Bitcoin has set yet another new all-time high — $73,835 on Coinbase BTC-USD on March 14. This means bitcoin is good now! All our past objections are resolved. Going forward, we only deal in Finances U Desire.

Sound and fury, signifying nothing

What’s interesting is that while the price is back up, the bitcoin trading market has not recovered. If anyone says “the market is back!” that’s an incorrect claim.

Market volume is one-eighth of what it was in November 2021, the last time the price was this high.

We get that number from Coinbase retail trading fee income, which is 2% of the volume. Coinbase is the largest actual-dollar exchange and it’s not allowed to lie in SEC filings — so for once in crypto, we have numbers we can trust a bit.

The retail trade volume against actual dollars on Coinbase went down in seven of the past eight quarters. Here’s a table from Q4 2021 to Q3 2023. Q4 2023 didn’t show any improvement.

Even as the price went up through 2023, every day people wanted bitcoins less and less. Coinbase gives us the numbers showing this.

(This is why we prefer to just quote the Coinbase price — the skew between exchanges can be hundreds of dollars when anything interesting is happening.)

BTC-USDT on BitMEX flash-crashed from $66,000 to just $8,900 on Monday, March 18. Starting at around 22:40 UTC, someone dumped 1,000 BTC as fast as possible at whatever the market would pay for it. [CoinDesk; Twitter, archive]

By the time the flash crash flowed through to Coinbase, it was a mere $2,000 drop.

BitMEX has much less bitcoin liquidity than Coinbase BTC-USD or Binance BTC-USDT — so we suspect this was a very urgent seller who felt that FinCEN didn’t need his details.

We’re not sure why our trader didn’t use OKX, HTX (formerly Huobi), or Bitfinex, which would have had more liquidity and thus less price slippage — hence our impression that they were really in a hurry. And now they have to put all that USDT somewhere.

ETFs will save bitcoin!

BlackRock says its spot bitcoin ETF has reached $10 billion in assets. But Grayscale’s GBTC has seen over $11 billion in outflows because nobody wants to pay their 1.5% fee. (Everyone else is around 0.3%.)

Bitcoin ETFs aren’t hitting the institutions they were hoping for — pension funds and so on. (Thankfully.) For all of BlackRock’s helpful ETF marketing advice, financial advisors are being very careful about recommending these things. [WSJ, archive]

The money flowing into the ETFs seems to be from individual investors. It’s not clear whether these are new investors or just existing holders dumping their bitcoin for ETFs because they’re tired of being their own bank.

This Financial Times article starts with BlackRock talking up its bitcoin ETF and the fabulous future of the blockchain … then details every way in which crypto is utterly incompatible with sane finance and doesn’t work. [FT, archive]

The hot air crypto bubble

Meanwhile, Tether has printed 11 billion tethers just since the start of 2024. It’s at 103 billion tethers and counting.

We very much doubt that most of these billions of tethers are being bought with real US dollars. Why would you send real dollars to an unregulated offshore wildcat bank to buy bitcoins when you could just put them into a US-regulated bitcoin ETF?

We suspect the tethers are being printed out of thin air and accounted as loans — the fresh USDT is “backed” by the loan itself.

This supports our theory that the present pump is not real money flooding into bitcoin. It’s stablecoins on Binance — tethers and FDUSD. The volume on Binance completely swamps the volumes on Coinbase or ETF trading.

The bitcoin price chart looks very like someone’s trying to pump the price. You’ll see the price slowly getting walked up, as if someone’s wash-trading it up … then it hits a round number of dollars, someone tries to cash out, and the price drops several thousand.

Fake dollars going up, real dollars going down.

So we’re not in a bubble. We’re in a balloon, one being pumped full of hot air. It’s fun going up — but the trip down can be very quick.

What do I do with my holdings?

Back in November 2022, when exchanges were suffering urgent unplanned maintenance left, right, and center, we went so far as to say that if you insisted on investing in bitcoins, you should not risk storing your coins on an exchange. Holding private keys is ridiculously fraught and the tech is still unusable trash — but it’s still not as bad as trusting bitcoin exchanges.

If you must hold bitcoins in the hope of getting dollars for them one day, the least-worst option is to buy into an ETF. That way you’re in a regulated market and your only risk is Coinbase Custody getting hacked.

If you’ve bought into crypto, please at least cash out your principal — the cash basis that you paid to buy in. Then everything you make from then on is pure profit. When the price crashes, you won’t have lost anything.

Our real recommendation, of course, is not to touch this garbage.

Back in the snake pit

Bitcoin suffered a year of its media coverage being “Sam Bankman-Fried is a crook.” Crypto pumpers tried to make out that FTX, the second-largest exchange, being a massive fraud was a mere aberration on the part of Bankman-Fried, and everyone else in crypto was a good guy.

Then the first-largest exchange, Binance, got busted too. So price discovery for bitcoin — what determines where the number goes — happens on an exchange that literally admitted a few months ago to being a criminal conspiracy. Binance’s founder and former CEO, Changpeng “CZ” Zhao, is in the US awaiting sentencing.

We find, over and over, that normal people keep assuming that crypto isn’t just a completely criminal snake pit. Because US dollars are able to touch it in any way, so surely it’s regulated. Right?

Finance and finance journalism seem to have collectively forgotten what a hellhole unregulated markets always were.

The way crypto works is:

Actual dollars flow from retail suckers to a few rich guys;

There’s lots of fancy bafflegab to obscure the very simple flow of actual dollars.

Crypto is an unregulated mob casino and the regulated exchanges are just the cashier’s desk.

You can absolutely make money in crypto — we would never say that you can’t. But you have to be a better shark than all the other sharks who built the shark pool.

Trade carefully.

Media stardom

Billy Bambrough wrote about the bitcoin price for the Sunday Times and spoke to David. In a rare moment for journalistic coverage of the number, Tether was mentioned! [Sunday Times, archive]

____________________________________________

A word from our sponsors

Spread the good word — if you liked this post, tell just one other person. It really helps!

We write this newsletter for money. Please send us some! Here’s Amy’s Patreon and here’s David’s. For casual tips, here’s Amy’s Ko-Fi and here’s David’s.

Help our work: if you liked this post, please tell just one other person. It really helps!

You can also send money to our one-way ETFs! Here’s Amy’s Patreon and here’s David’s. For casual tips, here’s Amy’s Ko-Fi and here’s David’s.

