On August 14, Celsius filed a Budget and Coin Report, which put into full view the ongoing train wreck. The company is burning through piles of “cash,” while creditors watch in horror as their remaining hopes of recovering lost money go up in smoke before their eyes. [Docket 447]

To generate 18% returns on its Earn product, Celsius dived head-first into some stunningly risky “investments” and lost $1.2 billion in customer funds, at least. The company filed for Chapter 11 on July 13.

Now, Celsius founder Alex Mashinsky wants creditors to put their faith into another reckless gamble. The company is shifting its entire business model from crypto lending to bitcoin mining — with ludicrous plans to mine its way out of bankruptcy.

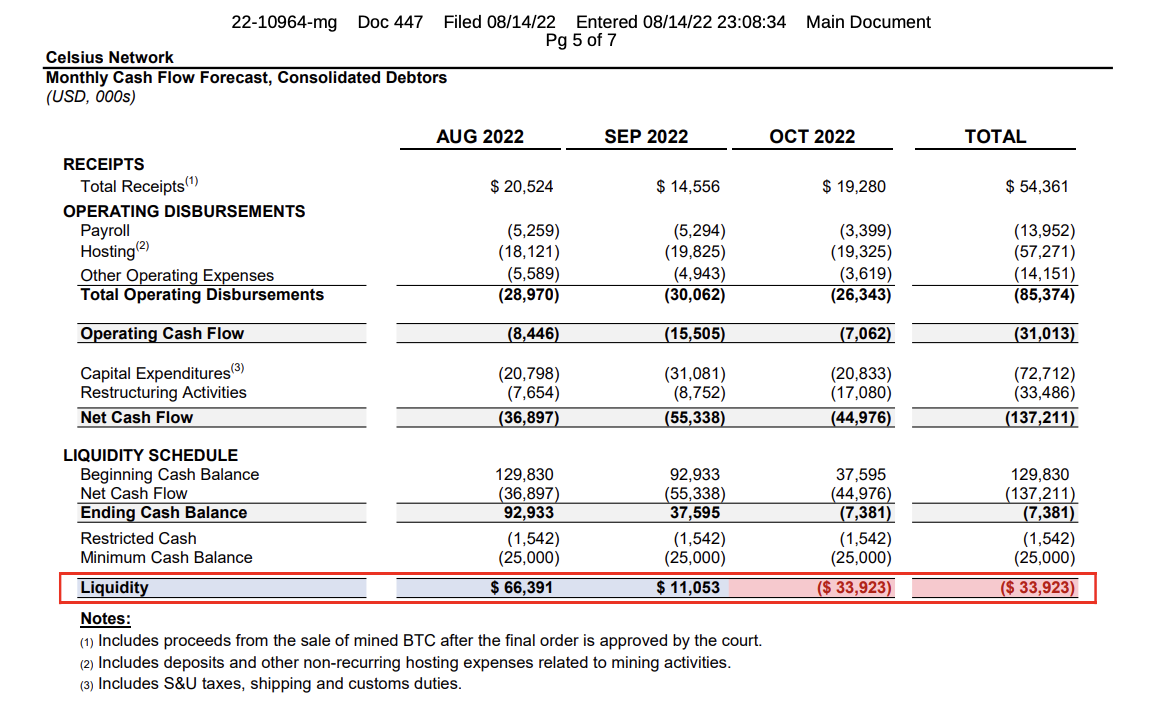

Over a three-month period from August through October, Celsius is allocating $14 million to payroll, $57.3 million to mining,* and $33 million to restructuring costs. By the end of October, Celsius will be operating hugely in the red.

Bitcoin mining is a money-losing proposition, as David Gerard and I detailed in an earlier report. Celsius’ mining business, headquartered in Texas, is currently burning through $19 million of customer money per month. In July, they only mined 432 BTC, worth $8.6 million!

Celsius argues this is because its facilities aren’t fully operational yet — but the facilities will be fully operational if the court will allow them to keep throwing more money into the flames.

All Celsius and its lawyers need to do is to convince creditors — and the judge — that the business will be profitable one day in the fabulous future.

On August 16, two days after filing its budget report, Celsius had its second-day bankruptcy hearing. The judge ultimately signed off on a motion allowing Celsius to sell mined bitcoin to fund its mining operations but withheld approving a motion authorizing the debtor to sell stocks and shares due to Celsius obfuscating what they were really selling.

What follows are my notes and comments on the hearing.

Second-Day Hearing

Judge Martin Glenn began the two-hour hearing by noting that the court has received hundreds of letters from Celsius customers. The letters are all being filed in the docket. “Some have raised important issues that will have to be addressed in this case,” he said.

