Crypto contagion

The price of Bitcoin has bobbled along above $20,000 since mid-June. There seems to be serious interest in keeping it above that number!

Sam Bankman-Fried has been playing the J. Pierpont Morgan of crypto, rescuing sinking companies with hundreds of millions of dollars in crypto assets. His companies FTX and Alameda have so far bailed out Voyager Digital and BlockFi. He says he’s got a few billion left to keep other crypto companies from slipping into the dark abyss of liquidation. [Financial Post]

All Bankman-Fried can do is buy time. The entire cryptosystem is imploding. People are finally realizing that most of the money they thought they had in crypto was imaginary. You didn’t lose money in the crash — you lost your money when you bought crypto.

We’ve been busy keeping up with the fallout, and mining comedy gold. Who thought staying poor would be this much fun? It was nice of the coiners to suggest it.

The liquidation of Three Arrows Capital

Three Arrows Capital (3AC) went into liquidation as of June 27. Two applications were filed in the British Virgin Islands (BVI) where 3AC is incorporated — one by 3AC themselves, and the other, a provisional liquidation, by 3AC creditor Deribit. [LinkedIn]

In a liquidation, a liquidator is appointed to tally up all the assets of a company and distribute them to creditors. It’s the end of the company. Provisional liquidation is not quite the end yet — it’s like bankruptcy protection, even though you know the company is probably insolvent. Wassielawyer has a great thread explaining all this. [Twitter thread]

Why would 3AC petition to liquidate themselves? CEO Zhu Su has shamelessly listed himself as a creditor in the liquidation!

Teneo is the court-appointed liquidator. They’ll be assessing the assets and the claims against the company and its directors.

The liquidators are able to convert any crypto assets into US dollars. This could mean a few billion dollars worth of bitcoin getting dumped any day now — or maybe not, if 3AC’s own bitcoin wallets turn out to be empty.

Less than a week later, 3AC filed for Chapter 15 bankruptcy in the US on July 1. 3AC’s assets are (likely) not in BVI, but in the US and Singapore. Chapter 15 allows the BVI court to be recognized in the US — and protects US assets during the liquidation process. [Bloomberg, archive; bankruptcy filing, PDF]

According to its bankruptcy filing, 3AC had $3 billion under management in April 2022. Analytics firm Nansen reported the company held $10 billion in assets in March. Money disappears fast in crypto land! [Bloomberg]

Also according to the filing — and we’re sure this is fine! — 3AC’s two founders have gone missing: “Mr. Davies and Mr. Zhu’s current location remains unknown. They are rumored to have left Singapore.”

The last we heard from Zhu Su on Twitter was a vague tweet on June 14 — “We are in the process of communicating with relevant parties and fully committed to working this out” — a month after the Terra Luna collapse, which set this entire cascade of dominoes falling. [Twitter]

Zhu is currently trying to offload a bungalow in Singapore that he bought in December for SGD$48.8 million (USD$35 million). The house is held in his son’s trust. [Bloomberg]

Fatmanterra (who is pretty on the ball) says he heard Zhu is planning to transfer the funds from the sale of the bungalow to a bank account in Dubai and has no intention of paying creditors with the proceeds. [Twitter]

3AC has other troubles, such as a probe by Singapore’s central bank. The Monetary Authority of Singapore said that 3AC provided them with false information, failed to meet regulatory requirements when moving fund management to the BVI, and ignored limits on assets under management. They weren’t supposed to manage more than SGD$250 million (about $178 million). [MAS press release, PDF; Blockworks]

Oh, look! 3AC’s money has an over-the-counter trading desk: Tai Ping Shan (TPS) Capital. 3AC seems to have a bunch of money sheltered in this entity, and TPS is still trading despite the liquidation order! Sources told Coindesk that TPS was “where the action was” for 3AC, and where most of 3AC’s treasury is held and traded.

