the exchange’s now-deceased founder also admitted to using it in the past.

In an email to Bloomberg News on May 17, 2018, he wrote: “Crypto Capital is one such company that we have/do use. In general it works well, though there are occasionally hiccups.”

Assuming Quadriga did use Crypto Capital, the only question that remains is, was the payment processor holding any Quadriga funds when the exchange went belly up? (Remember, Quadriga didn’t keep any books, so it’s up to Miller Thomson and court-appointed trustee Ernst & Young to piece things together.) And if so, is there any chance in hell of getting those funds back?

Updated on Feb. 19 to add Ralf Hülsmann and link to someone on Reddit who said they received CCC withdrawals via Global Trade Solutions Gmbh.

Updated on Feb. 13 to fix typo — Global Trade Solutions AG, not Global Trading Solutions AG — add a screenshot from Crypto Capital’s website and mention missing $850 million.

Reginald Fowler, the ex-NFL owner arrested in connection with operating a “shadow bank” that processed hundreds of millions of dollars of unregulated transactions on behalf of crypto exchanges, is out on $5 million bail.

The U.S. Government previously argued that Fowler should be detained without bail. The government thought he was too much of a flight risk due to his overseas connections and access to bank accounts around the world. But for the time being, at least, Fowler is a free man, albeit, with restrictions.

Order and letter

The order setting conditions of release was filed with the District Court for the District of Arizona on May 9. A letter of motion, submitted by U.S. Attorney Geoffrey Berman and addressed to Judge Andrew Carter of the District Court of Southern New York, was entered on May 8.

Copies of the letter went to defense attorneys James McGovern and Michael Hefter, partners at Hogan Lovells in New York. Fowler’s arraignment is set for 4:30 p.m. on May 15 at the Southern District Court of New York.

Fowler was arrested in Arizona on April 30. The bond is being posted in New York, because the District of Arizona does not include secured bonds in bail packages.

According to conditions set forth in the bond, Fowler cannot travel outside of the Southern District of New York, the Eastern District of New York, and Arizona. He also had to surrender his travel documents and his passport.

The properties and the wealthy friends

Fowler’s $5 million personal recognizance bond is secured by two unnamed “financially responsible” co-signers and the following properties:

3965 Bayamon Street, Las Vegas, Nevada

8337 Brittany Harbor Drive, Las Vegas, Nevada

4670 Slippery Rock Drive, Fort Worth, Texas

4417 Chaparral Creek Drive, Fort Worth, Texas

8821 Friendswood Drive, Fort Worth, Texas

A quick look on Zillow indicates the properties are cheap investment houses, worth perhaps $1.5 million in total, if that. This would mean that the additional $3.5 million is secured by Fowler’s wealthy friends, whoever they are.

The LLC on the five properties is Eligibility LLC, 4939 Ray Road, #4-349 Chandler, Arizona 85226. The mailing address points to a UPS store, so it is basically a P.O. Box.

Global Trading Solutions LLC, a company linked to Fowler’s shadow banking operation, had the same mailing address for a time, but the address was later changed.

Indictment

On April 11, Fowler and Ravid Yosef, an Israeli woman who lived in Los Angeles and is still at large, were indicted on charges of bank fraud. Fowler was also charged with operating an unlicensed money services business.

Fowler’s company—or one of his companies—was Global Trading Solutions LLC, which provided services for Global Trade Solutions AG, the Switzerland-based parent company of Crypto Capital Corp.

Cryptocurrency exchanges used Crypto Capital as an intermediary to wire cash to their customers. The firm is allegedly withholding $851 million on behalf of Bitfinex, a crypto exchange that is currently being sued by the New York Attorney General.

# # #

Thanks to Nic Weaver for locating the court documents. He spends his beer money on PACER, so you don’t have to.

There is so much going on now with Bitfinex. My eyes are burning and my head hurts from reading piles of court docs. Here is a rundown of all the latest—and then some.

The New York Attorney General (NYAG) is suing Bitfinex and Tether, saying tethers (USDT) are not fully backed—after $850 million funneled through third-party payment processor Crypto Capital has gone missing.

It’s still not clear where all that money went. Bitfinex says the funds were “seized and safeguarded” by government authorities in Portugal, Poland and the U.S. The NYAG says the money was lost. It wants Bitfinex to stop dipping into Tether’s reserves and to handover a mountain of documents.

