- By Amy Castor and David Gerard

- If you like our work, please do sign up for our Patreons — here’s Amy’s, and here’s David’s.

Bitcoin mining is a highly lucrative business as long as the price of bitcoin keeps going up — and as long as investors believe it will keep going up.

When the price crashes — and the price of bitcoin has halved since the start of the year — crypto miners face margin calls, they have to dump their bitcoins, and reality comes knocking.

In this post, we outline some of the biggest problems facing North American bitcoin miners:

- Miners are nothing like as profitable as they report to the public stock markets that they are.

- Miners don’t want to sell their freshly mined bitcoins, as this would risk crashing the price of bitcoin — so instead, they borrow against the bitcoins, and against their rigs, too!

- This business model only works if number goes up forever.

- Number doesn’t go up forever.

During the bitcoin bubble of 2021, miners wanted to lure in naïve investors from the capital markets who thought that crypto mining companies were a great way to get exposure to bitcoin — without the risk of actually touching a bitcoin. The miners would hold their bitcoins, subsidize their business with debt, and you could just buy their stock!

So the bitcoin miners promoted themselves as enthusiastic bitcoin “to the moon” boys — in the hope of luring in other prospective moon boys. Buy now and watch your profits soar! Number can’t go down!

The cunning plan

Bitcoin miners used to be ruthless economic agents, in it for the money. They knew how volatile crypto was, so they sold their coins as soon as they mined them to cover power bills and other business expenses.

As some point, miners’ business model changed from selling bitcoin to holding bitcoin — and borrowing against it.

This model doesn’t make any sense unless you first assume that the number will never go down, and that the bitcoin bubble will never burst — even though bubbles always burst.

The change started in mid-2021 when bitcoin miners were kicked out of China. Most eventually settled in the US and Canada — because these countries had the world’s next-cheapest reliable electricity.

The US is now the world’s largest bitcoin mining hub, making up about 37% of the global hash rate. [CBECI]

North American miners filed to become publicly-traded companies. Marathon Digital Holdings (MARA) and Riot Blockchain (RIOT) were the first to be listed on Nasdaq. Other miners soon followed. [Investopedia; Compass Mining]

Going public gave the miners access to the mainstream capital markets, investors, and new lines of credit — way more financial resources than they’d ever had before.

The miners marketed themselves to capital markets as massive bitcoin enthusiasts. Get in, this is the magical future! Here’s Whit Gibbs from Compass Mining in January 2022: [CoinDesk]

“With ample access to funding and investors pouring in money, miners didn’t have to sell their bitcoin to fund operational costs, said Compass Mining’s CEO Whit Gibbs. ‘And since miners are incredibly bullish on bitcoin, this allows them to do what they want to do naturally, which is to speculate on bitcoin’s positive price appreciation,’ he added.”

Miners spent mid-2021 onward racking up debt to finance the construction of facilities, buy mining equipment, and pay their executives enormous salaries.

The companies’ operating expenses were paid for by borrowing against their freshly-mined bitcoins. Some loans even used mining rigs as the collateral.

The miners also did accounting tricks, such as depreciating mining rigs over five years — and not the 15 months they should have — to make the companies look like better investments. Meanwhile, their executives were paid well beyond the carrying capacity of the companies.

In 2021, outgoing Marathon CEO Merrick Okamoto earned a shocking $220 million — although most of that was awarded in stock. Riot Blockchain’s top five execs collectively were paid $90 million the same year with a net loss. [SEC; SEC]

Riot Blockchain failed its say-on-pay shareholder vote on executive compensation for 2021. It’s an advisory vote that the company doesn’t have to act on — but it’s an embarrassing thing to have to admit publicly to failing. Thankfully, coiners have no capacity for embarrassment. [SEC]

Bitcoin loans

While the price of bitcoin was going up through 2021, mining saw profit margins as high as 90%. Bitcoin hit $64,000 in April 2021 and $69,000 in November 2021. [Bloomberg, archive]

Margins on mining were especially good in 2021 because the supply of state-of-the art mining rigs was constrained due to the worldwide chip shortage. If everyone could get rigs, the margins would go away.

But by 2022, when bitcoin lost 70% of its price from its November high, it was a different story.

Miners need actual money to pay their operating expenses. Energy can account for as much as 90-95% of a miner’s overheads. Power companies don’t take bitcoins or tethers. But the crypto trading system was running low on naïve retail suckers to supply fresh dollars. [Reuters]

So the miners needed to do their part in propping up the price of bitcoin. Their solution was to avoid selling their bitcoins, and instead to hold them and use them as collateral against low-interest loans.