TPS insists it’s completely independent of 3AC, even though Zhu and Davies of 3AC are still part-owners, and the companies have long had multiple links. [CoinDesk; Twitter; CoinDesk]

Peckshield noticed that on 4 July, 3AC transferred $30 million in stablecoins to Kucoin — 10 million USDT and 20 million USDC. This is after the firm was ordered to liquidate. [Twitter]

Rumor has it that 3AC also looked to crypto whales for loans. [Twitter]

3AC also owns a bunch of NFTs — because we all know that NFTs are a great investment and very liquid. [Twitter]

Big plans for Voyager Digital (in bankruptcy)

Less than a week after crypto lender Voyager halted withdrawals, the company filed for Chapter 11 bankruptcy protection in New York on July 5. [Filing; press release; Ehrlich Twitter thread; FT]

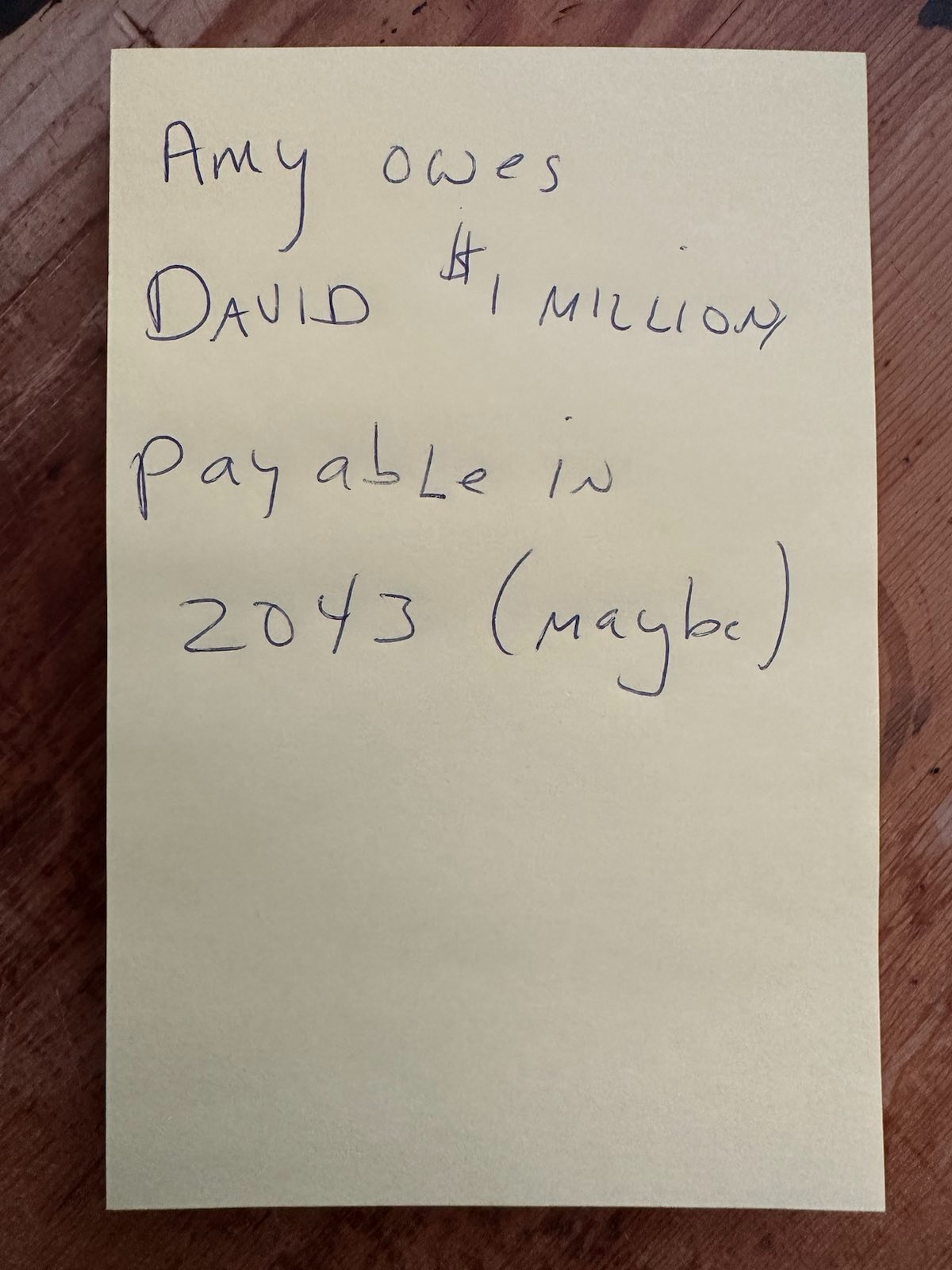

Voyager says it has $110 million of cash and “owned crypto assets” on hand, plus $1.3 billion in crypto assets on its platform. It owes nearly $1 million to Google and $75 million to Alameda Research — which recently threw Voyager a lifeline of $485 million. The rest of its large unsecured creditors are customers.