In response to the NYAG’s ex parte order, Tether general counsel Stuart Hoegner filed an affidavitaccompanied by a motion to vacate from outside counsel Zoe Phillips of Morgan Lewis. Hoegner admits $2.8 billion worth of tethers are only 74% backed, but claims “Tether is not at risk.” Morgan says New York has no jurisdiction over Tether or Bitfinex. Meanwhile, the NYAG has filed an opposition. It wants Bitfinex to stop messing around.

Bitfinex: No one is willing to audit us because they don't want to damage their reputation by auditing us! Asymmetric risk!

New York Attorney General: We'll audit you! For free! Bitfinex: NOT LIKE THIS! New York Attorney General: Send documents. Bitfinex: NO GOD PLEASE NO!

Football businessman Reggie Fowler and “co-conspirator” Ravid Yosef were charged with running a “shadow banking” service for crypto exchanges. This all loops back to Crypto Capital, which Bitfinex and Tether were using to solve their banking woes.

In an odd twist, the cryptocurrency saga is crossing over into the sports world. Fowler was the original main investor in the Alliance of American Football (AAF), an attempt to create a new football league. The league filed for bankruptcy last month—after Fowler was unable to deliver, because the DoJ had frozen his bank accounts last fall.

The US government thinks Fowler is a flight risk and wants him held without bail. The FBI has also found a “Master US Workbook,” detailing the operations of a massive “cryptocurrency scheme.” They found it with email subpoenas, which sounds like it was being kept on a Google Drive?

Yosef is still at large. She appears to have split her time between Tel Aviv and Los Angeles. This is her LinkedIn profile. She works as a relationship coach and looks to be the sister of Crypto Capital’s Oz Yosef (aka “Ozzie Joseph”), who was likely the “Oz” chatting with “Merlin” documented in NYAG’s suit against Bitfinex.

All eyes are on Tether right now. Bloomberg reveals the Commodity and Futures Trading Commission (CFTC) has been investigating whether Tether actually had a stockpile of cash to support the currency. The DoJ is also looking into issues raised by the NYAG.

Meanwhile, bitcoin is selling for a $300 to $400 premium on Bitfinex — a sign that traders are willing to pay more for bitcoin, so they can dump their tethers and get their funds off the exchange. This isn’t the first time we’ve seen this sort of thing. Bitcoin sold at a premium on Mt. Gox and QuadrigaCX before those exchanges collapsed.

Bitfinex is still in the ring, but it needs cash. The exchange is now trying to cover its Tether shortfalls by raising money via—of all things—a token sale. It plans to raise $1 billion in an initial exchange offering (IEO) by selling its LEO token. CoinDesk wrote a story on it, and even linked to my Tether timeline.

It's funny because LEO also means law enforcement organization

Tether wants to move tethers from Omni to the Tron blockchain. Tron planned to offer a 20% incentive to Omni USDT holders to convert to Tron USDT on Huobi and OkEx exchanges. But given the “recent news” about Bitfinex and Tether, it is delaying the rewards program.

Coinbase is bidding adieu to yet another executive. Earn.com founder Balaji Srinivasan, who served as the exchange’s CTO for a year, is leaving. It looks like his departure comes after he served the minimum agreed period with Coinbase.

Elsewhere, BreakerMag is shutting down. The crypto publication had a lot of good stories in its short life, including this unforgettable one by Laurie Penny, who survived a bitcoin cruise to tell about it. David Gerard wrote an obituary for the magazine.

The Los Angeles Ballet is suing MovieCoin, accusing the film finance startup of trying to pay a $200,000 pledge in worthless tokens—you can’t run a ballet on shit coins.

Police in Germany and Finland have shut down two dark markets, Wall Street Market and Valhalla. And a mystery Git ransomware is wiping Git repository commits and replacing them with a ransom note demanding Bitcoin, as this Redditor details.

According to an April 24 court filing, New York State Attorney General Letitia James has alleged that crypto exchange Bitfinex lost $850 million and then tried to pull the wool over people’s eyes by dipping into Tether’s reserves.

Tether issues a dollar-pegged stable coin of the same name. According to the Office of the Attorney General (OAG), Bitfinex has so far siphoned $700 million from Tether funds, meaning that tethers are not fully backed. Given that tether is an essential source of liquidity in the crypto markets—currently, there are 2.8 billion tethers in circulation—this is not good news for bitcoin.

