The Securities and Exchange Commission is being inundated by thousands of comments solicited by Grayscale to support the conversion of their Grayscale Bitcoin Trust (GBTC) into a spot bitcoin ETF. [Comments on NYSE Arca Rulemaking]

As part of the filing, the SEC provides a comment period of 240 days. NYSE Arca filed the application on October 19, 2021, so the last day for comments is June 16.

Bitcoin skeptics refer to GBTC as the Bitcoin Roach Motel or Hotel California, a place you can check in but never leave because once bitcoin goes into the trust, it has no obvious way of getting out. I covered the details of how the trust works in an earlier blog post. [Amy Castor]

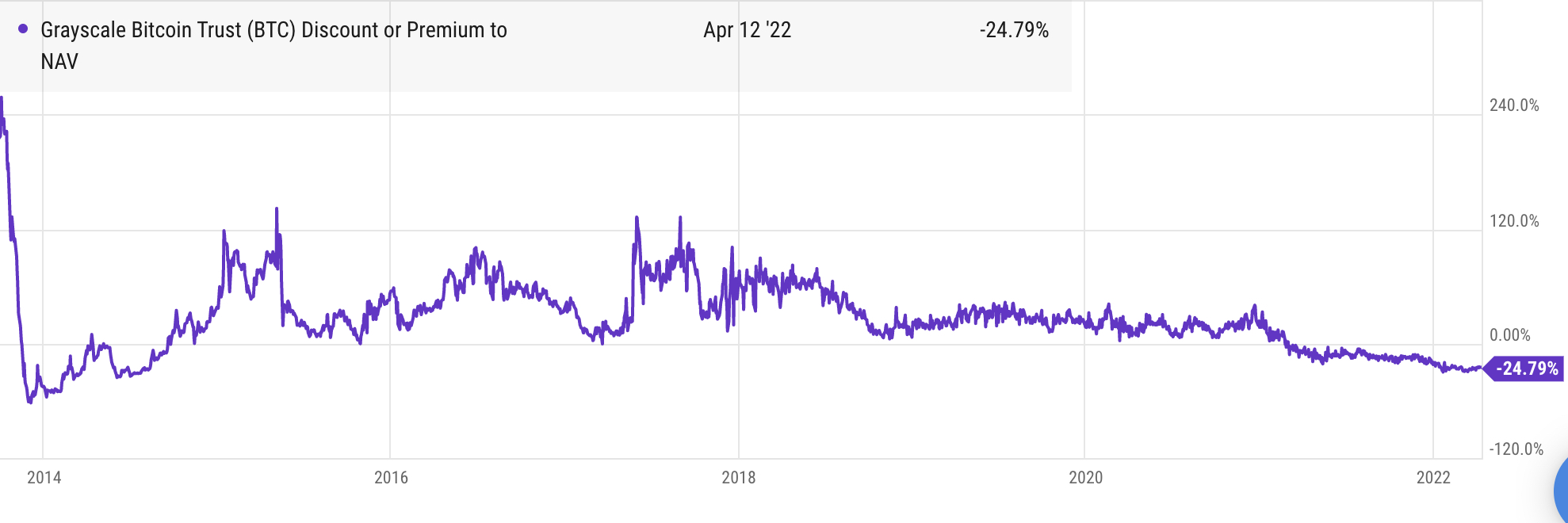

GBTC is currently trading at 25% below the price of bitcoin. Grayscale argues that converting it to a spot bitcoin ETF will allow GBTC to trade in line with its underlying asset.

In truth, Grayscale can redeem shares and return investors their money, but it stands to make hundreds of millions of dollars more with an ETF, so you should definitely spam the SEC instead!

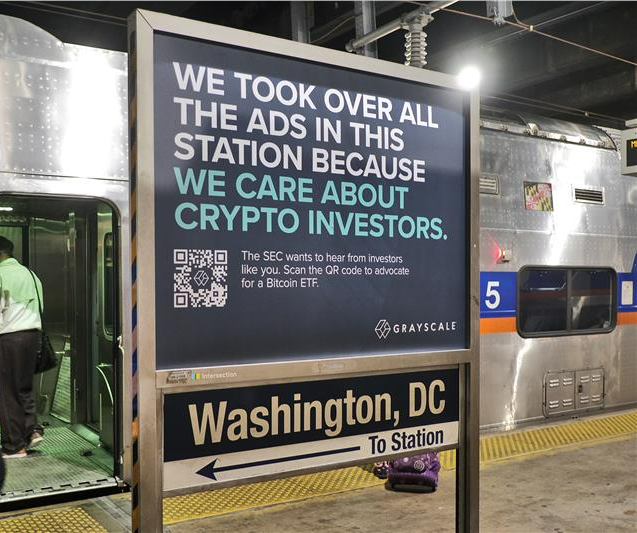

Grayscale has encouraged spamming the commission through a massive ad campaign at Amtrak stations. Grayscale CEO Michael Sonnenshein is going around giving press interviews, pointing out how mean and evil the SEC is for never having approved a spot bitcoin ETF in the past.