Boy, those ETFs were the juice bitcoin really needed, eh?

The SEC approved 11 bitcoin spot ETFs on Wednesday, January 10, with media widely reporting what a boon this would be for the coiners. Surely this would lure piles of fresh dollars into bitcoin!

Not quite. The bitcoin price held around $46,000 — but just for long enough for the whales to start cashing out.

What the crypto world needs to understand is that bitcoin ETFs are not bitcoins. They’re a traditional finance product with bitcoin flavoring.

Except for the risk — that bit is completely bitcoin.

Number go down

The first big post-ETF price drop came on Friday, January 12. Bitcoin slipped from $46,000 to $43,500 in two hours — only one hour after the day’s printing of a billion tethers was released. A few hours after that, another dump took the price from $43,500 to $41,000.

The bitcoin market is fake and in tethers. The retail securities market is real and in actual dollars. You can’t pump bitcoin ETFs with tethers.

After years of being severely discounted from the price of the bitcoins in the fund, Grayscale GBTC finally reached net asset value. This turned out to be not so great — it looks like long-frustrated GBTC holders are finally dumping now that they can. [CoinDesk; Bloomberg, archive]

Coinbase (Nasdaq: COIN) stock went down as well. It was up as high as $186 at the end of December. It dropped to $130.78 on January 12.

ETFs have put bitcoin on steroids! Asthmatic and with shrunken balls.

Bitcoins: not so great

Bitcoins are still an awful investment for ordinary people who aren’t true believers in Satoshi and just want to grow their dollars.

The ETF S-1 filings go into considerable detail on the risks — none of which should be news to anyone here.

The main risk the ETF trusts see is that the base asset is still a completely terrible investment. Crypto is insanely volatile. A pile of crypto companies went broke from being run by crooks — the filings go into some detail on this. Everyone hates bitcoin miners. The regulators, from the White House down, increasingly just despise everything about crypto. And very few people like bitcoin anyway.

Securities broker Vanguard thinks the bitcoin ETFs are such trash that they’re not only not offering these spot bitcoin ETFs — they’re withdrawing the crypto futures ETFs they presently offer. [Axios]

What happens if the ETF bitcoins are stolen?

Unlike a bitcoin futures ETF, a spot ETF is based on actual bitcoins — and these have to be stored somewhere.

Most of it, including $29 billion face value of GBTC bitcoin, is stored by Coinbase Custody. VanEck is storing their ETF coins at Gemini. Fidelity is storing their ETF coins at their own custody subsidiary.

So what happens if a hacker gets into the digital fortress and takes all the bitcoins?

In short: too bad. Sorry, your money is gone!

Coinbase Custody advised BlackRock that it has insurance covering up to $320 million losses of custodied crypto — but that’s for all its customers’ $144 billion (face value) of cryptos in custody. That’s a whole 0.2% coverage. [SEC]

The ETF trusts themselves do not have FDIC or Securities Investor Protection Corporation (SIPC) insurance.

The ETF trusts specifically disclaim liability for lost backing assets. Valkyrie, for example, says: “Shareholders’ recourse against the Trust, Trustee, Custodian and Sponsor under New York law governing their custody operations is limited.” [SEC]

Investors would likely sue anyway. BlackRock and Fidelity could cover such a loss, though it would sting. Grayscale would be utterly unable to cover it.

If Coinbase were to go bankrupt, it’s not clear legally if crypto stored in Coinbase Custody would belong to the individual customers or would be thrown into the bankruptcy estate!

The custodian just losing all the bitcoins is not a trivial risk — two crypto custodians, Prime Trust and Fortress, went bankrupt in 2023 just from losing customer coins.

We spoke to Frank Paiano, who teaches finance and investing at Southwestern Community College, about what would happen if a bitcoin ETF’s backing assets vanished. [Frank Paiano]

He thinks that customers “will be fooled into thinking” that the ETF assets are protected, even though they absolutely are not. “That is mostly why Fidelity has set up their own trustee. I would guess that companies such as BlackRock would do the same.” (BlackRock is so far just using Coinbase.)

Loss of ETF-backing assets happens quite a lot, said Paiano. “A simple Internet search for ‘gold investments stolen’ yields several examples. Then there are the age-old anecdotes of people being duped into buying lead painted or plated with gold.”

Paiano thinks bitcoin ETFs are profoundly unwise investments: “prudent, long-term oriented investors should stay far away from these abominations”— but they’ll find customers.

“If there are foolish, greedy individuals willing to part with their hard-earned money, there will be scoundrels happy to oblige them.”

Other bitcoin ETF fallout

The day before the SEC announced its approval of 11 spot bitcoin ETFs, the official @SECGov Twitter posted a fake notice saying a bitcoin ETF was approved. SEC Chair Gary Gensler issued a statement on the fake tweet, saying that an unauthorized party got hold of the phone number connected to the account but didn’t get access to any SEC internal systems. [SEC]

What happens next?

The new narrative we’ve seen is that the real bitcoin pump is in 90 days when financial advisors are finally ready to push bitcoin ETFs on their customers, for some reason. Probably the halvening, or sunspots maybe.

We don’t expect the number to go up just from bitcoin ETFs existing — anyone who wanted bitcoins could already buy them, and “anyone” numbers one-eighth of what it did in the recent bubble.

We do expect downward pressure on the bitcoin price to continue from the GBTC holders who can finally cash out near par.

Tether pumps only work if nobody tries to cash out into the pumped-up price. Unfortunately, that only works as long as nobody wants real dollars. It turns out they do.

With these ETFs, bitcoin is the dog that caught the parked car.

Media stardom

David was quoted by Cointelegraph on bitcoin ETFs. A bitcoin ETF is a terrible idea, but we don’t think the threat model includes the issuers stealing the bitcoins. [Cointelegraph; Cointelegraph; Cointelegraph]

David spoke to Davar about bitcoin ETFs and our friends at Tether. (“Basket fund” is the local term for “ETF.”) [Davar, in Hebrew, Google translate]

David went on Logan Moody’s podcast The Contrarian just before the ETFs were approved to talk about the state of crypto as of early 2024. [YouTube]

As predicted, the SEC today approved several spot bitcoin ETFs — Grayscale GBTC, Bitwise, Hashdex, BlackRock iShares, Valkyrie, ARK 21Shares, Invesco Galaxy, VanEck, WisdomTree, Fidelity Wise Origin, and Franklin.