Marathon had started the fashion of borrowing against mined bitcoins as early as October 2020 — and the other mining companies soon followed the same plan.

Mainstream financial institutions didn’t really get into lending to bitcoin miners. The main lenders to miners were their fellow crypto companies: Galaxy Digital, NYDIG, BlockFi, Foundry Networks, Silvergate Bank [SEC], Celsius Network, and Babel Finance. (Note that Celsius is bankrupt, and Babel has suspended withdrawals.)

In fact, Marathon just entered a new $100 million revolving loan with Silvergate to add to their existing $100 million line of credit from Silvergate. This is while Marathon has thousands of mining rigs lying idle, waiting on a deal for cheap electricity. [SEC; CoinDesk]

Bitcoin miners are also trying to hedge against the downturn by betting against the bitcoin price going back up. Marathon has been selling call options at, say, $50,000. If bitcoin doesn’t hit this price, those options expire worthless. [Bloomberg]

Miners did deals with politicians and the power industry to get cheap electricity in Texas, as low as 2.5c/kWh — the sort of prices that miners were paying in China. [Bloomberg; press release]

But the Texas grid is notoriously unreliable — and can’t fall back on the other two continental US national grids. With 2022’s summer heat, electricity usage went up significantly, and ERCOT has told miners to switch off from time to time. [Bloomberg; Washington Post; The Verge]

Some miners, such as Riot, made money from credits for not using power in this time. [press release]

Margin calls

Borrowed money, one day, needs to be paid back. When the collateral dropped in value, miners’ loans got margin-called. They had to dump some of their vast holdings.

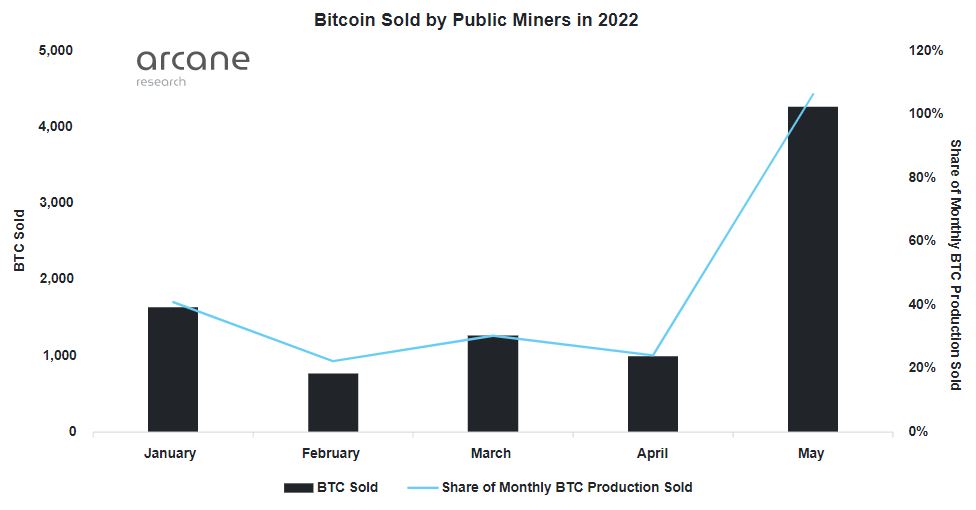

Miners started dumping big time in June 2022, some selling all their mined bitcoins and some of their “stockpile.” Bitfarms dumped 3,000 coins — half its stockpile — in mid-June. A month later, miners collectively sold 14,000 bitcoins, with a face value of roughly $300 million, in a single 24-hour period — when the CeFi crash was in full swing. [Reuters; Bloomberg; Cryptoslate]

Compass Mining — which sells people mining machines that are then hosted in third-party facilities — posted a list of publicly-listed miners in North America who were selling off their stashes. [Compass Mining]

Arcane Research’s Jaran Mellerud analyzed the cash flows and balance sheets of public miners. Marathon was the weakest: “Marathon has 6.2 times higher remaining machine payments in 2022 than their accumulated current operating cash flow accumulated out the year. This will drain them of liquidity.” He thinks Marathon will be forced to sell off their bitcoin stockpile as well. [Tweet thread; Arcane report]

Some loans even used mining hardware as collateral. But mining rigs are even worse collateral than bitcoins. The price of mining rigs on the second-hand market is extremely sensitive to the price of bitcoin — and those loans are now undercollateralized.