Alameda says it’s “happy to return the Voyager loan and get our collateral back whenever works for Voyage” — we’re not even sure what that means. [Tweet]

Voyager holds $350 million of customer money in an omnibus account at Metropolitan Commercial Bank — just an undifferentiated pile of cash, with only Voyager knowing which customers’ money it is. The judge says “That money belongs to those customers and will go to those customers” — but the company will have to sort through who owns what and conduct a “fraud prevention process” (KYC, we presume) first. [Bloomberg, archive]

Voyager sent its customers an email stressing that it’s not going out of business — it has a plan! [Reddit]

“Under this Plan, which is subject to change given ongoing discussions with other parties, and requires Court approval, customers with crypto in their account(s) will receive in exchange a combination of the crypto in their account(s), proceeds from the 3AC recovery, common shares in the newly reorganized Company, and Voyager tokens. The plan contemplates an opportunity for customers to elect the proportion of common equity and crypto they will receive, subject to certain maximum thresholds.”

Instead of getting your crypto back, you’ll get a corn beef hash of magic beans, and we’ll call that money, okay?

The only issues here are that future Voyager tokens, future proceeds from the 3AC recovery, and future equity in the reorganized company will all be close to worthless.

Putting this nonsense through the bankruptcy court will take months, and Voyager customers get to stand back and watch in horror as the value of their crypto plummets to nothing. Look what’s happened to Mt. Gox customers — they are still waiting.

Jim Chanos weighs in on Voyager’s apparently false claims that its money is FDIC insured: “Making false claims to attract depositors/investors is financial fraud, plain and simple. No regulatory jurisdiction tug-of-war need come into play here, if true.” [Twitter]

The FDIC is also looking into Voyager’s FDIC claims. [WSJ]

Patrick McKenzie writes one of his informative blog posts on money transfer systems, this time explaining what a deposit is — and what a deposit isn’t. Unsurprisingly, he rapidly gets to our friends at Voyager Not-A-Bank. [Kalzumeus]

Voyager is just trying to buy time. But given their apparently false claims of FDIC insurance, the odds they can get a judge to let them avoid liquidation this way are zero.

When the accountants get hold of the books and start going through everything, the real story will be shocking. We saw all this happen with QuadrigaCX.

Voyager stock trading was halted on the Toronto Stock Exchange, after the bankruptcy filing. [Newswire]

Cornell Law professor Dan Awry writes: “If you thought securities regulation was a jolt to the crypto community, just wait until they learn about bankruptcy law.” [Twitter]

Here’s a Voyager ad preying on artists. Why be a poor artist when you can get rich for free by handing them your crypto? [YouTube]

And here’s a Twitter thread detailing Voyager’s shenanigans in getting a public listing in the first place. They bought a shell company and did a reverse-merger — and then pumped the stock, only to dump it during crypto’s bull run. [Twitter thread]

It’s worth a closer look at just how much ickiness from Voyager the Metropolitan Commercial Bank risks getting on itself. Dig page 30 of this March 2022 investor presentation, talking up Metropolitan’s foray into crypto customers. The presentation mentions elsewhere how Metropolitan wants to get into crypto. [Investor presentation]

Celsius Network Ltd. has a new board of directors. They’re all bankruptcy attorneys. [Companies House]

But Celsius is not bankrupt yet! As such! In fact, Celsius is still paying debts! If selectively. Though paying down debts is likely a sign that Celsius is getting its books in order before filing for bankruptcy.

Celsius has repaid $150 million worth of DAI to MakerDAO. Celsius still owes MakerDAO about $82 million in DAI. [FXEmpire]

On July 4, Celsius took out 67,000 ETH ($72 million) from Aave (30,000 ETH) and Compound (37,000 ETH). [Etherscan; Peckshield; Tweet]

Celsius has laid off 150 employees. [Ctech]

Let’s keep in mind that Celsius isn’t just about crypto bros wrecking each other. Celsius investors were lied to and stolen from: “Celsius customers losing hope for locked up crypto.” [WSJ]

Celsius’ CEO has a book on Amazon — you know, in case anyone felt they needed the financial wisdom of Alex Mashinsky in their life. What editor at Wiley thought this was a good decision? “This book belongs on the bookshelf of anyone interested in financial independence, cryptocurrencies, bitcoin, blockchain, or the battle between decentralization and centralization.” Also, how to take everyone’s money and lose it playing the DeFi markets. [Amazon]

KeyFi sues Celsius: I’m shocked, shocked to find that Ponziing is going on in here!