Fees are cut throat, some less than a quarter of a percent. These companies can run the ETFs as loss leaders for a while, but eventually they’ll have to raise the fees or quit.

Today’s post is over on David’s blog. [DavidGerard]

Q: I keep wondering what’s keeping the circus alive, given that the retail dollars are practically gone, and the last remaining on/off-ramps are all but down the drain. [Tomalak on Bluesky]

The circus is fed by dollars — real and fake — and its product is hopium, the unfaltering belief that number will always go up. The hopium runs on narratives, such as the current story that a bitcoin ETF will result in a magical influx of fresh dollars.

In crypto, the retail dollars have largely gone home — but too many people have large piles of crypto accounted as dollars to let the number go down. So they deploy fake dollars to keep the crypto flowing.

There are currently 93 billion dubiously-backed tethers sloshing around the crypto markets. We expect that to go over 100 billion as we get closer to the bitcoin mining reward halving in April.

The circus is advertised by the crypto media, which functions as PR outlets for the space. The CoinDesk live-wire feed on any given day is about half hopium, for instance. There are no respectable media outlets in a crypto winter.

Q: Why can’t or wouldn’t the average investor make money in crypto? We criticize it, and rightfully so, but why should the person looking to make a profit care? [King Schultz on Twitter]

There is no source of dollars other than fresh retail investors. Old investors can only be paid out with money from new investors.

Crypto isn’t technically a Ponzi scheme — it just works like one. So investing in crypto will always be a slightly negative-sum game.

Functionally, crypto is a single unified casino, run by a very small number of people, with no regulation. Binance is the tables, Coinbase is the cashier window. The flow of cash is from retail suckers to very few rich guys at the top.

There are many, many complicated mechanisms in the middle, and they’re fascinating to look at and describe and watch in action. But the complex mechanisms don’t change what’s happening here — money flows from lots of suckers to a few scammers.

Some people make money in crypto, just like some people make money in Las Vegas — but gambling in Vegas isn’t an investment scheme either. And the house always wins.

You can make money in crypto if you’re a better shark than all the other sharks in the shark pool, who built the pool. It can be done! Good luck!

Q: be interested in reading about money laundering [Broseph on Bluesky]

Money laundering is when you try to turn the proceeds of crime into money that doesn’t appear to be the proceeds of crime. Laundering money is also a specific crime in itself.

With money going electronic, it’s harder to obscure the origins of ill-gotten gains and avoid unwanted attention from banks and the authorities. Many crooks have attempted to launder money by using crypto as the obfuscatory step.

Heather “Razzlekhan” Morgan and Ilya Lichtenstein tried laundering the bitcoins from the Bitfinex hack through the Alphabay darknet market. This would have completely covered their trail! Except that the police had pwned Alphabay by then, and Lichtenstein’s transactions were all right there for the cops to track him. Whoops.

We also highly recommend Dan Davies’s fabulous book on fraud, Lying for Money.

Q: Not so much baffled but curious as to how law enforcement can and does identify people using blockchain. Also, do some coins not have a public blockchain? [Bob Morris on Twitter]

Cryptocurrencies run on publicly available blockchains. In theory, you can trace the history of every transaction on a blockchain right back to when it started.

The hard part for authorities is linking someone’s real-world identity to a specific blockchain address. Achieving this was the key to busting Heather Morgan and Ilya Lichtenstein, for instance. The hardest part for crooks is cashing out successfully without being busted.

The trail can be difficult to trace, especially if the crook has put effort into obfuscation — e.g., running transactions through a mixer such as Tornado Cash. But specialists can get good at tracing blockchain transactions and several companies sell this as a service.

Privacy coins like Monero and ZCash try to obfuscate the traceability of transactions on the blockchain itself. But users often give themselves away by other channels — e.g., transaction volumes elsewhere that coincidentally correspond to amounts of Monero sent to a darknet market.

Even if you can protect yourself cryptographically, one error can leave your backside hanging out — and crypto users are really bad at operational security.

Q: nfts aren’t really relevant these days but I’ve never been clear on what ‘mint events’ are and how they relate to the icos. Are users generating new nfts paid for by using the coins they previously bought? [Robert Kambic on Bluesky]

Initial coin offerings (ICOs) were huge in 2017 and 2018 — but the SEC came down hard on them because they were pretty much all unregistered offerings of penny stocks.

Since that time, crypto has tried to come up with other ideas for doing unregistered offerings while making them look at least a little less illegal. There were SAFTs, airdrops, and now NFT mint events. These are all about creating fresh tokens out of thin air and promoting them as an investment in a common enterprise that will make a profit from the efforts of others.

A “mint event” is when you buy into an NFT collection early — when it first mints — hoping the value will increase astronomically over time.

But these are not securities, no, no, no. Yuga Labs wasn’t selling you shares in a company — they were selling you ape cartoons! You weren’t getting dividends, you were getting Mutant Apes, dog NFTs, and ApeCoins! You’re not investing in a speculative startup, you’re buying art!

The SEC has so far sued one NFT company, Impact Theory, after it raised $30 million through NFT sales. The SEC said the NFTs were promoted as investment contracts and not registered. [Complaint, PDF]

We didn’t say too much about NFTs in our 2024 predictions, but we expect that the SEC will go after more NFT projects this year, as they clear their backlog of violators.

Q. I’d like a definitive explanation on the amount of apes you can feed with a single slurp juice. [Etienne Beureux on Twitter]

Slurp juices were popularized in a tweet about Astro Apes, a Bored Apes knockoff, which also featured tokens called “slurp juices” that you could apply to your Astro Ape tokens to generate more Astro Ape tokens and get rich for free.

The tweet was posted on May 4, 2022 — just a few days before Terra-Luna exploded and popped the 2021-2022 crypto bubble.

Also, the guy who tweeted about slurp juices is a neo-Nazi. Welcome to crypto. [BuzzFeed News]

Q: I’ve often wondered why new languages like Solidity were necessary for smart contracts. [David John Smailes on Twitter]

The Ethereum team originally just wanted to use JavaScript, but it didn’t quite do what they needed in terms of functionality and data types — so they created Solidity, a new language based on JavaScript.

A blockchain is an extremely harsh programming environment. It’s hard or impossible to modify your code once deployed — you must get it right the first time. It’s about money, so every attacker will be going after your code.

In situations where programming errors have drastic consequences, you usually try to make it harder to shoot yourself in the foot — functional programming languages, formal methods, mathematical verification of the code, not using a full computer language (avoid Turing completeness), and so on.