As of June 2022, almost $4 billion in loans to bitcoin miners are coming under stress, posing a risk to crypto lenders, as many of the rigs posed as collateral have halved in value. [Bloomberg, archive]

Miners still hold huge piles of unsaleable bitcoins. CryptoQuant says that miners’ holdings have been increasing. As of July 2022, miners held 1,856,000 BTC. [CoinTelegraph]

Mining accounting

Bitcoin miners are not as profitable as they’ve been reporting.

Paul Butler points out that bitcoin mining companies are using questionable accounting methods. [blog post]

When you buy capital equipment with a lifetime longer than your financial year, you can allocate the cost of the purchase over its expected useful lifetime, rather than all in one hit. This is called depreciation.

Publicly-traded mining companies typically depreciate their assets over five years — but the equipment is good for about fourteen to fifteen months, and it’s most profitable in its first nine months. Bitcoin miners play on their “success” in the early years to raise capital to buy additional mining rigs.

The excessively long depreciation on mining rigs is a way to hide that the miners’ real costs are much higher than they’re reporting. The miners are not putting away money for future equipment. This is as well as overpaying their executives.

Tick … tock. Next block?

In a bubble, you can sell mined bitcoins for far more than the cost of the electricity to play Extreme Bingo trying to guess a winning hash.

You can even run old mining rigs that might otherwise be scrapped. Old rigs might spend $30,000 to mine a bitcoin — but that’s fine if you can then sell that bitcoin for $40,000.

So what happens when the bitcoin price drops too low for mining to be profitable?

We’re seeing this now. Miners are taking inefficient hardware offline, causing visible drops in the hash rate charts since May 2022. In November 2018, the price of bitcoin dropped below $3,800 and a lot of miners threw out all their old equipment. The hash rate dipped noticeably.

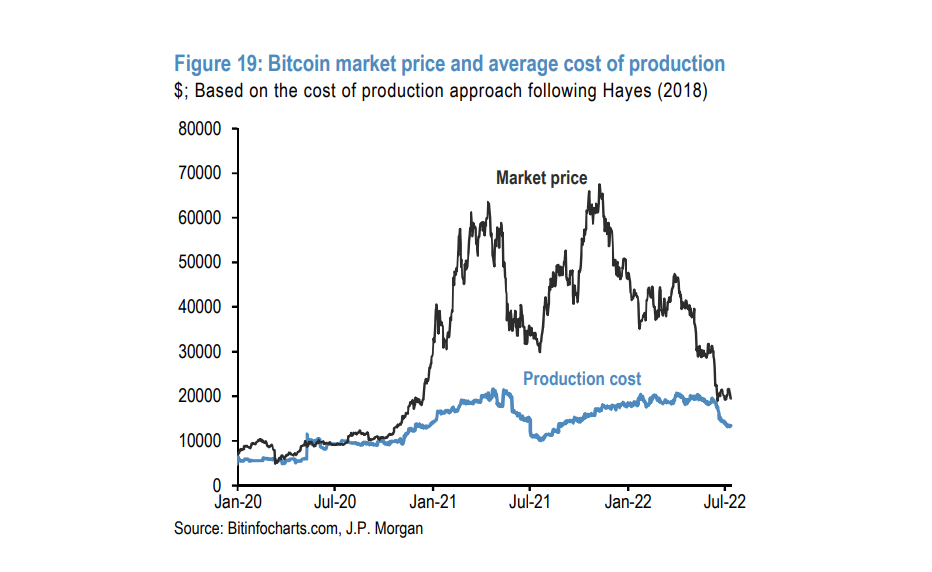

The real trouble starts when bitcoin falls below $15,000. (As we write this, bitcoin is around $23,000.) Break-even for the most efficient machines is somewhere between $9,000 and $11,000, based on an electricity cost of 5c/kWh. In June 2022, JPMorgan put the cost of mining at $13,000 per bitcoin. [Bloomberg]

If the price drops too low, will the bitcoin blockchain stop ticking along? Probably not — bitcoin really doesn’t need much mining to keep running.

There was a slowdown on the bitcoin (BTC) blockchain in late 2017, when bitcoin cash (BCH) — a fork of not just the bitcoin software, but also its full transaction history — was trying to compete to become the official version of bitcoin. Large miners such as Bitmain switched a large proportion of their mining pools to the BCH chain.