On its website, Grayscale offers a link that opens up directly to a ready-made email, making it mindlessly easy to spam the SEC in a few simple clicks.

Jorge Stolfi, a computer scientist in Brazil, has been reading through the SEC comments one by one and posting his thoughts on Twitter.

Nearly 4,000 comments have been submitted so far, and 98% of them are positive in that they support converting GBTC to a bitcoin ETF. Some of the names look suspiciously made up.

Thousands of the comments are copies of the same Grayscale spam message, and many don’t even bother to edit the “[YOUR NAME HERE]” placeholders.

Thanks to the torrent of spam letters to the SEC re making GBTC into an ETF, I learned two more financial terms: "contango" and "backwardation".

I feel embarrassed for having to learn them from guys who cannot even edit "***[YOUR NAME HERE]***" placeholders in spam messages.

Many of the comments parrot Sonnenshein’s remarks to the press about how the SEC has approved a bitcoin futures ETF; therefore, it should also approve a spot. (This is nonsense. The former is an actual bet on dollars. Nobody touches BTC at any point in the process.)

Hopefully, the SEC will read the spam comments and understand them for what they are: clear evidence that thousands of GBTC investors do not understand the nature of bitcoin, and that GBTC should not be converted to an ETF for the sake of those same investors.

In reading through the comments something else becomes alarmingly clear — many retail investors are stuck with GBTC in their retirement accounts. Thanks to a television ad campaign that Grayscale ran in 2020, many falsely believed that bitcoin was a hedge against inflation, rather than an incredible risky and volatile asset.

Amongst the positive comments, Coinbase submitted a ridiculously long (27 pages) letter trying to demonstrate that the bitcoin market cannot be manipulated. They somehow forgot to mention the 83 billion tethers currently sloshing around in the crypto markets. [SEC Comment]

Last year, Coinbase settled charges with the CFTC that one of its own employees was wash trading the vast majority of a certain coin’s volume on their own exchange, and they apparently weren’t aware of it until much later. I’m sure they have a lot of credibility on this subject!

Voices against the GBTC conversion

There are a few powerful letters to the SEC against the conversion. These are definitely worth a read for anyone who wants to get a better understanding of how GBTC works.

Writing on behalf of a client, Ropes & Gray Attorney David Hennes does a fantastic job underscoring how Grayscale is royally screwing over GBTC holders. [SEC Comment]

As Hennes points out, Grayscale bought $700 million worth of its own GBTC shares at a discount and is authorized to buy back $1.2 billion.

If GBTC converts to an ETF, Grayscale would then be authorized to sell the corresponding bitcoins at the market price, thus making some $200 million to $350 million in profit at the expense of those who sold them the shares at discount.

Since Grayscale is no longer issuing shares of GBTC, it can redeem GBTC at net asset value without running afoul of Regulation M, as it had in the past. However, it chooses not to because it is collecting a 2% management fee on $25 billion in BTC assets held in the trust.

“The SEC should thus deny the conversion of GBTC into an ETF unless and until Grayscale first (a) initiates a redemption program for GBTC that complies with Regulation M; and (b) agrees to distribute to GBTC’s other shareholders on a pro-rata basis any and all gains resulting from any Grayscale purchases of GBTC shares at a discount and corresponding sales of GBTC shares on an undiscounted basis,” wrote Hennes.

Computer scientist David Rosenthal, who gave a popular lecture at Stanford warning about the hazards of crypto, says all of the reasons the SEC had for rejecting previous bitcoin spot ETFs — and there have been close to a dozen of them — are still valid.

“The constant pressure to approve a spot Bitcoin ETF exists because Bitcoin is a negative-sum game. Bitcoin whales need to increase the flow of dollars in so as to have dollars to withdraw. The SEC should not pander to them.” [SEC Comment]

Rosenthal also comments on my Grayscale story in his blog. [DSHR blog]

Along that same vein, David Golumbia, author of “The Politics of Bitcoin,” warns “manipulators in the crypto space need a constant inflow of real dollars to prop up their manipulation so that they can continue to dump their tokens into the hands of ever more unsuspecting consumers. That they are obviously engaged in selling their own tokens for a profit while bullying others into buying at the same time is only one of many tactics they use that are illegal in well-ordered markets.” [SEC Comment]

In his own submission, Stolfi states that bitcoin is a tool of crime. It allows dark markets to exist and flourish. It has taken the place of the now-defunct criminal bank Liberty Reserve. And it functions as a natural Ponzi. [SEC comment]

“Bitcoin does not provide any benefits for society; on the contrary, it has caused enormous damage; and this balance cannot ever improve, because the technology is inherently wasteful, impractical, illegal, and insecure.”