Solidity ignores all of that — and the world’s most mediocre JavaScript programmers moved sideways to write the world’s most mediocre smart contracts and cause everyone to lose all their money, repeatedly. Smart contracts are best modeled as a piñata, where you whack it in the right spot and a pile of crypto falls out.

Other blockchains saw Ethereum-based projects making a ton of money (or crypto) and wanted that for themselves — so they tend to just use the Ethereum Virtual Machine so they can run buggy Solidity code too.

There are other, somewhat better, smart contract languages — but Solidity is overwhelmingly the language of choice, which keeps the comedy gold flowing nicely.

Q. Miner extracted value? [Cathal Mooney on Twitter]

Miners — or now validators — supposedly make money from block rewards and transaction fees.

There is a third way for validators to make money. Smart contract execution depends on the order of transactions within a block. Since the validator controls what transactions they can put in a block and how they order those transactions, they can front run the traders — the validator sees an unprocessed transaction, creates their own transaction ahead of that one and takes some or all of the advantage that the trader saw.

The term “Miner Extractable Value” was coined in the paper “Flash Boys 2.0: Frontrunning in Decentralized Exchanges, Miner Extractable Value, and Consensus Instability” in 2020. [IEEE Xplore]

Front-running is largely illegal in real finance. But since the Ethereum Foundation couldn’t stop their validators from front-running their users, they decided to claim it was a feature, which they have renamed “maximal extractable value.” [Ethereum Foundation]

Q: What do you think will eventually happen to all the Satoshi Nakamoto Bitcoin wallets? [Steve Alarm on Twitter]

Quite likely nothing. We suspect the keys, and thus the million bitcoins, are simply lost. Nobody has heard anything verifiably from Satoshi since April 13, 2011, when he sent a final email to bitcoin developer Mike Hearn. [Plan99]

If the Satoshi coins ever did move, there would be a lot of headlines. But we don’t think the crypto trading market would be affected much — the market is so thin, there are multiple large holders who could crash the market any time they felt like it, and the market is already largely fake. We think everyone will just pretend nothing happened and everything is fine.

Q. Did Do Kwon actually sell all his BTC to prop up Luna? [Saku Kamiyūbetsu on Twitter]

Terra (UST) was an algorithmic dollar stablecoin and luna was its free-floating twin. Terraform Labs ran the Anchor Protocol, which promised 20% interest on staked UST. At peak, there were 18 billion UST in circulation.

It turned out there was money to be made in crashing UST — so in May 2022, someone did. There is a strong rumor (and DOJ investigations) that it was Alameda. Other parties who collapsed because of Terra-Luna left the gaping hole in Alameda that eventually killed FTX. If Alameda fired the first shot directly into their own leg, that would be extremely crypto, as well as extremely funny.

UST was crashing, so Terraform Labs tried to prop up Terra-Luna. The bitcoins came from the Luna Foundation Guard, which promised to deploy $1.5 billion worth of bitcoin to defend UST. This didn’t work. [Twitter, archive]

We haven’t found a smoking gun that Luna actually spent the bitcoins on buying up UST or luna. In 2023, the SEC charged Terraform Labs and Do Kwon and said that Kwon and Terraform took over 10,000 BTC out of Luna Foundation Guard in May 2022 and converted at least $100 million into cash.

Q: I’m baffled at the lack of interest from crypto critics that the DoJ will not be pursuing additional charges against SBF. Specifically, the charges that could make some politicians very uncomfortable. [Amer Icon on Twitter]

The issue was specifically whether to further prosecute Sam Bankman-Fried. The prosecution letter to the judge quite clearly explains their reasons why a second case wouldn’t do anything useful in this regard. [Letter, PDF]

The evidence that Sam was the guy who made these bribes was presented in the case that just concluded and will be considered when he’s sentenced in March — they don’t need a second trial to nail those facts down.

Hypothetical other evidence that might have come to light about other parties wasn’t a factor in considering what to do about Sam Bankman-Fried. It’s quite reasonable to want to get those guys, but you will probably need a more direct method than a side factor in an additional case against a guy who is already likely going to jail forever.

Q. snarkier memes would be worthy [Chris Doerfler on Twitter]

“Esto no puede ser tan estúpido, debes estar explicándolo mal.”

We did a follow-up on this story. Part 2, though not labeled as such, is here!

Image: Amy Landers and Dear David reading today’s Web 3 Is Going Just Great

The SEC really doesn’t want to approve a bitcoin ETF — but we think it may be forced to. So it’s gonna make them compliant, which means they’ll suck a lot more for crypto’s purposes.

Image: Gary Gensler with Zeke Faux’s Number Go Up.

Bitcoin is over $44,000! By complete coincidence, Tether has printed five billion USDT in the past month out of thin air as “loans.”

In its attempts to explain number go up, the mainstream press keeps repeating crypto talking points — a bitcoin ETF is coming soon, and all the crime is behind us now — without mentioning Tether! David and I break down what’s behind the current pump — and why the crypto talking points are absolute rubbish.

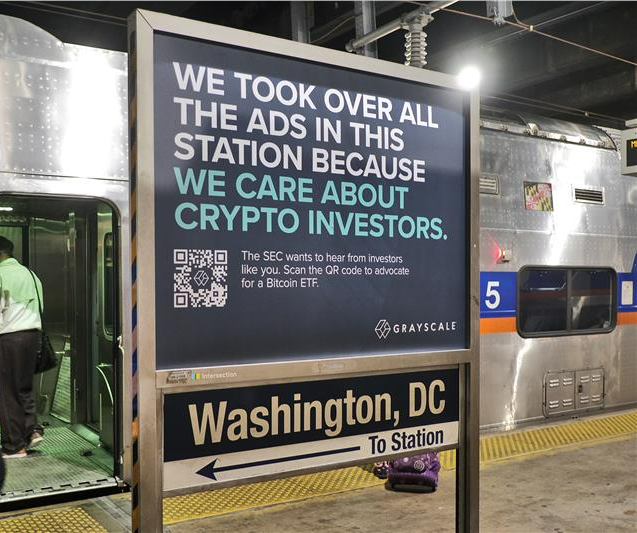

If you happen to be taking Amtrak and pass through Penn Station or Union Station, you will notice something unusual: every available ad space has been taken up by Grayscale.