The BTC chain took an hour between blocks at times in November 2017 — about 15% of the previous hash power.

Hardly anyone noticed — they were too busy having fun on the exchanges, which is where the action was in the 2017 bubble. Nobody really cares about the blockchain itself.

Bitcoin mining is green, actually

LOL, no it isn’t.

Proof-of-work mining has long been cryptocurrency’s biggest public relations battle, especially since Elon Musk — formerly the avatar of energy transition — bought bitcoins for Tesla in February 2021.

The general public thinks of crypto as nerd money for nerds to rip each other off. But when the public hear about proof-of-work crypto mining, and how it consumes an entire country’s worth of electricity, they get angry.

So it’s extremely important for the crypto industry to pretend as hard as possible that bitcoin mining isn’t as stupidly and egregiously wasteful as it obviously is — so that they’re allowed to keep mining at all.

The Bitcoin Mining Council claims that bitcoin uses 0.16% of all the electricity in the world. The BMC also claims that 58.4% of bitcoin mining energy use is from sustainable sources, based on claims by its members. [BMC, PDF]

Neither of these numbers is true — and BMC doesn’t show its working. Sources that do show their working — and don’t have a financial interest in fudging their numbers — put the sustainable energy percentage at 25.1%, and the percentage of the world’s electricity consumption over 0.5%. [Joule, paywalled; Digiconomist]

We’re also boggling that the BMC calls 0.16% of all the electricity in the world “negligible” — for the most inefficient payment network in human history. Even Christmas tree lights are more useful to humanity.

You’d almost think that coiners will say any bizarre and egregious nonsense if only it lets them keep trading their magic beans.

What happens next?

Number goes down, loans get margin-called, and the mining companies go broke because of a market downturn.

We expect the mining companies to blame everyone else they possibly can — the CeFi companies for crashing the market, bitcoin for just refusing to go up forever. They have to, really.

Bitcoin mining stocks are already down — MARA is down 58% year-to-date, RIOT is down 75%, and Core Scientific (CORZ) is down 74% since the beginning of the year. Meanwhile, crypto stock short sellers were up 126% as of June. [Reuters]

This scheme was never a sustainable business model. But none of these guys are long-term planners. So we don’t expect they had a coherent exit plan either.

The crypto companies who lent dollars to the miners should have been sufficiently capable of joined-up thinking to realize this was never a sustainable business model. Somehow, they didn’t.

But then, for an example of the forward thinking skills of crypto guys, we remind you that Michael Novogratz of Galaxy Digital — one of the big lenders to miners — got a Terra-Luna tattoo in January 2022. [Twitter]

Those loans are never getting paid off. The mining rigs are near-worthless, and the bitcoins held as collateral can’t be dumped without taking the market down even further. The lenders get to take a bath on this one.

The bitcoins will likely be dumped, putting more sell pressure on the price of bitcoin.

Along with the rest of the crypto collapse, this is thankfully isolated within crypto. The only “real” financial institution involved is Silvergate, and they have almost no non-crypto customers these days. Any hit to Silvergate is unlikely to be contagious.

Of course, the investors can always sue the bankrupt corpses of the mining companies.

{kind=link}

Brilliant!

The mining industry for Bitcoin is not creating wealth to the world. It’s the opposite. It drains the worlds energi resourses in a process to produse an articial asset with no real value. This is to stupid and can’t continue much longer.

Amazing work and thanks for telling the truth.

This is the kind of investigative journalism that FORBES and FORTUNE should be doing, instead of pandering to the CryptoLobby – their articles and features are evidence of this and only the most naïve would be fooled into believing otherwise

Can’t wait for this nonsense to finally bite the dust. Snake oil finance at it’s finest.

It’s already been bit — then venom is spreading

These bankruptcy proceedings take a long time, but I’ll be very curious to learn what the examiner uncovers in the Celsius case!

I attended the GCPA fall 2022 conference; a Texas state congress-lady noted that the cryptomining companies in Texas made more money selling electricity than cryptomining. This isn’t so hard to believe: Texas is a fully market grid. Texas wholesale electricity prices averaged $0.022 per kWh in 2020, so a $0.03 to $0.05 long term pricing agreement is very possible.

In contrast, peak pricing during 2021 Uri went up to $0.90 / kWh = system max price limit set by ERCOT.

So a spread between $0.03 – $0.05 purchase price vs. $0.25 to $0.40 is very possible, especially since Texas set a series of peak electricity demand records this past summer.

thanks for writing this up!