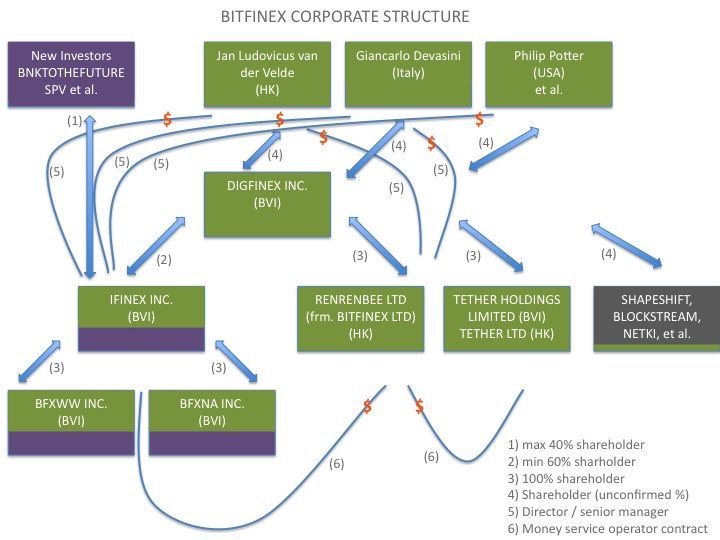

I’ve updated my Bitfinex/Tether timeline to bring you up to speed on the full history of these companies’ past shenanigans. Bitfinex and Tether are operated by the same individuals, and their parent company is Hong Kong-based iFinex. I recommend reading the entire 23-page courtdocument. It reveals a lot about what has been going on under the covers at Tether/Bitfinex. I’ll try and summarize.

What happened

Bitfinex was allowing residents of New York to trade on its platform. This is not supposed to happen. Effective August 8, 2015, any virtual currency company that wants to do business in New York State needs to have a BitLicense. This led the OAG to launch an investigation into Bitfinex and Tether in 2018.

Banking has been an ongoing struggle for Bitfinex since April 2017, when it was cut off by correspondent bank Wells Fargo and its main banks in Taiwan. At different periods, Bitfinex has turned to Puerto Rico’s Noble Bank, Bahamas’ Deltec Bank, and more recently, HSBC via a private account with Global Trading Solutions LLC.

Meanwhile, Bitfinex has had to rely on third-party payment processors to handle customer fiat deposits and withdrawals—a fact that it has never been completely up front about. (In fact, the HSBC account turns out to be part of the shadow banking network set up by its payment processor.)

Since 2014, Bitfinex has sent $1 billion through Panama-based Crypto Capital Corp. Bitfinex also told the OAG that it had used a number of other third-party payment processors, including “various companies owned by Bitfinex/Tether executives,” as well as other “friends of Bitfinex” — meaning human-being friends of Bitfinex employees willing to use their bank accounts to transfer money to Bitfinex clients.

This is basically Bitfinex setting up shell companies and playing cat and mouse with the banks—and it sounds a lot like what Canadian crypto exchange QuadrigaCX was doing before it went belly up in January. (Quadriga also used Crypto Capital, but the payment processor is not holding any Quadriga funds.)

By mid-2018 Bitfinex customers were complaining they were unable to withdraw fiat from the exchange. This is apparently because Crypto Capital, which held “all or almost all” of Bitfinex funds, failed to process customer withdrawal requests. Crypto Capital told Bitfinex that the reason the $850 million could not be returned was because the funds were seized by government authorities in Portugal, Poland and the U.S.

Bitfinex did not believe this explanation. “Based on statements made by counsel for Respondents to AG attorneys… Respondents do not believe Crypto Capital’s representations that the funds have been seized,” the court document states.

(This is not in the court filings but Crypto Capital shared this letter with its customers in December 2018. The letter is from Global Trade Solutions AG, the parent company of Crypto Capital Corp——not to be confused with Global Trading Solutions LLC. The letter states that GTS AG is being denied banking services in the U.S., Europe, and elsewhere “as a result of certain AML and financial crimes investigations” by the FBI and cooperative international law enforcements and/or regulatory agencies.”)