Molly White has been pulling out excerpts of these letters, and they are indeed heart-wrenching. These are real people, some of whom have lost their life savings because they believed the promises of Celsius founder Alex Mashinsky. [Molly White]

Celsius’s lead lawyer at Kirkland & Ellis, Josh Sussberg, was the first to present at the hearing. Before delving into a nine-page PowerPoint, he took a moment to rant about the “relentless” and “inaccurate” media coverage surrounding the bankruptcy. Sussberg said he’s told Celsius “to take the repeated punches,” and not respond. [Celsius presentation]

Sussberg has clearly been in close talks with Mashinsky, who has a pattern of deflecting blame. When Celsius initially filed for bankruptcy, Mashinsky pinned his company’s failure on “misinformation” in the media and on social media for encouraging customers to withdraw $1 billion in funds over five days in May. Mashinsky’s new message is that the banks are lying, the media is lying, but you can trust me with your money, even though I just lost it all.

Sussberg noted the elephant in the room: everyone knows that Celsius will run out of money by the end of October. He said that Celsius is working to expedite a restructuring plan that will lead to the company being liquid.

Celsius is also trying to sell its business and its digital assets to a third party. “We have multiple offers outstanding with several more coming in,” said Sussberg.

In addition to the official unsecured creditors’ committee, two ad-hoc creditors’ groups have formed. One is for custodial holders, represented by Togut, Segal & Segal. They have $180 million in claims. The other, represented by Troutman Pepper, is for withhold account holders. These were customers in states where Celsius was not licensed. When they tried to withdraw funds, the money went into holding accounts. They represent $14.5 million in claims. Kirkland has been in talks with both groups, Sussberg said.

Celsius is not seeking to dollarize claims on the petition date. Instead, it wants to return crypto. In other words, Celsius is counting on the markets to rebound — i.e., bitcoin will moon again and everyone’s problems will be solved.

Interestingly, the creditors also do not want to dollarize claims. Greg Pesce at White & Case, the lead lawyer for the creditors’ committee, said that they too want an in-kind recovery of coins.

Pesce said the committee has begun its own investigation into Celsius in the hopes of recovering more money for creditors, as they believe they are the only ones able to fight for the customers’ interests. Their search will take them “across the globe, across the country, and across the blockchain.”

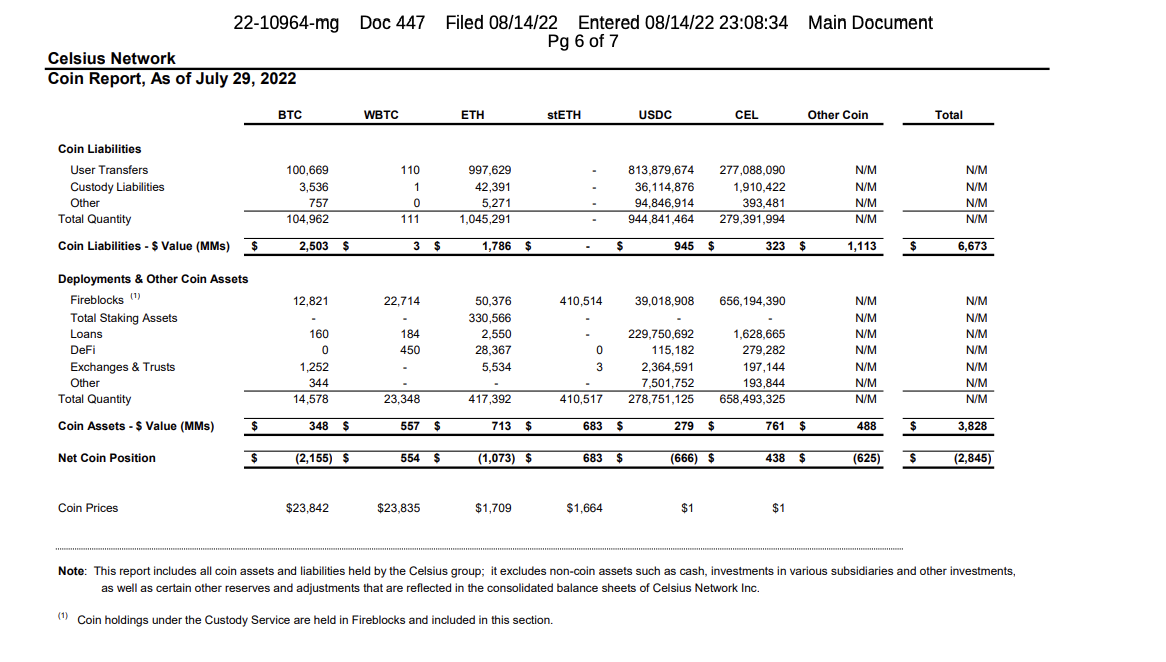

In addition to the possibility of identifying potential insider trading, Pesce seems to be alluding to the Tether loan. Tether loaned Celsius $840 million in USDT backed by bitcoin, and then sold the bitcoin Celsius loaned as collateral just before Celsius filed for bankruptcy. Any attempts to retrieve that bitcoin will be a sideshow in and of itself.