Someone going by “Concerned Citizen of the Word” noted that “It’s just a matter of time before the Bitcoin bubble pops due to any of many reasons, and a lot of people, especially Americans, are going to lose massively.” [SEC comment]

If you are similarly disturbed by Grayscale’s campaign of misinformation, I encourage you to write to the SEC and make your own voice heard — with original commentary, which I’m sure they would appreciate. You can submit your comments here.

If you like my work, consider supporting my writing by subscribing to my Patreon account for $5 or $20 a month. Every little bit helps.

If you happen to be taking Amtrak and pass through Penn Station or Union Station, you will notice something unusual: every available ad space has been taken up by Grayscale.

“We care about crypto investors,” the crypto asset manager says in its ads. Grayscale is urging the public to write to the Securities and Exchange Commission and convince them to approve the first spot bitcoin ETF in the U.S.

Grayscale wants to convert its Grayscale Bitcoin Trust (GBTC) into a bitcoin ETF after flooding the market with shares. GBTC is trading 25% below its net asset value, and investors are rightfully pissed off. Grayscale wants them to be upset with the SEC, but the regulator isn’t really to blame. If anything, the SEC should have warned the public about GBTC years ago.

Over the last eight years, Grayscale has been telling investors to buy shares of GBTC, advertising the fund as a way to get exposure to bitcoin without having to buy bitcoin.

Accredited investors plowed dollars (or maybe bitcoins) into the fund all through 2020, looking to take advantage of an arbitrage opportunity. They could buy in at NAV, and after a 6 to 12-month lockup, sell on the open market for a premium. All through 2020, that premium was around 18%, on average.

Everybody was happy until February 2021, when the Purpose bitcoin ETF launched in Canada. Unlike GBTC, which trades over-the-counter, Purpose trades on the Toronto Stock Exchange, close to NAV. At 1%, its management fees are half that of GBTC. Within a month of trading, Purpose quickly absorbed more than $1 billion worth of assets.

Demand for GBTC dropped off and its premium evaporated. Currently, 653,919 bitcoins (worth a face value of $26 billion) are stuck in an illiquid vehicle. Welcome to Grayscale’s Hotel California.

The plan all along, Grayscale claims, has been to convert GBTC into a bitcoin ETF. On October 19, 2021, NYSE Arca filed Form 19b-4 with the SEC. The regulator has until early July to respond.

In all probability, the SEC will reject the application, just as it has every single spot bitcoin ETF application put before it to date.

Bitcoin’s price is largely determined by wash-trades, whales controlling the market, and manipulation with tethers. SEC Chair Gary Gensler knows this. He taught a course in blockchain and money at MIT Sloan before his appointment by the Biden administration.

This is Grayscale’s second time around. It applied for a bitcoin ETF in 2016, but withdrew the application during the 2017 bitcoin bubble because “the regulatory environment for digital assets had not advanced to the point where such a product could successfully be brought to market.” Meanwhile, the trust’s assets under management grew as did Grayscale’s profits.

Closed-end fund

“Inflation is rising, we need to diversify!” a panicked woman tells her son over the phone in the middle of the night. “I’m buying crypto!” She hangs up. Her son rolls over in bed. The scene is from a series of TV commercials Grayscale ran in 2020 to convince the public that GBTC was a sound investment.

Digital Currency Group is the parent company of Grayscale. Both firms were founded by Barry Silbert. DCG is invested in hundreds of crypto firms. It owns crypto outlet CoinDesk, which essentially functions as a PR machine for the entire crypto industry.

Initially called the “Bitcoin Investment Trust,” GBTC launched in September 2013. It was promoted as an investment vehicle that would allow hedge funds and institutional investors to gain exposure to bitcoin, without having to deal with custody. Coinbase has been the custodian of the fund since 2019 when it bought Xapo, the previous custodian.

Legally, GBTC is a grantor trust, meaning it functions like a closed-end fund. Unlike a typical ETF, there is no mechanism to redeem the underlying asset. The SEC specifically stopped Grayscale from doing this in 2016. Grayscale can create new shares, but it can’t destroy shares to adjust for demand. Grayscale only takes bitcoin out to pay its whopping 2% annual fees, which currently amount to $200 million per year.