“We care about crypto investors,” the crypto asset manager says in its ads. Grayscale is urging the public to write to the Securities and Exchange Commission and convince them to approve the first spot bitcoin ETF in the U.S.

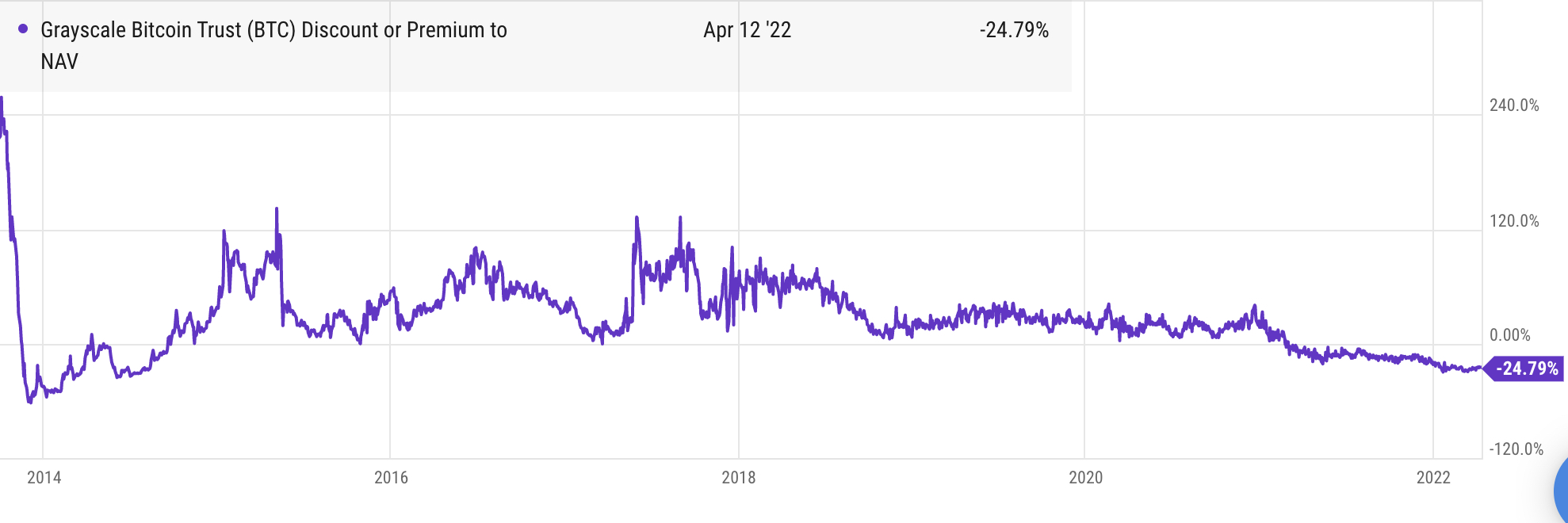

Grayscale wants to convert its Grayscale Bitcoin Trust (GBTC) into a bitcoin ETF after flooding the market with shares. GBTC is trading 25% below its net asset value, and investors are rightfully pissed off. Grayscale wants them to be upset with the SEC, but the regulator isn’t really to blame. If anything, the SEC should have warned the public about GBTC years ago.

Over the last eight years, Grayscale has been telling investors to buy shares of GBTC, advertising the fund as a way to get exposure to bitcoin without having to buy bitcoin.

Accredited investors plowed dollars (or maybe bitcoins) into the fund all through 2020, looking to take advantage of an arbitrage opportunity. They could buy in at NAV, and after a 6 to 12-month lockup, sell on the open market for a premium. All through 2020, that premium was around 18%, on average.

Everybody was happy until February 2021, when the Purpose bitcoin ETF launched in Canada. Unlike GBTC, which trades over-the-counter, Purpose trades on the Toronto Stock Exchange, close to NAV. At 1%, its management fees are half that of GBTC. Within a month of trading, Purpose quickly absorbed more than $1 billion worth of assets.

Demand for GBTC dropped off and its premium evaporated. Currently, 653,919 bitcoins (worth a face value of $26 billion) are stuck in an illiquid vehicle. Welcome to Grayscale’s Hotel California.

The plan all along, Grayscale claims, has been to convert GBTC into a bitcoin ETF. On October 19, 2021, NYSE Arca filed Form 19b-4 with the SEC. The regulator has until early July to respond.

In all probability, the SEC will reject the application, just as it has every single spot bitcoin ETF application put before it to date.

Bitcoin’s price is largely determined by wash-trades, whales controlling the market, and manipulation with tethers. SEC Chair Gary Gensler knows this. He taught a course in blockchain and money at MIT Sloan before his appointment by the Biden administration.

This is Grayscale’s second time around. It applied for a bitcoin ETF in 2016, but withdrew the application during the 2017 bitcoin bubble because “the regulatory environment for digital assets had not advanced to the point where such a product could successfully be brought to market.” Meanwhile, the trust’s assets under management grew as did Grayscale’s profits.

Closed-end fund

“Inflation is rising, we need to diversify!” a panicked woman tells her son over the phone in the middle of the night. “I’m buying crypto!” She hangs up. Her son rolls over in bed. The scene is from a series of TV commercials Grayscale ran in 2020 to convince the public that GBTC was a sound investment.

Digital Currency Group is the parent company of Grayscale. Both firms were founded by Barry Silbert. DCG is invested in hundreds of crypto firms. It owns crypto outlet CoinDesk, which essentially functions as a PR machine for the entire crypto industry.

Initially called the “Bitcoin Investment Trust,” GBTC launched in September 2013. It was promoted as an investment vehicle that would allow hedge funds and institutional investors to gain exposure to bitcoin, without having to deal with custody. Coinbase has been the custodian of the fund since 2019 when it bought Xapo, the previous custodian.

Legally, GBTC is a grantor trust, meaning it functions like a closed-end fund. Unlike a typical ETF, there is no mechanism to redeem the underlying asset. The SEC specifically stopped Grayscale from doing this in 2016. Grayscale can create new shares, but it can’t destroy shares to adjust for demand. Grayscale only takes bitcoin out to pay its whopping 2% annual fees, which currently amount to $200 million per year.

In contrast, an ETF trades like a stock on a national securities exchange, like NYSE Arca or Nasdaq. An ETF has a built-in creation and redemption mechanism that allows the shares to trade at NAV via arbitrage. Authorized participants (essentially, broker-dealers, like banks and trading firms) issue new shares when the ETF trades at a premium and redeem shares when they trade at a discount, making a profit on the spread.