In communication logs from April 2018 to early 2019 shared with the OAG, a senior Bitfinex executive “Merlin” repeatedly beseeched an individual at Crypto Capital, “Oz,” to return funds. Merlin writes: “Please understand, all this could be extremely dangerous for everybody, the entire crypto community. BTC could tank to below $1K if we don’t act quickly.” A Crypto Capital customer, who asked not to be named, told me that Merlin is Bitfinex CFO Giancarlo Devasini.

Borrowing money from Tether

Rather than admit it was insolvent, Bitfinex/Tether tried to cover up the problem. According to the court docs, in November 2018, Tether transferred $625 million in an account at Deltec in the Bahamas to Bitfinex. In return, Bitfinex caused $625 million to be transferred from an account at Crypto Capital to Tether’s Crypto Capital account.

Absolute legendary move here, Bitfinex took $625 million in real money at a real bank from Tether, and in exchange gave Tether back $625 million in fake money at a fake bank. https://t.co/llyRhT4Op2pic.twitter.com/wFPmmOnGVI

Essentially, Bitfinex tries to create the money by doing a one-for-one transfer of real money at Deltec for funds that don’t actually exist at Crypto Capital. Once they realized that this was probably a terrible idea, they re-papered the transfer as a loan.

Bitfinex then borrowed $900 million from its Tether bank accounts. The loan is secured with shares in iFinex stock. In case you didn’t quite follow that, Bitfinex and Tether are basically the same company, so you can think of this as Bitfinex borrowing money from itself—and then backing the loan with shares of itself.

According to the OAG, “The transaction documents were signed on behalf of Bitfinex and Tether by the same two individuals.”

OAG is fed up with the nonsense. It has obtained a court order against iFinex. Under the court order, Bitfinex and Tether are to cease making any claim to the dollar reserves held by Tether. iFinex is also required to turn over documents and information as the OAG continues its probe.

The court has also ordered that iFinex identify all New York and U.S. customers of Bitfinex whose funds were provided to Crypto Capital and the amount of any outstanding funds—and provide a weekly report evidencing any issuance or redemption of tethers.

Bitfinex responds

Bitfinex has issued a response (archive), stating that the OAG court filings “were written in bad faith and are riddled with false assertions.” It claims the $850 million are not lost but have been “seized and safeguarded.”

The exchange continues to deny any problem. It writes:

“Both Bitfinex and Tether are financially strong—full stop. And both Bitfinex and Tether are committed to fighting this gross overreach by the New York Attorney General’s office against companies that are good corporate citizens and strong supporters of law enforcement.”

What does this mean?

It means Bitfinex is in real trouble. The New York’s Attorney General is one of the most powerful in the nation. That should worry Bitfinex.

New York law allows the AG to seek restitution and damages. On top of that, there is also the Martin Act, a 1921 statute designed to protect investors. The Act vests the attorney general with wide-ranging enforcement powers. Under the Act, the attorney general can issue subpoenas to compel attendance of witnesses and production of documents. Those called in for questioning do not have a right to counsel.

The attorney general‘s decision to conduct an investigation is not reviewable by courts. As Stephen Palley, partner at Anderson Kill, points out, the iFinex action arises out of a Martin Act investigation and “Violations of the Martin Act can be civil and criminal.”

The Martin Act is a New York law that gives the N.Y. Attorney General very broad power to investigate securities fraud.

Violations of the Martin Act can be civil and criminal.

The New York A.G.' Tether/Bitfinex action arises out of a Martin Act investigation. pic.twitter.com/VsDgDcEjw8

Finally, if $850 million is really missing, not just stuck somewhere, Bitcoin is in real trouble, too. Tether could lose its peg and drop substantially below $1. Remarkably, tether’s peg seems to be holding steady now.

Since the news broke, the price of bitcoin has dropped several hundred dollars. A valiant effort is being made to pump the price back up, and it’s working, sort of—for now.

I originally wrote this article in January 2019. It is based off an earlier story that I wrote for Bitcoin Magazine in February 2018.

This timeline only goes up until May 2021; however, it documents all of the early shenanigans of Bitfinex and Tether.

Stablecoins—virtual currencies pegged to another asset, usually, the U.S. dollar—bring liquidity to crypto exchanges, especially those that lack ties to traditional banking. Putting it simply, if you are a crypto exchange and you don’t have access to real dollars, stablecoins are the next best thing.