Judge Glenn notes that Celsius’ Earn product attracted lots of government investigations into whether Celsius was selling unregistered securities. The Securities and Exchange Commission has been looking into Celsius since January. Celsius had already been thrown out of Alabama, New Jersey, Texas, and Kentucky for unregistered offerings of securities.

“Since the debtor business model was so heavily dependent on the so-called Earn accounts, and given the number of securities regulator investigations as to whether the debtors were engaged in the sale of unregistered securities, what is the business model going forward?”

“That’s the $64,000 question,” Pesce responded.

Celsius had 1.7 million customers at the time it filed its petition. About 58,000 held crypto in Celsius’ custody accounts — they might get their crypto back first depending on whether they are deemed secured or unsecured creditors.

Judge Glenn wants to resolve the custodial accounts sooner rather than later. But Celsius didn’t set up its custodial business until April 2022, and he wants to make sure custodial accounts weren’t a vehicle for insider trading:

“I am certainly going to want to know whether there are insiders and employees with custodial accounts and whether any of them were able to transfer crypto assets from other accounts into the custodial accounts — and what did they know at the time they made the transfer? Were they contemplating that the business was trending negative and the best way for them to individually protect the value of their accounts was to try and transfer assets into custodial accounts?”

Judge Glenn previously ordered all versions of Celsius’ terms of service going back to 2018. He wanted to trace through all of the changes made over time to determine what is and what isn’t the property of the bankruptcy estate. “Little did I know there were going to be 1,100 pages of them,” he said.

Bitcoin sell motion

After the presentations, the hearing moved on to the motions.

Celsius wants to sell bitcoin generated by its mining business and use the cash to fund its mining operations. “We are still in the capital-intensive part of the business and also, importantly, we don’t have all of the mining rigs,” said Sussberg.

US Trustee attorney Shara Cornell said the Trustee needs more information to form an opinion on the matter: “As of today, we still do not know what expenses are being paid or what bitcoin is being sold,” she said. “We know what the debtors expect to generate but we have no idea what it is going to cost to generate any of that.”

Cornell said that the Trustee is considering hiring an examiner to address Celsius’ rampant transparency issues. She noted that Celsius said it planned to file a long-term mining plan. “Maybe what we need to do is put this motion on hold until we have more information.”

(Update: Just after I published this story, the Trustee entered a motion for the appointment of an examiner. This is a big deal!)

Surprisingly, Pesce said the creditors’ committee has not made a decision on the mining. Frankly. I was sort of expecting the creditors to push for a liquidation.

Not all Celsius customers support the idea.

If they raised a virtual hand during the Zoom hearing, creditors were allowed to speak. One creditor said: “We didn’t sign up to be part of the mining business. We signed up to be part of an exchange. As a fellow miner, I don’t see it being very profitable in the long run.”

Judge Glenn approved a motion to allow Celsius to sell bitcoin generated from its mining business, but he clearly had reservations: “At bottom, this is a business judgment decision that may turn out to be very wrong, but we will see.” [Order 187]

Not so ‘de minimis’ after all

Celsius wants to sell assets that they claim are “de minimis” and “non-core” to the business to bring in more cash for operating expenses. It turns out these are notes/bonds and equity in other crypto companies, but Celsius never bothered to tell anyone.

De minimus means too small to be taken into consideration. Debtors can sell assets free and clear of liens. But sales of bankruptcy estate property must be approved by the bankruptcy court.

Prior to the hearing, the Trustee had objected to the motion, saying the debtor hadn’t provided enough information for the Trustee to evaluate the motion. [Docket 400]

Trustee attorney Shara Cornell told Judge Glenn: “The motion makes it sound like the debtor is selling office furniture or similar hard-type assets that they no longer need. One of our questions in objection had to do with whether or not that might be mining equipment. But what they are actually looking to sell are equities and stocks. And that, in our opinion, is not a de minimis.”

Judge: “Did you find out what stock they were talking about?” Cornell: “No.”

Judge Glenn declined to approve the de minimis sales motion and told Celsius to work it out further with the Trustee. Even he was surprised.

“Certainly I had no inkling the debtor was proposing to sell millions of dollars of equity or notes/investments in other crypto businesses. Those were not what I would normally consider to be de minimis assets, so I want some better definition.”

Celsius’ business model going forward is all predicated on number go up and making sure the boys get paid. I’m not sure how long this will drag on before the “restructuring” turns into a liquidation, and Celsius management is booted. Likely not before Celsius burns through the rest of their customers’ funds, pays as many of their friends as possible, and the bankruptcy attorneys make their millions.

The next Celsius hearing is September 1.

*Celsius calls running mining rigs “hosting.”

If you like my work, consider supporting my writing by subscribing to my Patreon for $1, $5, $20, $50, or even $100 a month.