How it all works

Grayscale periodically invites rich investors to pledge money into the fund in private placements at its discretion. The minimum investment is $50,000. Grayscale uses the cash to buy bitcoin and issues shares of GBTC in kind.

Investors can also pledge bitcoin directly — a great advantage if you happen to be a large holder who wants to unload your BTC without crashing the market. (More on this later.)

After a lockup period, investors can sell their GBTC on the open markets. Anyone can buy and sell GBTC on OTC Markets Group, the main over-the-counter marketplace, or via a brokerage account, like Schwab or Fidelity.

Up until early last year, GBTC has typically always traded at a premium on the open market. That premium occasionally soared to over 100%. During the 2017 bitcoin bubble, GBTC traded as high as 130% above NAV.

Why would anyone pay the premium? Many institutional investors can’t buy bitcoin directly for compliance reasons. And there are a lot of individuals who don’t want the headache of figuring out how to set up a bitcoin wallet. GBTC was initially the only option for getting exposure to BTC, without having to buy BTC, at least until bitcoin futures came along. However, bitcoin futures contracts came with their own risks, costs, and headaches. GBTC was easier.

In early 2020, GBTC became an SEC reporting company. This allowed investors who purchased shares in the trust’s private placement to sell their shares in 6 months instead of the previous 12 months. You could now make more money faster!

Unsurprisingly, the trust went into overdrive in 2020. Starting in January 2020 up to Feb. 23, 2021, Grayscale filed 35 reports with the SEC indicating that it sold additional shares to accredited investors, according to Morning Star’s Bobby Blue.

The trust’s holdings doubled from roughly 261,000 BTC in January 2020 to 544,000 BTC by mid-December 2020, per Arcane Research.

The @Grayscale Bitcoin Trust has attracted new investors throughout the year, leading to a doubling of Grayscale's BTC holdings from approx. 261k BTC in January to 544k BTC by Dec 12th.

Harris Kupperman, who operates a hedge fund, explained in a November 2020 blog post how GBTC’s arbitrage opportunity created a “reflexive Ponzi,” responsible for sending the price of bitcoin hyperbolic.

There were several versions of the arb. You could borrow money through a prime broker. You could use futures to hedge your bet. You could recycle your capital twice a year.

Every version involved Grayscale purchasing more bitcoin, thus increasing demand, widening the spread in the premium, and pushing the price of bitcoin ever higher. Between January 2020 and February 19, 2021, the price of BTC climbed from $7,000 to $56,000.

“When the spread is 26% wide and liquid to the tune of hundreds of millions per week, you can bet the biggest guys in finance are all over it,” Kupperman said. “As you can imagine, everyone big is putting on some version of this trade.”

Kupperman wasn’t the only person to raise alerts about the fund, which mainly benefited wealthy investors. As soon as GBTC launched, skeptics voiced their concerns.

“You can put a nice wrapper around a turd, and present it in a very well-manicured product to investors that you say is safe,” Barry Ritholtz, a wealth manager and founder of The Big Picture blog, told Verge. “But at the end of the day, it’s still crap.”

In September 2017, Citron Research called GBTC “the widow maker” and “the most dangerous way to own bitcoin.” Citron’s Andrew Left accurately predicted GBTC’s collapse:

“Citron believes that as new methods become available for investors to gain exposure to bitcoin — including traditional ETFs — that money will move to these regulated instruments and out of the uncertain waters of GBTC, which we believe can fall by 50% easily.”

Who holds GBTC?

The press has repeatedly credited Grayscale as a massive buyer of bitcoins, and evidence of institutional money entering the cryptoverse. This may not be the case.

Even though Grayscale states its holdings in dollars, it accepts deposits of bitcoins. A whale, or a good friend of Grayscale, can trade in their BTC for shares of GBTC, which they can flip six months later at well above the actual price of bitcoin.

The last time Grayscale broke out the numbers in Q3 2019, they said that the majority of deposited value into their family of trusts was in crypto, not dollars:

“Nearly 80% of inflows in 3Q19 were associated with contributions of digital assets into the Grayscale family of products ‘in-kind’ in exchange for shares, an acceleration of the recent trend, up from 71% in 2Q19.”

Grayscale stopped breaking out the percentage of crypto deposits into its trusts after 2019, and just stated everything in dollars. They may want to break out the numbers again, as this is something the SEC might be interested in.

Crypto lender BlockFi’s reliance on the GBTC arbitrage is well known as the source of their high bitcoin interest offering. Customers loan BlockFi their bitcoin, and BlockFi invests it into Grayscale’s trust. By the end of October 2020, a filing with the SEC revealed BlockFi had a 5% stake in all GBTC shares.

Here’s the problem: Now that GBTC prices are below the price of bitcoin, BlockFi won’t have enough cash to buy back the bitcoins that customers lent to them. BlockFi already had to pay a $100 million fine for allegedly selling unregistered securities in 2021.

As of September 2021, 47 mutual funds and SMAs held GBTC, according to Morning Star. Cathie Wood’s ArkInvest is one of the largest holders of GBTC. Along with Morgan Stanley, which held more than 13 million shares at the end of 2021.

Such a lovely place

Grayscale was happy to take investor money during the bitcoin bull runs of 2017 and 2020-21 and saturate the market with shares of GBTC. Anyone sitting on GBTC now is forced to take their losses, or hold out in the hopes Grayscale will do something to fix this.

Investors, many of whom are regular folks with GBTC in their IRAs, have every reason to be upset. Meanwhile, Grayscale is pointing the finger at the SEC as the reason we can’t have nice things.

Michael Sonnenshein, Grayscale’s chief executive, told Bloomberg he would even consider suing the regulator if Grayscale’s application to convert GBTC into a bitcoin ETF is denied.

Sonnenshein argues that because the SEC has approved bitcoin futures ETFs, it should also approve a bitcoin spot ETF.

This makes absolutely no sense. The two investment vehicles are totally different animals.

A bitcoin futures ETF indexes a bitcoin futures contract on the CME. It is a bet in dollars, paid in dollars. Nobody touches an actual bitcoin at any point. In contrast, Grayscale’s spot bitcoin ETF application represents an investment that is backed by bitcoins — not derivatives tied to it.

A spot bitcoin ETF is good for bitcoin, because it means more actual cash flowing into the cryptoverse. Crypto promoters are pushing hard for this. Bitcoin is a negative-sum game that relies on new supplies of fresh cash to keep it going.