Today, there are several stablecoins to choose from. But by far the most popular and widely traded is tether (USDT), issued by a company of the same name. Of the three or four main stablecoin models, Tether follows the I.O.U. model, where virtual coins are supposed to represent actual money and be redeemable at any time. It all sounds well and good, but for one thing: There is no evidence to suggest Tether is fully backed.

Currently, there are 1.9 billion tethers in circulation.* That means, there should be a corresponding $1.9 billion tucked away in one or more bank accounts somewhere. Bitfinex, the crypto exchange closely linked to Tether, claims the money exists, but has yet to provide an official audit to support those claims. (We have seen snapshots of bank account balances at certain points in time, but these are not full audits.)

*As of May 2025, there are 149 billion tethers in circulation, according to Tether’s Transparency page.

More troubling, the issuance of tethers correlates with the rapid run up in price of bitcoin from April to December 2017 when bitcoin peaked at nearly $20,000. If authorities were to step in and freeze the bank accounts underlying tether, it is hard to guess what impact that could have on crypto markets at large.

A timeline of events reveals a full picture of the controversy surrounding Tether and Bitfinex.

Timeline

2012 — iFinex Inc., the company that is to become the parent company of Bitfinex and Tether, is founded in Hong Kong. (Like its parent company DigFinex, iFinex is registered in the British Virgin Islands. An org chart from NY AG court filings is here.)

2013 — Bitfinex incorporates in Hong Kong. The cryptocurrency exchange is run by the triad: Chief Strategy Officer Phil Potter, CEO Jan Ludovicus van der Velde and CFO Giancarlo Devasini.

July 9, 2014— Brock Pierce, Bitcoin Foundation director and former Disney child actor, launches Realcoin, a dollar-backed stablecoin. Realcoin is built on a Bitcoin second-layer protocol called Mastercoin, now Omni. Pierce was one of the founding members of the Mastercoin Foundation before resigning in July 2014. He founded Realcoin along with Mastercoin CTO Craig Sellars and ad-industry entrepreneur Reeve Collins. (Wall Street Journal)

September 5, 2014—Appleby, an offshore law firm, assists Bitfinex operators Potter and Devasini in setting up Tether Holdings Limited in the British Virgin Islands, according to the Paradise Papers. (Offshore Leaks Database)

September 8, 2014 — Tether Limited registers in Hong Kong.

October 6, 2014 — The very first tethers are minted, according to the Omni block explorer.

November 20, 2014 — Realcoin rebrands as “Tether” and officially launches in private beta. The company hides its full relationship with Bitfinex. A press release lists Bitfinex as a “partner.” In explaining the name change, project co-founder Reeve Collins tells CoinDesk the firm wanted to avoid association with altcoins.

January 15, 2015 — Bitfinex enables trading of tether on their platform.* (Bitfinex blog.Archive.)

May 18, 2015 — Tether issues 200,000 tethers, bringing the total supply to 450,000.

May 22, 2015— Bitfinex is hit with its first hack. The exchange claims it lost 1,500 bitcoin (worth $400,000 at the time) when its hot wallets were breached. The amount represents 0.05 percent of the company’s total holdings. Bitfinex says it will absorb the losses.

December 1, 2015 — Tether issues 500,000 USDT, bringing the total supply to 950,000. (The price of bitcoin has remained stable throughout most of 2015, but climbs from $250 in October to about $460 in December.)

June 2, 2016— The U.S. Commodity Futures Trading Commission fines Bitfinex $75,000 for offering illegal off-exchange financed retail commodity transactions in bitcoin and other cryptocurrencies and for failing to register as a futures commission merchant as required by the Commodity Exchange Act. In response, Bitfinex moves its crypto funds from an omnibus account to multisignature wallets protected by BitGo.

August 2, 2016 —Bitfinex claims it has been hacked again when 119,756 BTC, worth $72 million at the time, vanish. This is one of the largest hacks in bitcoin’s history, second only to Mt. Gox, a Tokyo exchange that lost 650,000 BTC in 2014. Bitfinex never reveals the full details of the breach. (Chapter 8 of David Gerard’s book “Attack of the 50-Foot Blockchain” offers an in-depth explanation of the hack.)