0x_b1 was a crypto whale, active on Twitter, who traded vast sums of crypto in the DeFi markets. He was the third-largest DeFi user at one point, with only Alameda Research and Justin Sun doing larger volumes. 0x_b1 was highly respected, yet nobody knew who he was or where he got his wealth from — until now.

0x_b1 turns out to be Jason Stone, the CEO of trading firm KeyFi, a.k.a. Battlestar Capital, who says that KeyFi managed Celsius’ DeFi portfolio from 2020 to 2021. The cryptos that 0x_b1 traded were hundreds of millions of dollars (in crypto) of Celsius customer funds.

As Battlestar Capital, Stone first hooked up with Celsius in March 2019. Battlestar said that customers could earn an astonishing “up to 30 percent” annually from staking their cryptos. [CoinDesk, 2019]

Jason Stone and KeyFi are now suing Celsius, saying they never got paid. A case was filed 7 July by Stone’s attorney, Kyle Roche of Roche Freedman. The complaint is incendiary. [complaint, PDF]

Celsius saw DeFi take off in 2020. Celsius figured they could use customer funds to play the markets and make some yield, so they hired KeyFi to trade for them, with a handshake agreement to share the “hundreds of millions of dollars in profits” — rather than anything so trad-fi as, e.g., a written contract. (They did finally write up contracts after KeyFi had been working for Celsius for six months.)

Celsius invested cryptos, and its liabilities to customers were denominated in cryptos — but Celsius accounted for everything in US dollars. So if an asset appreciated, Celsius and KeyFi might show a dollar profit — but Celsius might not be able to repurchase the ETH or whatever, to return it to the customer who lent it to them, without losing money to do so.

KeyFi says it would have been trivial to hedge against such an event by purchasing call options at the spot price it originally paid. KeyFi says that Celsius didn’t do this — but told KeyFi it had. It’s not clear why KeyFi didn’t just do something similar themselves.

Celsius gave customers a higher yield for accepting payment in their own CEL tokens. The yield was calculated in dollars. Stone alleges that Celsius used customer bitcoins to pump the price of CEL through 2020, meaning they paid out less CEL for a given dollar yield.

Alex Mashinksy also sold $45 million of his personal CEL holding during this time.

“The Celsius Ponzi Scheme” starts on page 23 of the complaint. Celsius had liabilities to customers denominated in ETH — but bitcoin and ether prices started going up dizzyingly in January 2021:

“87. As customers sought to withdraw their ether deposits, Celsius was forced to buy ether in the open market at historically high prices, suffering heavy losses. Faced with a liquidity crisis, Celsius began to offer double-digit interest rates in order to lure new depositors, whose funds were used to repay earlier depositors and creditors. Thus, while Celsius continued to market itself as a transparent and well capitalized business, in reality, it had become a Ponzi scheme.”

Jason Stone and KeyFi quit in March 2021.

In September 2021, Roche wrote demanding a full accounting from Celsius, and all the money that Celsius hadn’t paid KeyFi. This was the start of the present action, and this is what KeyFi is suing over.

This suit is important because it sets out a clear claim that Celsius operated as a Ponzi scheme. If the courts find that Celsius was in fact a Ponzi, then any money or cryptos that Celsius paid out to customers or some creditors could be clawed back in bankruptcy.

Stone is seeking damages for an amount “to be determined at trial.”

It’s not clear that Stone was as great a trader as he paints himself. A report from Arkham details how Stone racked up $350 million in losses. [Arkham, PDF]

CoinFLEX

We’ve been watching online interviews with Mark Lamb of CoinFLEX, which stopped withdrawals after $47 million of bitcoin cash (BCH) went missing.

Lamb, who appears alone in the interviews, keeps saying “we” and referring to his “team.” His wife is the chief marketing officer of CoinFLEX and Sudhu Arumugam is listed as a cofounder, but where’s the rest of the team?

How Lamb’s business really works: [Twitter]

- Create fictitious dollars (FlexUSD).

- Lock them up in a lending scheme.

- Offer unsustainably high yields to attract retail deposits.

CoinFLEX had a special deal with CoinFLEX investor Roger Ver, where it would not liquidate Ver’s account in the event of a margin call — a highly risky proposition for Coinflex.