In contrast, an ETF trades like a stock on a national securities exchange, like NYSE Arca or Nasdaq. An ETF has a built-in creation and redemption mechanism that allows the shares to trade at NAV via arbitrage. Authorized participants (essentially, broker-dealers, like banks and trading firms) issue new shares when the ETF trades at a premium and redeem shares when they trade at a discount, making a profit on the spread.

How it all works

Grayscale periodically invites rich investors to pledge money into the fund in private placements at its discretion. The minimum investment is $50,000. Grayscale uses the cash to buy bitcoin and issues shares of GBTC in kind.

Investors can also pledge bitcoin directly — a great advantage if you happen to be a large holder who wants to unload your BTC without crashing the market. (More on this later.)

After a lockup period, investors can sell their GBTC on the open markets. Anyone can buy and sell GBTC on OTC Markets Group, the main over-the-counter marketplace, or via a brokerage account, like Schwab or Fidelity.

Up until early last year, GBTC has typically always traded at a premium on the open market. That premium occasionally soared to over 100%. During the 2017 bitcoin bubble, GBTC traded as high as 130% above NAV.

Why would anyone pay the premium? Many institutional investors can’t buy bitcoin directly for compliance reasons. And there are a lot of individuals who don’t want the headache of figuring out how to set up a bitcoin wallet. GBTC was initially the only option for getting exposure to BTC, without having to buy BTC, at least until bitcoin futures came along. However, bitcoin futures contracts came with their own risks, costs, and headaches. GBTC was easier.

In early 2020, GBTC became an SEC reporting company. This allowed investors who purchased shares in the trust’s private placement to sell their shares in 6 months instead of the previous 12 months. You could now make more money faster!

Unsurprisingly, the trust went into overdrive in 2020. Starting in January 2020 up to Feb. 23, 2021, Grayscale filed 35 reports with the SEC indicating that it sold additional shares to accredited investors, according to Morning Star’s Bobby Blue.

The trust’s holdings doubled from roughly 261,000 BTC in January 2020 to 544,000 BTC by mid-December 2020, per Arcane Research.

The @Grayscale Bitcoin Trust has attracted new investors throughout the year, leading to a doubling of Grayscale's BTC holdings from approx. 261k BTC in January to 544k BTC by Dec 12th.

Harris Kupperman, who operates a hedge fund, explained in a November 2020 blog post how GBTC’s arbitrage opportunity created a “reflexive Ponzi,” responsible for sending the price of bitcoin hyperbolic.

There were several versions of the arb. You could borrow money through a prime broker. You could use futures to hedge your bet. You could recycle your capital twice a year.

Every version involved Grayscale purchasing more bitcoin, thus increasing demand, widening the spread in the premium, and pushing the price of bitcoin ever higher. Between January 2020 and February 19, 2021, the price of BTC climbed from $7,000 to $56,000.

“When the spread is 26% wide and liquid to the tune of hundreds of millions per week, you can bet the biggest guys in finance are all over it,” Kupperman said. “As you can imagine, everyone big is putting on some version of this trade.”

Kupperman wasn’t the only person to raise alerts about the fund, which mainly benefited wealthy investors. As soon as GBTC launched, skeptics voiced their concerns.

“You can put a nice wrapper around a turd, and present it in a very well-manicured product to investors that you say is safe,” Barry Ritholtz, a wealth manager and founder of The Big Picture blog, told Verge. “But at the end of the day, it’s still crap.”

In September 2017, Citron Research called GBTC “the widow maker” and “the most dangerous way to own bitcoin.” Citron’s Andrew Left accurately predicted GBTC’s collapse:

“Citron believes that as new methods become available for investors to gain exposure to bitcoin — including traditional ETFs — that money will move to these regulated instruments and out of the uncertain waters of GBTC, which we believe can fall by 50% easily.”

Who holds GBTC?

The press has repeatedly credited Grayscale as a massive buyer of bitcoins, and evidence of institutional money entering the cryptoverse. This may not be the case.

Even though Grayscale states its holdings in dollars, it accepts deposits of bitcoins. A whale, or a good friend of Grayscale, can trade in their BTC for shares of GBTC, which they can flip six months later at well above the actual price of bitcoin.

The last time Grayscale broke out the numbers in Q3 2019, they said that the majority of deposited value into their family of trusts was in crypto, not dollars:

“Nearly 80% of inflows in 3Q19 were associated with contributions of digital assets into the Grayscale family of products ‘in-kind’ in exchange for shares, an acceleration of the recent trend, up from 71% in 2Q19.”