August 6, 2016— Bitfinex is unable to absorb the losses of the hack. The exchange announces a 36% haircut across the board for its customers. It even takes funds from those who were not holding any bitcoin at the time of the hack. In return, customers receive an I.O.U. in the form of BFX tokens, valued at $1 each.

One large U.S. customer reportedly didn’t get the full haircut. “Coinbase, got a better deal after threatening to sue, multiple sources told me,” said NYT’s Nathaniel Popper.

One point that didn't fit in the story: After getting hacked in 2016, Bitfinex said it gave every customer a 36% haircut to cover losses. But at least one customer, Coinbase, got a better deal after threatening to sue, multiple sources told me.

August 10, 2016 — After having been shut down for a week after the heist, Bitfinex resumes trading and withdrawals on its platform. Meanwhile, Zane Tacket, the exchange’s community director, announces on Reddit (archive) that Bitfinex is offering a bounty of 5% (worth up to $3.6 million) for any information leading to the recovery of the stolen funds.

August 17, 2016— Bitfinex announces it is engaging Ledger Labs, a blockchain forensic firm founded by Ethereum creator Vitalik Buterin, to investigate its recent breach. Bitfinex hires Ledger to do a computer security audit, but leads customers into believing that Ledger is also going to perform a financial audit. A financial audit is key to knowing whether Bitfinex was even solvent at the time of the hack.

“We are also in the process of engaging Ledger Labs to perform an audit of our complete balance sheet for both cryptocurrency and fiat assets and liabilities,” Bitfinex says in a blog post (archive).

A footnote added to the blog post on April 5, 2017, makes a correction: “Ledger Labs has not been engaged to perform a financial audit of Bitfinex. When in initial discussions with Ledger Labs in August 2016, we had initially understood that they could offer this service to us.” The exchange goes on to say that it is in the process of engaging a third-party accounting firm to audit its balance sheet.

This audit, as we are to learn, never happens.

October 12, 2016 — Bitfinex tries to reach out to the hacker. In a blog post (archive), titled “Message to the individual responsible for the Bitfinex security incident of August 2, 2016,” the firm writes: “We would like to have the opportunity to securely communicate with you. It might be possible to reach a mutually agreeable arrangement in exchange for an enormous bug bounty.”

October 13, 2016 — Bitfinex announces (archive) that its largest BFX token holders have agreed to exchange over 20 million BFX tokens for equity shares of iFinex, the exchange’s parent company. Many Bitfinex customers accept the offer, having already watched BFX tokens drop far below $1. One Redditor even reported the price dropping to $0.30.

As a way to incentivize BFX holders to convert, Bitfinex creates yet another new token: a tradable Recovery Rights Token (RRT). According to the exchange, if any of the stolen bitcoins are recovered, any excess of funds after all BFX tokens have been redeemed will be distributed to RRT token holders.

If you convert your BFX to iFinex shares before October 7, you get one RRT for each BFX token converted. If you convert between Oct. 8 and Nov. 1, you get half an RRT for each BFX token converted. After that, you get 1/4 of an RRT per BFX token converted. No further RTTs are given after November 30.

December 31, 2016 — In 2016, Tether issued 6 million USDT, six times what it issued the prior year.

March 31, 2017— Correspondent bank Wells Fargo cuts off services to Bitfinex and Tether, according to court documents in a lawsuit that Bitfinex later files. Bitfinex is not a direct customer of Wells Fargo, but rather a customer of four Taiwan-based banks that use Wells Fargo as an intermediate to facilitate wire transfers.

April 3, 2017 — In a blog post(archive), Bitfinex announces plans to redeem any outstanding BFX tokens. “After these redemptions, no BFX tokens will remain outstanding; they will all be destroyed.”

Meanwhile, Potter reveals in an audio that all of the remaining BFX tokens have been converted to tethers. In a nutshell, this means that none of the victims of the August 2016 Bitfinex hack got back any of their original funds—they were all compensated with BFX tokens, RRT tokens and USDT.

April 5, 2017 — Two days after announcing that it had “paid off” all its debt to customers, Bitfinex, via law firm Steptoe & Johnson, files a lawsuit against Wells Fargo for interrupting its wire transfers. Tether Limited is listed as a plaintiff. In addition to an injunction order, Bitfinex seeks more than $75,000 in damages. (See here for a complete list of documents associated with the lawsuit.)