But what happens if the SEC doesn’t approve Grayscale’s application?

Grayscale can issue more buybacks. In the fall of 2021, DCG began buying back over $1 billion worth of GBTC. In March 2022, it announced another $250 million in buybacks for Grayscale trusts. The effort had little impact. GBTC continued to trade well below the price of bitcoin.

As Morning Star points out, Grayscale has the power to make this right. It can redeem shares at NAV and simply return investors their cash or bitcoin. That is, if Grayscale really does care about crypto investors.

Grayscale offered a redemption program before 2016. However, the SEC issued a cease and desist order because the repurchases took place at the same time the trust was issuing new shares, in violation of Regulation M.

The situation is different now. Grayscale stopped issuing new shares in March 2021. That leaves the door open for it to pursue a redemption program and bring GBTC closer inline with the price of bitcoin.

I doubt this will ever happen. Grayscale is sitting on a cash cow. As long as it can redirect investor anger at the SEC, why change?

“There is no obligation to convert to an ETF,” David Fauchier, a fund manager at London’s Nickel Digital Asset, told me in a tweet. “If things stay as they are, they will print money into perpetuity basically, it’s a FANTASTIC business if BTC doesn’t zero.”

Ha. No, the status quo is to keep the trust as is. There is no obligation to convert to ETF. If things stay as they are, they will print money into perpetuity basically, it’s a FANTASTIC business if BTC doesn’t zero

Fed by stimulus money, tethers, and a new grift in the form of NFTs, the price of bitcoin reached a record of nearly $69,000 in November 2021. Bitcoiners rah-rahed the moment.

However, the same network effects that brought BTC to its heights are working in reverse and can just as easily bring it back down again. At its current price of $40,000, amidst 8.5% inflation, bitcoin is not proving itself to be the inflation hedge Grayscale hyped it up to be.

I encourage anyone reading this to submit your comments to the SEC regarding Grayscale’s application for a spot bitcoin ETF. Jorge Stolfi, a computer scientist in Brazil, has provided an excellent example, and so has David Rosenthal, also a computer scientist. You can submit your own comments here.

Did you enjoy this story? Consider supporting my work by subscribing to my Patreon account for as little as $5 a month. It’s the cost of a cup of coffee! Or, if you’re feeling generous, you can buy me a pound of coffee beans.

As you know, I left my most recent full-time gig, so I’m solo again. I’m going to keep on writing, but I need to figure out how to make ends meet. I’ll be writing more for my blog, possibly writing some e-books, and relying on support from patrons. If this newsletter is worth buying me a latte every four weeks, consider becoming a monthly supporter.

Now, on to the news. Since I didn’t write a newsletter last week, a few of these items stretch beyond the last seven days.

Filming for Quadriga documentary

Filming at a coffee shop in Vancouver Monday.

If you’ve been following me on Twitter, you know I was in Vancouver all weekend filming for an upcoming Quadriga documentary for Canadian public broadcast station CBC. It was a whirlwind adventure, loads of fun, and I got to meet my idol and fellow nocoiner David Gerard for the first time. He is 6’4″, which helps explain why he is not easily intimidated by anyone. (My blog, David’s blog with more pics.)

On our second day of filming, the crew got shots of David and me at a coffee shop going through my Quadriga timeline in detail. Of course, the more we talked and went over things, the more unanswered questions we came up with.

Ripple has been paying Moneygram millions

Moneygram’s 8-K filing with the SEC must be a bit of an embarrassment for Ripple CEO Brad Garlinghouse. It reveals Ripple paid $11.3 million to Moneygram over the last two quarters. That’s in addition to the $50 million Ripple has already invested in the firm. (Cointelegraph, Coindesk.)

This is apparently the ugly truth to how Ripple works. The company appears to pay its partners to use its On-Demand Liquidity (formerly xRapid) blockchain platform and XRP tokens and then say nice things about how well things are going. (FT Alphaville)

Of course, none of this is news to @Tr0llyTr0llFace, who wrote about how Ripple pays its partners in his blog a year ago. “Basically, Ripple is paying its clients to use its products, and then pays them again to talk about how they’re using its products,” he said.

Ripple class-action to move forward

In other Ripple news, a federal judge in Oakland, Calif., has granted in part and denied in part Ripple’s motion to dismiss a class-action lawsuit claiming the company violated U.S. securities laws. There’s a lot to unpack here, but overall it’s a win for the plaintiffs. In other words, the lawsuit will proceed even though it’s been trimmed back a bit. (Court order, CoinDesk, Bloomberg)

Ripple had claimed in its November court filing that the suit could topple the $10 billion market for XRP. Well, yeah, one would think so, especially if XRP is deemed a security and gets shut down by the SEC. This class action may be laying the groundwork for that.

Reggie Fowler gets hit with another charge

As if Reggie Flower did not have enough trouble on his hands. After forgoing a plea deal where three out of four charges against him would have been dropped, prosecutors have heaped on another charge — this one for wire fraud.

They allege that Fowler used ill-gotten gains from his shadow banking business, which he ran on behalf of Panamanian payment processor Crypto Capital, to fund a professional football league. The league isn’t named in the indictment, but a good guess says its the collapsed American Football League of which Fowler was a major investor. (My blog.)

The new charge should come as no surprise to those following the U.S. v. Fowler (1:19-cr-00254) case closely. In a court transcript filed in October 2019, Assistant U.S. Attorney Sebastian Swett told Judge Andrew Carter:

“We have told defense counsel that, notwithstanding the plea negotiations, we are still investigating this matter, and, should we not reach a resolution, we will likely supersede with additional charges.”

Fowler needs to go before the judge and enter his plea on the new charge before he can proceed to trial. Federal prosecutors are asking the judge to schedule arraignment for May 5, but it’s quite possible this is a typo and they meant March 5. (Court doc.)

Convicted fraudster won’t be buying Perth football team after all

LFE founder Jim Aylward on Twitter

The sale of Perth Glory Soccer Club to a London crypto entrepreneur fell through after it turned out that the man behind the company trying to buy Glory — businessman Jim Aylward — is convicted fraudster James Abbass Biniaz. (Imagine that, a person with a criminal past getting involved in crypto?)

Aylward had set up a group called London Football Exchange, a football stock exchange and fan marketplace powered by the LFE token. The grand scheme was for the company to buy soccer teams all over the world and integrate that business with the token.