Grayscale stopped breaking out the percentage of crypto deposits into its trusts after 2019, and just stated everything in dollars. They may want to break out the numbers again, as this is something the SEC might be interested in.

Crypto lender BlockFi’s reliance on the GBTC arbitrage is well known as the source of their high bitcoin interest offering. Customers loan BlockFi their bitcoin, and BlockFi invests it into Grayscale’s trust. By the end of October 2020, a filing with the SEC revealed BlockFi had a 5% stake in all GBTC shares.

Here’s the problem: Now that GBTC prices are below the price of bitcoin, BlockFi won’t have enough cash to buy back the bitcoins that customers lent to them. BlockFi already had to pay a $100 million fine for allegedly selling unregistered securities in 2021.

As of September 2021, 47 mutual funds and SMAs held GBTC, according to Morning Star. Cathie Wood’s ArkInvest is one of the largest holders of GBTC. Along with Morgan Stanley, which held more than 13 million shares at the end of 2021.

Such a lovely place

Grayscale was happy to take investor money during the bitcoin bull runs of 2017 and 2020-21 and saturate the market with shares of GBTC. Anyone sitting on GBTC now is forced to take their losses, or hold out in the hopes Grayscale will do something to fix this.

Investors, many of whom are regular folks with GBTC in their IRAs, have every reason to be upset. Meanwhile, Grayscale is pointing the finger at the SEC as the reason we can’t have nice things.

Michael Sonnenshein, Grayscale’s chief executive, told Bloomberg he would even consider suing the regulator if Grayscale’s application to convert GBTC into a bitcoin ETF is denied.

Sonnenshein argues that because the SEC has approved bitcoin futures ETFs, it should also approve a bitcoin spot ETF.

This makes absolutely no sense. The two investment vehicles are totally different animals.

A bitcoin futures ETF indexes a bitcoin futures contract on the CME. It is a bet in dollars, paid in dollars. Nobody touches an actual bitcoin at any point. In contrast, Grayscale’s spot bitcoin ETF application represents an investment that is backed by bitcoins — not derivatives tied to it.

A spot bitcoin ETF is good for bitcoin, because it means more actual cash flowing into the cryptoverse. Crypto promoters are pushing hard for this. Bitcoin is a negative-sum game that relies on new supplies of fresh cash to keep it going.

But what happens if the SEC doesn’t approve Grayscale’s application?

Grayscale can issue more buybacks. In the fall of 2021, DCG began buying back over $1 billion worth of GBTC. In March 2022, it announced another $250 million in buybacks for Grayscale trusts. The effort had little impact. GBTC continued to trade well below the price of bitcoin.

As Morning Star points out, Grayscale has the power to make this right. It can redeem shares at NAV and simply return investors their cash or bitcoin. That is, if Grayscale really does care about crypto investors.

Grayscale offered a redemption program before 2016. However, the SEC issued a cease and desist order because the repurchases took place at the same time the trust was issuing new shares, in violation of Regulation M.

The situation is different now. Grayscale stopped issuing new shares in March 2021. That leaves the door open for it to pursue a redemption program and bring GBTC closer inline with the price of bitcoin.

I doubt this will ever happen. Grayscale is sitting on a cash cow. As long as it can redirect investor anger at the SEC, why change?

“There is no obligation to convert to an ETF,” David Fauchier, a fund manager at London’s Nickel Digital Asset, told me in a tweet. “If things stay as they are, they will print money into perpetuity basically, it’s a FANTASTIC business if BTC doesn’t zero.”

Ha. No, the status quo is to keep the trust as is. There is no obligation to convert to ETF. If things stay as they are, they will print money into perpetuity basically, it’s a FANTASTIC business if BTC doesn’t zero

Fed by stimulus money, tethers, and a new grift in the form of NFTs, the price of bitcoin reached a record of nearly $69,000 in November 2021. Bitcoiners rah-rahed the moment.

However, the same network effects that brought BTC to its heights are working in reverse and can just as easily bring it back down again. At its current price of $40,000, amidst 8.5% inflation, bitcoin is not proving itself to be the inflation hedge Grayscale hyped it up to be.

I encourage anyone reading this to submit your comments to the SEC regarding Grayscale’s application for a spot bitcoin ETF. Jorge Stolfi, a computer scientist in Brazil, has provided an excellent example, and so has David Rosenthal, also a computer scientist. You can submit your own comments here.

Did you enjoy this story? Consider supporting my work by subscribing to my Patreon account for as little as $5 a month. It’s the cost of a cup of coffee! Or, if you’re feeling generous, you can buy me a pound of coffee beans.