Ver had taken a large long position in BCH, which was losing value. [Twitter] Lamb claims Ver needed to deposit $47 million to meet a margin call.

But it looks like Lamb liquidated Ver’s BCH anyway by selling it on Binance, even though he’s claimed to know nothing of this. CoinFLEX claims that Ver owes them $47 million, while Ver considers that Lamb broke their agreement.

Lamb lent one-third of all CoinFLEX’s customer money to one guy. Now, with the “significant loss in liquidating his significant FLEX coin positions,” the deficit for Ver’s account is $84 million. CoinFLEX says that they’ve brought an arbitration against Ver in Hong Kong. It will take 12 months to get a judgment. [blog post]

Meanwhile, CoinFLEX are … issuing a new coin (rvUSD), out of thin air, to pay back their existing customers.

Lamb explained his incredible plan to rescue CoinFLEX in an interview with Ash Bennington on Real Vision. Lamb refused to reveal how big the hole in his books actually is. “I can’t comment on those specific figures at this time.” [Twitter]

But creditors will be made whole and transparency will come — in the fabulous future, along with an audit!

Lamb’s plan includes issuing rvUSD, a debt token. You get 20% returns — also to be paid in rvUSD. Lamb says the returns will be funded by Ver paying the money, which Ver still maintains he doesn’t owe.

Lamb has clearly thought all of this through carefully with his “team.” Their hard work is apparent — the rvUSD whitepaper is three pages long. [Whitepaper, PDF]

Who would want to buy rvUSD? Lamb told Bennington he has lots of “big” investors lined up. CoinFLEX says it will resume 10% of withdrawals in a week and everyone will get their money as soon as these big investors come through.

There are 197 million FlexUSD tokens in the wild, according to Coingecko. Even if Ver owes $47 million, there should still be a difference of $150 million in collateral there — if FlexUSD is indeed fully backed by USDC, as Lamb claims it is. Additionally, CoinFLEX still has $10 million of BCH held for its bridge to its SmartBCH chain. And there are user deposits on the exchange.

So what percentage of assets does CoinFLEX still have? Why won’t they release assets and liabilities?

Other legitimate trading firms that are definitely stable going concerns

BlockFi: BlockFi and FTX reached a deal on 1 July, where FTX will buy BlockFi for a “variable price of up to $240 million based on performance triggers” that will provide Blockfi with a $400 million credit facility. [BlockFi; Twitter thread]

Babel: Orthogonal Trading issued a default to defunct DeFi lender Babel regarding a $10 million loan. [Twitter]

Genesis: Genesis is one of the largest cryptocurrency brokerages for institutional investors. The company confirmed speculation that it had exposure to 3AC. Genesis is part of Digital Currency Group, who put in some cash to prop them up. [Bloomberg; Twitter]

Blockchain.com: another crypto exchange that thought playing the DeFi markets with customer funds was a good and cool idea. They lost $270 million in loans to 3AC. They told shareholders: “Three Arrows is rapidly becoming insolvent and the default impact is approximately $270 million worth of cryptocurrency and U.S. dollar loans from Blockchain.com.” [CoinDesk]

Uprise: Korean crypto startup Uprise lost $20 million shorting luna in May. They were right about luna — but their short was wiped out anyway, by a sudden spike in the price. [The Block]

CoinLoan: Crypto lender CoinLoan restricted withdrawal limits on 4 July — from $500,000 per day down to only $5,000 per day. They are calling this a “temporary change” to withdrawal limits. Presumably, it’s “temporary” because it will soon be $0. [Tweet; Bitfinex Tweet]

They directly say this is because of “a spike in withdrawals of assets from CoinLoan.” How dare you try to get your funds out! [blog, archive]

Nexo: has signed a term sheet to acquire 100% of defunct Indian crypto exchange Vauld. It’s not clear what’s left in Vauld, or if Nexo thinks they can pillage the corpse but pretend Vauld’s considerable liabilities to customers don’t exist. [Coindesk]

Our friend Michel does the numbers. He estimates $300 million was lost by Vauld in the UST/luna collapse. [Twitter]

Bitcoin Core ETP: this is an exchange-traded product, a bit like a bitcoin ETF, but based in Switzerland. How does the ETP plan to make money? By lending out the bitcoins on the DeFi markets! That will definitely work out fine, probably. [FT, paywalled]

{kind=link}