Glory owner Tony Sage pulled out of the deal after traveling to London to go through a due diligence process with his lawyers and representatives of the London Football Exchange group. Sage had been promised $30 million by Aylward for 80% of the A-League club. (Sydney Morning Herald)

Here’s a recording of Aylward admitting the price of LFE is totally manipulated. “We control about 95% of the token holders,” he said.

Weird stuff happening with e-Payments

Something funny is going on with e-Payments, one of the biggest digital payments firms in the U.K. The London firm, which caters to the adult entertainment, affiliate marketing, and crypto industries, was ordered by the U.K.’s Financial Conduct Authority to suspend its activities as of Feb. 11 due to loose anti-money-laundering controls. That’s left ePayments’ customers unable to access their funds. Robert Courtneidge, one of its e-Payments’ directors stepped down the following week. Nobody knows why, but it looks like he was previously involved with the OneCoin scam. (FT Alphaville)

(BTW, on my flight back from Vancouver, I listened to the Missing Crypto Queen BBC podcast, which is all about OneCoin, and it’s fantastic. Definitely worth a listen.)

SEC shoots down another bitcoin ETF; Hester Pierce chimes in

In a filing posted Wednesday, the SEC set aflame another bitcoin ETF proposal. The regulator claims Wilshire Phoenix and NYSE Arca had not proven bitcoin is sufficiently resistant to fraud and market manipulation. (Their idea was to mix bitcoin and short-term treasuries to balance out bitcoin’s volatility, but the agency still wasn’t keen.) The SEC has rejected all bitcoin ETFs put before it to date, so there’s no new news here.

Predictably, though, SEC Commissioner Hester Pierce, aka “crypto mom,” filed her statement of dissent. She said the agency’s approach to bitcoin ETFs “evinces a stubborn stodginess in the face of innovation.” For some reason, Pierce seems to consistently confuse innovation with anarchy and giving bad actors free rein.

Speaking of which, she recently posted on Coindesk asking for suggestions to her ICO “safe harbor” plan. Attorney Preston Byrne responded, saying it would be hilarious if it weren’t so serious. He thinks the plan should be tossed in the bin.

other SEC commissioners: "no, 2+2 still makes 4" Hester Peirce: "I think sophisticated market investors can judge for themselves if it makes 5, or even 6. As Bruce Springsteen sung, 'it's just like Sister Ray said.'"

Canada’s central bank plans to lay the foundation for its own digital currency should the day arise where cash no longer rules. In a speech he gave in Montreal, Deputy Governor Tim Lane said there isn’t a compelling case to issue a central bank-backed digital currency right now, but the Bank of Canada is starting to formulate a plan in the event Canadian notes and coins go out of style. (Calgary Sun.)

Despite so many countries jumping into the game, central bank digital currencies are nothing new. They have been around since the 1990s, only nobody cared about them until Facebook’s Libra popped into the scene. Bank of Finland’s Alexi Grym recently did a podcast, where he talks about how the country launched its own Avanti project (a form of CBDC) in 1993. The idea sounded great in theory, but in practice, consumers didn’t like being charged to load the cards, especially since ATM withdrawals were free.

Drug dealer loses all his bitcoin

The problem with keeping track of the keys to your bitcoin is that it’s just too easy to lose them, as this U.K. drug dealer demonstrates. He jotted down the keys to his illicit $60 million BTC on a piece of paper. But then when he went to jail, his landlord gathered up all his belongings and took them to the dump. (Guardian.) This isn’t the first time millions of dollars worth of bitcoin have ended up in a trash heap.

FCoin insolvency bears hallmarks of funny business

FCoin, a crypto exchange based in Singapore, announced its insolvency on Feb. 17 after making the surprise discovery it was short 7,000 to 13,000 bitcoin—worth roughly $70 million to $130 million. The exchange blamed the shortage on a cacophony of errors following the launch of a controversial incentive program called “trans-fee mining.” There has been a lot of speculation that this was an outright scam. Now a new report by Anchain.ai shows BTC leaving the exchange’s cold wallets in droves right before FCoin shuttered and its founder Zhang Jian happily moved on to start a new business.

Quadriga was using Crypto Capital

The law firm representing QadrigaCX’s creditors believes the failed Canadian crypto exchange was funneling money through Crypto Capital. Financial documents that two former Quadriga users posted on Telegram show that to be true. (My blog)

Next question: Was Crypto Capital holding any Quadriga funds at the time the exchange went under? That’s going to be hard to track down given the exchange had no books.

Buffett still thinks crypto is a joke

Tron CEO Justin Sun paid $4.6 million to spend three hours with Warren Buffett and turn him into a crypto fan. He even gave the multi-billionaire some bitcoin. Turns out Buffett, promptly handed those BTC over to charity. He doesn’t want anything to do with bitcoin and still thinks crypto has zero value. “What you hope is someone else comes along and pays you more money for it, but then that person’s got the problem,” he told CNBC.

Steven Segal pays the price of being a shitcoin shill

Steven Segal thought he would bring in a little extra dough by shilling a shitcoin, but the effort backfired. The Hollywood actor has agreed to pay $314,000 to the SEC for failing to disclose payments he received for touting an ICO conducted by Bitcoiin2Gen (spelled with two “i”s) in 2018. He’ll pay a $157,000 disgorgement, plus a $157,000 fine on top.

How long does a blockchain need to be shut down for before it’s considered dead? How is it even possible to shut down something that is decentralized? Oh, wait, maybe it’s not.

IOTA has been offline for 14 days and counting ever since the IOTA Foundation turned off its coordinator node, which puts the final seal of approval on any IOTA currency transactions, to stop an attacker from slurping up funds from its wallet service.

The project has put together a tedious three-part series explaining the theft of its Trinity wallet, its seed migration plan and all the lessons it’s learned from the mishap. It’s all a bit mind-numbing, and you’ll feel a little dead after you read it, too.

Anyway, now the network, which they originally sold as (and spent years claiming was) decentralized has been down for nearly 2 weeks.

Anyway, now the network, which they originally sold as (and spent years claiming was) decentralized has been down for nearly 2 weeks.

“Absurd” isn’t the word I would use to describe the situation.

As if Reggie Flower did not have enough trouble on his hands. After

As if Reggie Flower did not have enough trouble on his hands. After

FCoin, a crypto exchange based in Singapore,

FCoin, a crypto exchange based in Singapore,