April 10, 2017— A pseudonymous character known as “Bitfinex’ed” debuts online. In a relentless series of tweets, he accuses Bitfinex of minting tethers out of thin air to pay off debts. At this point, the number of USDT in circulation is 55 million, and BTC’s price has begun a steep ascent that will continue to the end of the year.

April 11, 2017 — Bitfinex withdraws its lawsuit against Wells Fargo. In an audio, Potter admits the lawsuit was frivolous, stating the company was only hoping to “buy time.”

April 17, 2017 — Following a notice about wire delays, Bitfinex announces (archive) it has been shut off by its four main Taiwanese banks: Hwatai Commercial Bank, KGI Bank, First Commercial Bank, and Taishin Bank. Bitfinex is now left to shuffle money between a series of banks in other countries without telling its customers where it is keeping its reserves.

In an audio, Bitfinex CSO Phil Potter tries to calm customers by telling them that Bitfinex effectively deals with this sort of thing by setting up shell accounts and tricking banks.

“We’ve had banking hiccups in the past, we’ve just always been able to route around it or deal with it, open up new accounts, or what have you…shift to a new corporate entity, lots of cat and mouse tricks.”

Around this time, Bitfinex begins to rely increasingly upon Crypto Capital Corp, a Panamanian shadow bank, to shuffle funds around the globe—but it does not make this clear to customers. Also, Bitfinex never engages in a formal contract with Crypto Capital, according to later court documents.

April 24, 2017 — Amidst reports that Bitfinex has lost its banking, USDT temporarily dips to $0.91.

May 5, 2017— After finally clarifying (archive) to customers that it only engaged Ledger Labs for a security audit—not a financial audit—Bitfinex hires accounting firm Friedman LLP to complete a comprehensive balance sheet audit. “A third-party audit is important to all Bitfinex stakeholders, and we’re thrilled that Friedman will be helping us achieve this goal,” Bitfinex writes in a blog post (archive).

June 21, 2017 —The Omni foundation and Charlie Lee announce that tether will soon be issued on the Omni layer of Litecoin, but apparently it never panned out, according to Lee. (Omni Blog, archive)

"Tether will be issuing USDT on Omni on Litecoin 😀"

Launching tether (or anything) on Litecoin requires no approval or corporation from me. I was informed of their decision and I supported it. But I didn't do any work on it. Ultimately, it didn't pan out. I don't have inside info on tether.

August 5, 2017 — Bitfinex’ed publishes his first blog post titled: “Meet ‘Spoofy.’ How a Single Entity Dominates the Price of Bitcoin.” The post explains how an illegal form of market manipulation known as spoofing works. The post includes a video showing a Bitfinex trader putting up a large order of BTC just long enough to push up the price of bitcoin, before canceling the order.

(This is not the first time a crypto exchange has manipulated the price of bitcoin. Mt. Gox, a Tokyo exchange that handled 70% of all global bitcoin transactions before its 2014 collapse, also manipulated its markets. Former Mt. Gox CEO Mark Karpeles admitted in court to operating a “Willy Bot.” An academic paper titled “The Willy Report” shows how the bots were responsible for much of bitcoin’s 2013 price rise.)

September 11, 2017 — Tether announces they will begin making ERC-20 tokens for US dollars and euros on the Ethereum blockchain. (Ethfinex blog,archive)

September 15, 2017 —In the summer of 2017, rumors were afoot that tethers were not fully backed. To quash those rumors, Tether and Bitfinex arrange for accounting firm Friedman LLP to perform an attestation on September 15, 2017.

In the morning, Tether opens an account at Noble Bank. And Bitfinex transfers $382 million from Bitfinex’s account at Noble Bank into Tether’s account at Noble Bank. Friedman conducts its verification of Tether’s assets that evening.

“No one reviewing Tether’s representations would have reasonably understood that the $382,064,782 listed as cash reserves for tethers had only been placed in Tether’s account as of the very morning that Friedman verified the bank balance,” the NY attorney general wrote in its later findings.

The attestation included $61 million held at the Bank of Montreal in an a trust account controlled by Tether and Bitfinex’s general counsel Stuart Hoegner.

September 28, 2017 — Friedman LLP issues a report alleging that Tether’s U.S. dollar balances ($443 million) match the amount of tethers in circulation at the time. Falling far short of a full audit, the report does not disclose the names or locations of banks.